P11D Deadline 6 July 2026: UK Employer Guide to Benefits and Expenses

P11D deadline 6 July 2026 explained for UK employers, with what to report, Class 1A NIC examples, penalties, and a checklist.

P11D Deadline 6 July 2026: UK Employer Guide to Benefits and Expenses

The P11D deadline 6 July 2026 is the next big payroll date after P60 season. If you provided taxable benefits or expenses to employees or directors during the 2025/26 tax year, you may need to report them to HMRC by 6 July 2026, give employees their copy by the same date, and report the total Class 1A National Insurance due on form P11D(b).

This is the bit many small employers leave too late. Benefits data is rarely sitting in one neat place. Private medical invoices might be with HR, company car details with a director, mileage claims in accounting software, and employee reimbursements in the bank feed. By the time payroll asks for the figures, everybody suddenly remembers three things that should have been checked in April.

Quick summary: for the 2025/26 tax year, P11D and P11D(b) forms must usually be filed online by 6 July 2026. Employees must also receive their benefit information by 6 July 2026. Class 1A National Insurance is due by 19 July 2026 if paying by cheque, or 22 July 2026 if paying electronically. HMRC’s P11D(b) late filing penalty is GBP 100 per 50 employees for each month or part month the return is late.

If you want us to check your benefits, prepare the forms, and keep the July payment under control, we can help through our payroll services, bookkeeping service, and contact page.

P11D deadline 6 July 2026: the dates employers need

HMRC’s employer expenses and benefits deadline page sets out the core timetable. After the tax year ends on 5 April 2026, employers have until 6 July 2026 to report expenses and benefits, give employees a copy of the information, and report the total Class 1A National Insurance owed.

The payment deadline comes later in July. HMRC must receive Class 1A National Insurance by 19 July if you pay by cheque, or 22 July if you pay electronically. For 2026, that means the electronic payment date is 22 July 2026.

| Task | Deadline for 2025/26 benefits |

|---|---|

| File P11D forms, where needed | 6 July 2026 |

| File P11D(b) for Class 1A NIC | 6 July 2026 |

| Give employees a copy of their benefit information | 6 July 2026 |

| Pay Class 1A NIC by cheque | 19 July 2026 |

| Pay Class 1A NIC electronically | 22 July 2026 |

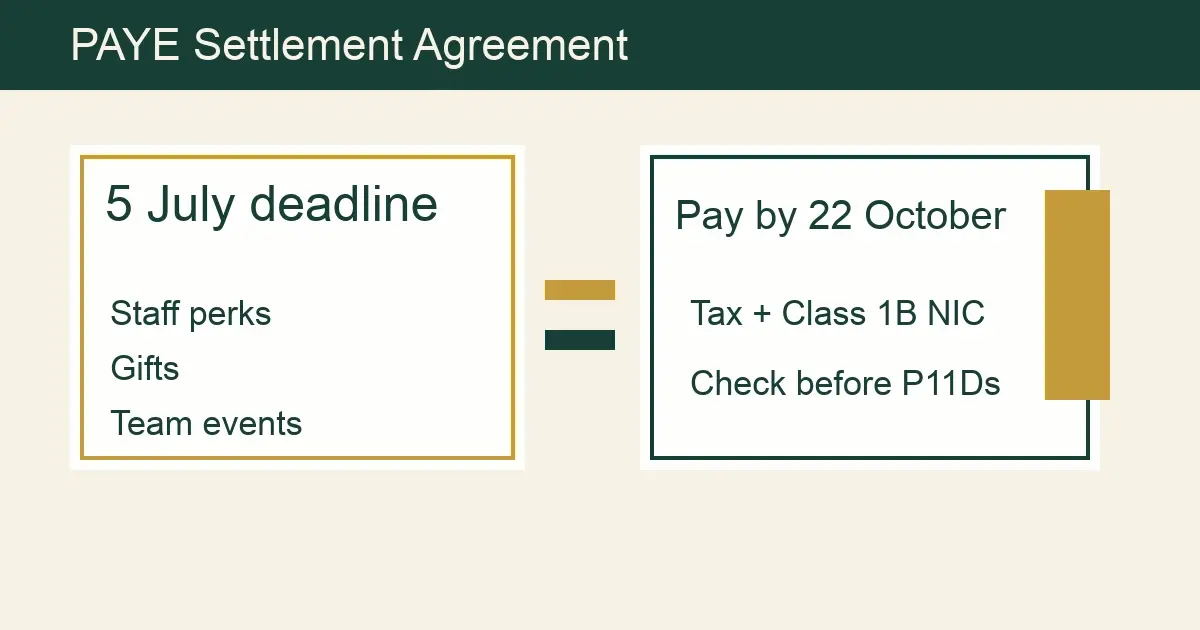

| Pay PAYE Settlement Agreement tax and Class 1B NIC, if relevant | 22 October 2026 electronically, or 19 October 2026 by cheque |

Official HMRC and GOV.UK references:

- Expenses and benefits for employers: deadlines

- Expenses and benefits for employers: reporting and paying

- April 2026 Employer Bulletin

- Class 1A National Insurance contributions on benefits in kind: 2026 guide

There is a practical reason for starting in May rather than late June. P11D work usually needs payroll, bookkeeping, HR, and directors to agree the same figures. If one person has the company car paperwork and another has the health insurance renewal, the deadline can disappear quickly.

What P11D and P11D(b) forms actually do

A P11D reports taxable expenses and benefits for an individual employee or director. Think of items like private medical insurance, company cars available for private use, beneficial loans, living accommodation, assets made available for personal use, and certain non-exempt expenses.

A P11D(b) is different. It is the employer’s summary of the Class 1A National Insurance due on taxable benefits. You may need a P11D(b) even if no individual P11D forms are due, because payrolled benefits can still create Class 1A National Insurance.

That distinction matters because payrolling benefits does not make the National Insurance side vanish. If you registered before the start of the tax year and taxed the benefit through payroll, the employee may not need a P11D for that benefit. The employer still needs to report the Class 1A position through P11D(b), unless the specific item is outside Class 1A.

Here is the quick split:

| Situation | P11D needed? | P11D(b) needed? |

|---|---|---|

| Benefits not payrolled, such as private medical insurance | Usually yes | Usually yes |

| All taxable benefits correctly payrolled | Often no individual P11D for those benefits | Usually yes |

| HMRC has asked for a P11D(b) | Depends on benefit position | Yes, respond to HMRC’s notice |

| Only exempt expenses reimbursed with proper checks | Usually no | Usually no |

| PAYE Settlement Agreement covers minor or irregular items | Usually no P11D for PSA items | PSA tax and Class 1B NIC follow the PSA process |

If you are unsure which route applies, do not guess from the label on the expense. Look at what was provided, who was contractually liable, whether it was taxed through payroll, and whether an exemption applies. The same cost can be treated differently depending on how it was arranged.

What employers usually need to report

The P11D process is not just a list of perks. It is a tax report, so the details matter.

Common reportable items include:

- private medical insurance

- company cars and fuel for private use

- company vans and van fuel, where private use is more than insignificant commuting or business travel

- beneficial loans to employees or directors

- assets made available for private use

- living accommodation

- non-business travel or entertainment

- subscriptions or club memberships paid for the employee’s personal benefit

- round sum allowances that are not properly matched to business costs

Some payments are exempt if the rules are met. For example, business travel, certain phone bills, uniforms and tools can be covered by HMRC exemptions when the employer is reimbursing actual business costs or paying approved flat rates, with checks in place.

Trivial benefits also have their own conditions. GOV.UK says a trivial benefit can be tax-free if it costs GBP 50 or less to provide, is not cash or a cash voucher, is not a reward for work or performance, and is not part of the employee’s contract. For directors of close companies, there is also a GBP 300 annual cap for trivial benefits provided to the director, office holder, or their family or household.

That sounds generous, but it is easy to get wrong. A GBP 45 birthday gift can be fine if it meets the conditions. A GBP 45 voucher promised under an incentive scheme is not the same thing. HMRC looks at why the benefit was provided, not just the amount.

Worked example 1: private medical insurance and Class 1A NIC

Assume a small limited company paid for private medical insurance for one director during the 2025/26 tax year. The annual taxable benefit is GBP 2,400.

If the benefit was not payrolled, the company would usually report GBP 2,400 on the director’s P11D. The director pays Income Tax on the benefit through their tax code or Self Assessment, depending on the position.

The employer then calculates Class 1A National Insurance on the taxable benefit. The Class 1A rate for the relevant year is the employer Class 1 NIC rate for that tax year. For 2026/27, HMRC’s CWG5 guide gives a 15% Class 1A rate in its worked example, and the same 15% employer rate applies from April 2025 onward for ordinary employer NIC planning.

Calculation:

- taxable medical benefit: GBP 2,400

- Class 1A NIC rate: 15%

- employer Class 1A NIC: GBP 2,400 x 15% = GBP 360

So the employer needs to budget GBP 360 for Class 1A NIC on top of the medical insurance cost. The director’s personal tax cost is separate.

If you run payroll through us, this is the type of check we would tie back to supplier invoices, payroll treatment, and director records before the July filing. A clean bookkeeping process makes the P11D job much less painful.

Worked example 2: company car benefit for an electric car

Company cars often take longer because the taxable benefit depends on the car’s list price, emissions, fuel type, dates available, and any employee contribution. HMRC has a company car and fuel calculator, but you still need accurate inputs.

Assume a director had a fully electric company car available throughout 2025/26. The car’s list price, including accessories used for benefit purposes, is GBP 35,000. The appropriate percentage for a zero-emission car in 2025/26 is 3%.

Car benefit calculation:

- list price: GBP 35,000

- appropriate percentage: 3%

- taxable car benefit: GBP 35,000 x 3% = GBP 1,050

Employer Class 1A NIC:

- taxable car benefit: GBP 1,050

- Class 1A NIC rate: 15%

- employer Class 1A NIC: GBP 1,050 x 15% = GBP 157.50

That looks modest for an electric car, which is why many directors have considered electric vehicles. The figures change if the car is not zero emission, if it was only available for part of the year, or if private fuel was provided. Your specific vehicle and dates matter.

For vans, GOV.UK’s published travel and mileage rates show the 2025/26 van benefit charge at GBP 4,020 and the 2025/26 van fuel benefit charge at GBP 769. Those figures only apply when the van benefit rules are triggered. A van used for business travel and ordinary commuting with no more than insignificant other private use may be treated differently, so the usage evidence matters.

Worked example 3: a director loan that becomes a benefit

Beneficial loans can be easy to miss because they sit between bookkeeping and payroll. If a director or employee has a loan from the company and the interest charged is below HMRC’s official rate, there may be a taxable benefit.

Assume a director had an average company loan balance of GBP 20,000 during the tax year and paid no interest. If the official rate used for the calculation were 2.25%, a simple estimate of the benefit would be:

- average loan balance: GBP 20,000

- official rate: 2.25%

- taxable benefit estimate: GBP 20,000 x 2.25% = GBP 450

Employer Class 1A NIC at 15% would be:

- GBP 450 x 15% = GBP 67.50

The real calculation can differ if the loan balance moved during the year, if interest was paid, or if the average method does not give a fair result. Director loans also have separate Corporation Tax and company law issues, so do not treat the P11D calculation as the whole story. Our annual accounts service can help tie the loan account, benefit position, and company tax reporting together.

The records to pull before you start the forms

The fastest P11D work starts with a checklist, not with the form itself. If you open HMRC’s online service before the benefit records are ready, you will end up stopping and starting.

Pull these records first:

- payroll reports for the 2025/26 tax year

- list of employees and directors who received benefits

- private medical, dental, and insurance invoices

- company car details, including list price, CO2 emissions, fuel type, availability dates, and employee contributions

- van usage records and evidence of private use restrictions

- fuel card records

- director loan account balances and interest paid

- employee expense claims and reimbursement reports

- staff entertaining and gift records

- salary sacrifice or optional remuneration arrangement notes

- evidence for exempt business expenses

- details of any benefits already payrolled

For most small employers, the biggest risk is not an exotic tax rule. It is missing one ordinary item because it was coded poorly in the accounts. A private medical bill posted to “insurance” can look harmless until someone asks whether it was for the business or for a director.

Right, so the accounting codes matter. If your software has a single vague expenses category, P11D season becomes detective work. Use separate codes for staff welfare, private medical insurance, business travel, entertainment, company cars, fuel, subscriptions, and director loans. That does not make the tax decision for you, but it makes the review much easier.

Common P11D mistakes small employers make

The first mistake is assuming the payroll software knows everything. It only knows what someone entered. If the bookkeeper posts a supplier invoice as general insurance and the payroll processor never sees it, the software will not magically create a P11D entry.

The second mistake is filing P11D forms but forgetting P11D(b). HMRC’s April 2026 Employer Bulletin is clear that P11D and P11D(b) forms for 2025/26 must be filed online and at the same time. It also reminds employers that P11D(b) is needed if you have submitted P11D forms, payrolled benefits, or HMRC has asked you to file one.

Another common problem is treating every reimbursement as tax-free. Reimbursing a genuine business expense with evidence is one thing. Paying a round sum allowance because it is administratively convenient is another. HMRC will expect you to show why the payment is exempt or how it was taxed.

Cars create their own problems. HMRC’s February 2026 Employer Bulletin highlighted common P11D car data errors, including incorrect registration date, fuel type, CO2 figure, electric car zero-emission mileage, engine size, and missing cash equivalent values. Those are not tiny details. One wrong input can change the tax code, employee tax bill, and employer Class 1A NIC.

The final mistake is failing to give employees their copy by 6 July 2026. Filing with HMRC is only half the job. Employees need the information too, especially if they complete a Self Assessment tax return or need to query a tax code.

What happens if you miss the P11D deadline

HMRC says the P11D(b) late filing penalty is GBP 100 per 50 employees for each month or part month the return is late. Late payment of Class 1A National Insurance can also lead to interest and penalties.

Here is a simple example. Say a business has 23 employees and its P11D(b) is filed two months late. The penalty is based on one block of up to 50 employees:

- penalty per month or part month: GBP 100

- number of late months or part months: 2

- estimated P11D(b) late filing penalty: GBP 200

Now assume a business has 74 employees and files two months late. That is two blocks of 50 employees:

- penalty per month or part month: GBP 200

- number of late months or part months: 2

- estimated P11D(b) late filing penalty: GBP 400

That is before you consider interest on late Class 1A NIC. It is a frustrating way to spend money because most P11D deadline problems are avoidable with a decent May and June process.

If you have missed the deadline, deal with it quickly. File the forms, pay what is due, correct employee copies where needed, and keep evidence of why the delay happened. If HMRC charges a penalty and you believe there is a valid reason to appeal, get advice before sending a rushed explanation.

Should you payroll benefits instead next year?

Payrolling benefits can reduce the year-end rush because the employee pays tax through payroll during the year rather than waiting for P11D reporting after 5 April. We covered that choice in more detail in our payrolling benefits in kind guide.

For the 2026/27 tax year, the registration window mattered before the year started on 6 April 2026. If you did not register in time, you may still be in the P11D process for certain benefits. Looking ahead, mandatory payrolling of benefits is expected from April 2027, so employers should start cleaning up benefit data now rather than waiting for the change to arrive.

Payrolling is not a shortcut if your records are messy. You still need accurate benefit values, employee communication, payroll setup, and year-end Class 1A reporting. It spreads the work across the year, which is useful, but it also means errors can repeat every pay run if the setup is wrong.

The best time to decide on next year’s process is straight after this year’s P11D filing. While the pain is still fresh, list what took longest:

- finding invoices

- checking car details

- working out director loan balances

- separating exempt and taxable expenses

- explaining benefits to employees

- calculating Class 1A NIC

That list becomes your payroll improvement plan for 2026/27.

FAQ: P11D deadline 6 July 2026

What is the P11D deadline for the 2025/26 tax year?

The deadline is 6 July 2026 to report taxable expenses and benefits for the tax year ended 5 April 2026, where P11D reporting applies.

Do employees need a copy of their P11D information?

Yes. Employees must receive a copy of the information by 6 July 2026 as well.

When is Class 1A National Insurance due?

Class 1A National Insurance for 2025/26 benefits is due by 19 July 2026 if paying by cheque, or 22 July 2026 if paying electronically.

Do I need a P11D if benefits were payrolled?

Often you will not need an individual P11D for benefits that were correctly payrolled, but you may still need to file P11D(b) to report Class 1A National Insurance.

What is the P11D(b) penalty for late filing?

HMRC states that the P11D(b) late filing penalty is GBP 100 per 50 employees for each month or part month the return is late.

Are trivial benefits reported on P11D?

Not if all trivial benefit conditions are met. The benefit must cost GBP 50 or less, must not be cash or a cash voucher, must not be a reward for work, and must not be contractual. Close company directors also have a GBP 300 annual cap.

Can Golden Tree Consulting prepare P11Ds for us?

Yes. We can review your payroll and bookkeeping records, identify reportable benefits, prepare P11D and P11D(b) forms, and help you plan the Class 1A payment. Start with our payroll services or contact us.

Your next step before July

Pull your 2025/26 benefits list before the end of May and compare it to payroll, bookkeeping, and director loan records. That one check will catch most of the nasty surprises before the P11D deadline gets close. If the figures do not tie together, fix the records before you file rather than sending HMRC a tidy-looking form based on untidy data.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

P46 Car Form Deadline 2026/27: Company Car Reporting Guide

P46 Car form deadline 2026/27 explained for employers, with quarterly dates, payroll rules, company car tax examples, and checks.

Payrolling Benefits in Kind UK: 5 April 2026 Deadline Guide for Employers

Payrolling benefits in kind can cut year-end admin. Use this UK guide to meet the 5 April 2026 deadline, avoid P11D mistakes, and plan Class 1A NICs.

PAYE Settlement Agreement Deadline 5 July 2026: Employer Guide

PAYE Settlement Agreement deadline guide for 2026, with PSA dates, eligible benefits, tax gross-up examples, and employer checklist.