Payrolling Benefits in Kind UK: 5 April 2026 Deadline Guide for Employers

Payrolling benefits in kind can cut year-end admin. Use this UK guide to meet the 5 April 2026 deadline, avoid P11D mistakes, and plan Class 1A NICs.

Payrolling Benefits in Kind UK: 5 April 2026 Deadline Guide for Employers

Payrolling benefits in kind is moving from a niche payroll choice to a mainstream compliance step for UK employers. If you want to payroll benefits for the 2026 to 2027 tax year, HMRC says you need to register before the new tax year starts, which means action before 5 April 2026. Miss that window and you may be back in the P11D cycle for another year for benefits that could have been handled through payroll.

Plenty of directors and payroll managers are asking the same thing right now: should we stick with P11D forms for one more year, or switch early and settle the process before mandatory payrolling arrives in April 2027? Good question. The answer depends on your team size, benefit mix, and how stable your payroll data is today.

Quick summary: if your benefit records are reliable, voluntary payrolling in 2026 to 2027 can reduce year-end form pressure and spread tax deductions through the year. The key date is 5 April 2026, and the setup work is not just a tick-box exercise.

If you want a hands-on review before registering, we can help through our payroll services, bookkeeping support, and Self Assessment service.

What payrolling benefits in kind means in plain English

Benefits in kind are non-cash perks you give employees or directors, like private medical insurance, company cars, or beneficial loans. Under the old route, you usually report those at year-end on form P11D, then submit P11D(b) for Class 1A National Insurance.

Payrolling benefits in kind changes the timing. Instead of waiting until after year-end, the taxable value goes through payroll during the tax year. Your employee pays Income Tax as they are paid, often with fewer later tax code adjustments.

That can feel cleaner for employees because the tax impact is visible month by month. It can also be cleaner for employers, as long as your payroll setup is accurate.

Accuracy is the part many teams underestimate.

Key dates to put in your diary now

Right, so let us pin down the dates that matter for this cycle.

| Date | What it means | Why it matters |

|---|---|---|

| 5 April 2026 | Last day before tax year starts | Practical deadline to register to payroll benefits for 2026 to 2027 |

| 6 April 2026 | Start of 2026 to 2027 tax year | Payrolling can begin if registration and setup are complete |

| 6 July 2026 | P11D and P11D(b) filing deadline for 2025 to 2026 | Still applies for benefits not payrolled in that prior year |

| 19 or 22 July 2026 | Class 1A NIC payment deadline | Payment date depends on method (post or electronic) |

| 6 April 2027 | Mandatory payrolling target date (current policy position) | Gives one year to test process voluntarily |

Dates can shift if policy changes, so check HMRC updates close to filing dates. We recommend a short compliance check each quarter.

Why this matters in March 2026

March is not just year-end planning season for Corporation Tax and dividends. Payroll teams are also dealing with final submissions, coding notices, and reconciliations. Adding benefit reporting changes on top can feel heavy.

Still, March is the best point to decide. If you wait until late April, the decision is made for you.

The other reason this is timely is policy direction. HMRC has been clear that mandatory payrolling of benefits is coming in April 2027, after an earlier timeline was pushed back. That delay gives employers breathing room, but only if you use it to test and improve your process.

One quiet year of voluntary setup usually beats one noisy year of forced change.

P11D route vs payrolling route

No single answer fits every employer. A good decision comes from mapping your real process, not copying what another company did.

| Area | Traditional P11D route | Payrolling route |

|---|---|---|

| Income Tax timing | Often corrected after year-end through tax codes | Collected in-year via payroll |

| Admin pressure | Heavy peak around P11D season | More spread across payroll cycles |

| Employee clarity | Lower, as adjustments arrive later | Higher, as deductions appear in pay runs |

| Setup effort | Lower if you keep existing process | Higher at start, then steadier |

| Error profile | Late-year valuation and reporting errors | In-year coding and classification errors |

Worth mentioning though, the payrolling route does not remove all year-end work. You still need controls, reconciliations, and Class 1A handling.

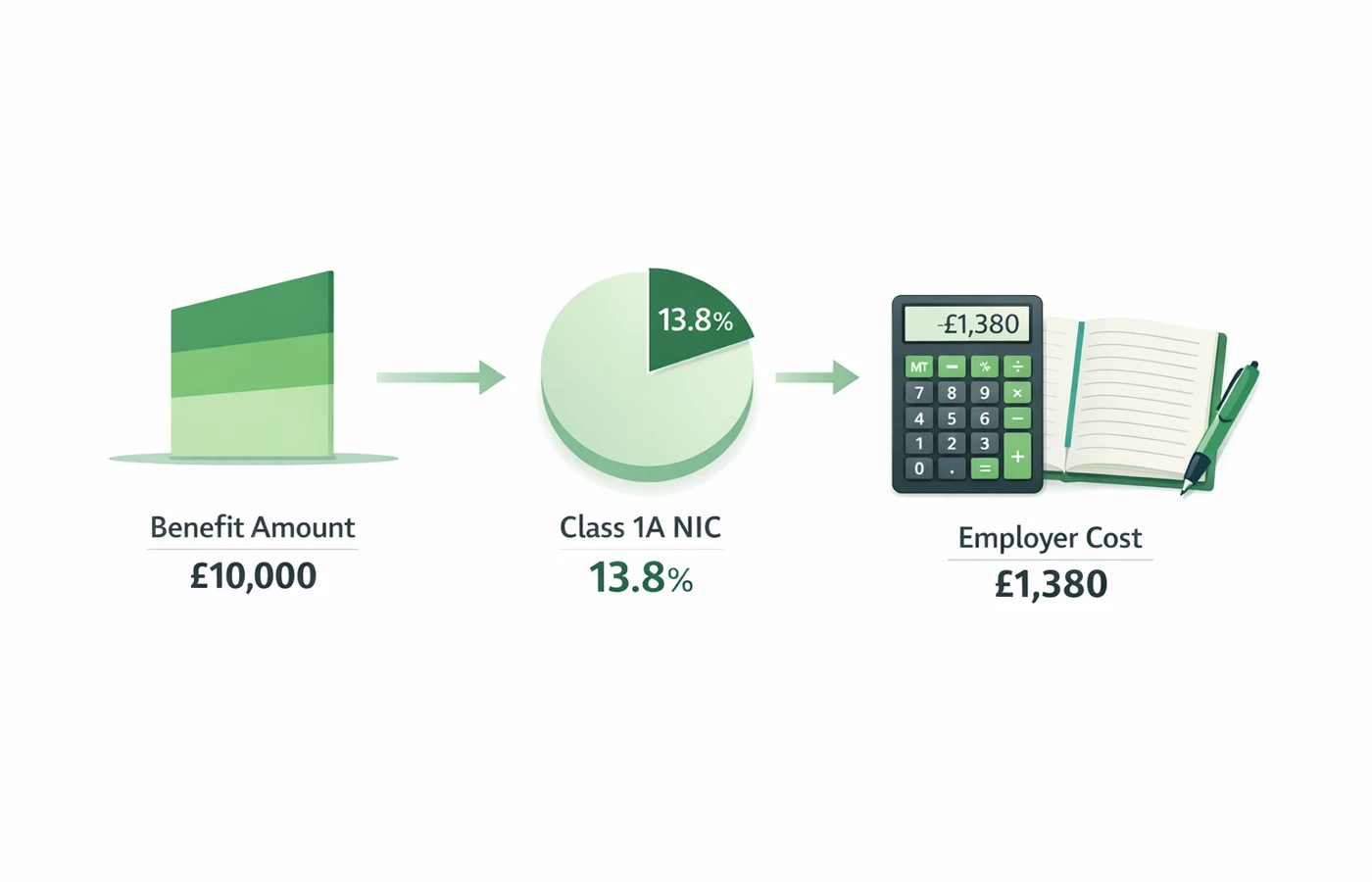

Worked example 1: private medical insurance benefit

Let us use a simple case. Imagine you provide private medical cover worth GBP 2,400 for an employee in 2026 to 2027.

Assume the employee is a basic rate taxpayer and the full benefit is taxable.

- Taxable benefit value: GBP 2,400

- Income Tax impact at 20%: GBP 480 for the year

- Approx monthly tax through payroll: GBP 40

Under a payrolling approach, that GBP 40 is typically spread in-year rather than corrected later through a tax code adjustment. Employees often prefer that because it is visible and predictable.

Now look at employer NIC.

If Class 1A NIC is due on this benefit and the rate is 15% for the year in question, the employer cost is:

- GBP 2,400 x 15% = GBP 360

Always check HMRC rates for the specific tax year before filing. Rates can change, and the exact treatment depends on benefit type and payroll configuration.

Worked example 2: small team with mixed benefits

Suppose a company has 8 employees and provides three benefit types:

- 3 employees: private medical cover, GBP 2,400 each

- 2 employees: gym benefit, GBP 600 each

- 1 director: beneficial loan equivalent value, GBP 1,800

- 2 employees: no taxable benefits

Total annual taxable benefits in scope:

- Medical: 3 x GBP 2,400 = GBP 7,200

- Gym: 2 x GBP 600 = GBP 1,200

- Loan benefit: GBP 1,800

- Total: GBP 10,200

If all were handled through payrolling and all employees were basic rate taxpayers for illustration:

- Employee Income Tax estimate: GBP 10,200 x 20% = GBP 2,040 collected across the year

Employer Class 1A estimate at 15%:

- GBP 10,200 x 15% = GBP 1,530

The cash cost to the employer is not magically lower just because reporting method changes. What changes is administration rhythm, data quality needs, and how clearly employees see tax deductions.

Worked example 3: late decision and the admin cost gap

Here is a practical comparison many growing firms face.

Scenario A: you register before the deadline and payroll 20 recurring benefits in-year.

- Initial setup and testing: 10 hours

- Monthly review: 1 hour x 12 = 12 hours

- Year-end reconciliation: 4 hours

- Total internal time: 26 hours

Scenario B: no registration, full P11D cycle with manual benefit collation.

- Year-end data gathering: 18 hours

- P11D preparation and corrections: 14 hours

- Employee query handling after coding changes: 8 hours

- Total internal time: 40 hours

No model is perfect, and your numbers will vary. Even so, many small employers find that moving work into monthly payroll checks reduces last-minute stress and error risk.

Step-by-step checklist before 5 April 2026

Use this as a working plan for March.

1. Confirm which benefits are in scope

List every benefit currently offered to employees and directors. Group them by type, frequency, and whether values are fixed or variable.

If your list is incomplete, pause here and fix that first.

2. Check payroll software and process readiness

Your software needs to support payrolled benefits correctly, including taxable value treatment and reporting outputs. Also check who reviews benefit values each month and who signs off changes.

A software feature exists on paper in many systems, but process ownership is what keeps it right.

3. Register with HMRC in time

Use HMRC guidance for registration and method selection. Leave time for internal checks rather than registering on the final day.

4. Decide what stays outside payrolling

Some benefit areas still require careful handling, and not every edge case is best handled in one sweep. Document your decisions and keep the rationale with payroll records.

5. Update employee communication

People notice net pay movement fast. Let staff know why deductions may change in appearance, what is being taxed, and where they can ask questions.

A short internal note now saves repeated confusion later.

6. Set a quarterly control review

Review calculations, classifications, and payroll mapping each quarter. Catching one misclassification in June is easier than fixing twenty in July.

Common mistakes we keep seeing

Treating registration as the whole project

Registration is the start. The real work is data quality, payroll mapping, and sign-off.

Mixing gross and taxable values

Benefit providers and internal reports may show figures in different formats. If you post the wrong value basis, payroll tax results drift quickly.

Ignoring director-specific complexities

Directors may have multiple income streams and existing tax code changes. A clean payroll setup still needs wider tax context, especially for owner-managed businesses.

Forgetting Class 1A planning

Payrolling affects employee Income Tax timing, but Class 1A obligations still need funding and deadline control.

Leaving employee communication too late

Silence creates payroll tickets. Payroll tickets create delay. Delay creates filing risk.

Internal links to help you implement this

If you are sorting the full process across payroll and accounts, these pages may help:

- Payroll services for UK employers

- Bookkeeping support for accurate records

- Self Assessment support for directors

- Contact our team

Authoritative sources used in this guide

- HMRC guidance on registering and operating payrolling: Payrolling benefits and expenses through your payroll

- HMRC employer year-end actions: PAYE for employers: End-of-year tasks

- Employer National Insurance rates and thresholds: Rates and thresholds for employers 2025 to 2026

- Policy timing for mandatory payrolling from April 2027: Tax update spring 2025

FAQ: payrolling benefits in kind

Do I still need to submit P11D forms if I payroll benefits?

Often you can reduce P11D submissions for benefits you have correctly payrolled. Edge cases and exclusions still need checking, and P11D(b) obligations for Class 1A remain relevant.

What happens if I miss the 5 April 2026 registration window?

You may need to wait for the next cycle and continue with existing year-end reporting for that tax year. If you are close to the deadline, act now and keep evidence of the steps you have taken.

Is payrolling always better than the P11D route?

Not always. Firms with irregular benefit data or weak monthly controls can struggle. A short readiness review is usually worth doing before switching.

Will employees pay more tax if we payroll benefits?

The total tax due on the same benefit does not usually change just because reporting method changes. Timing and visibility of deductions do change.

Do we still pay Class 1A NIC when benefits are payrolled?

In many cases, yes. Class 1A NIC is still part of employer obligations on taxable benefits in kind. Check current-year rates and exact treatment for each benefit.

Is this individual tax advice?

No. This guide is general information for UK employers and directors. Your figures may differ based on income mix, benefit design, and company structure, so personal advice is sensible before major decisions.

You can treat this week as the decision point. Either lock your payrolling setup before 5 April 2026, or plan a controlled P11D cycle and schedule a migration project for the following year. If you want a second pair of eyes before you commit, speak to our team.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

Year End Tax Planning for Limited Company Directors: 5 April 2026 Checklist

Year end tax planning for limited company directors before 5 April 2026. Use this practical UK checklist to cut surprises and plan tax efficiently.

MTD for Income Tax UK: April 2026 Checklist for Sole Traders and Landlords

MTD for Income Tax starts in April 2026 for many sole traders and landlords. Use this practical checklist to get ready, avoid penalties, and file with confidence.

Do I Need an Accountant for My Croydon Business?

Not sure if your Croydon business needs an accountant? Learn the difference between bookkeeping and accounting, and when it’s time to get professional help.