VAT Registration Threshold UK: When to Register, Deadlines, and Worked Examples for 2026

VAT registration threshold UK rules for 2026 explained with deadlines, worked examples, voluntary registration pros and cons, and common mistakes to avoid.

VAT Registration Threshold UK: When to Register, Deadlines, and Worked Examples for 2026

The VAT registration threshold UK businesses need to monitor is GBP 90,000 of VAT taxable turnover on a rolling 12-month basis. If your sales are rising this spring, this is the moment to check your numbers before the new tax year starts on 6 April 2026. Waiting until year end accounts are done is how late registrations happen.

A lot of owners still track turnover by financial year only. HMRC does not use that test for compulsory VAT registration. It uses a rolling 12-month look-back test, plus a forward look if you expect to exceed the threshold in the next 30 days alone. That catches growing businesses faster than many people expect.

Quick summary: track your rolling 12-month taxable turnover monthly, act quickly when you cross GBP 90,000, and use a cash-flow forecast before choosing voluntary registration.

If you want us to review your numbers and registration timing, we can help through our VAT returns service, bookkeeping service, and contact page.

VAT registration threshold UK rules in plain English

Let us pin down the rules first.

| Rule area | Current figure or rule | What it means for you |

|---|---|---|

| Compulsory VAT registration threshold | GBP 90,000 taxable turnover | Register if your rolling 12-month taxable turnover goes above this level |

| VAT deregistration threshold | GBP 88,000 | You can usually apply to deregister if future taxable turnover is expected to stay below this |

| Rolling period | Previous 12 months, checked continuously | Not your tax year, not your accounting year |

| Forward look test | Next 30 days alone expected to exceed GBP 90,000 | Can trigger registration even if your last 12 months are below threshold |

The thing to remember is that VAT taxable turnover is not the same as profit. It is your VAT taxable sales value, before VAT, across the relevant supplies.

Primary references:

Why March and April are key for VAT decisions

Right now, we are in that awkward period where many businesses have a strong end to the tax year and new contracts starting in April. If your turnover has been climbing, a delayed review can mean you only spot the threshold breach after the deadline has passed.

HMRC’s registration deadline mechanics are strict. In many cases, when you exceed the threshold over a rolling 12-month test, you must register within 30 days from the end of the month in which you crossed. Your effective date of registration is commonly the first day of the second month after you crossed.

A short delay can create three separate problems:

- backdated VAT liability on sales

- interest and potential penalties

- messy customer conversations if you need to reissue invoices

None of those are fun in May when you are already dealing with payroll year-end follow-up and normal quarter-end work.

What counts towards VAT taxable turnover, and what does not

Many registration mistakes begin here.

Usually included

- standard-rated sales

- reduced-rated sales

- zero-rated taxable sales

- most business goods and services supplied in the UK that are VAT taxable

Not usually included

- exempt supplies (for example, certain financial or education supplies)

- income outside the scope of UK VAT

- sale of capital assets in some contexts, depending on treatment

If you have mixed income streams, for example UK client work plus overseas activity, classification matters. We often see people either undercounting or overcounting because they are using bank statement totals instead of VAT classifications.

Worth mentioning though, borderline cases can get fiddly quickly. If your supply type is unusual, it is better to get a technical check than assume.

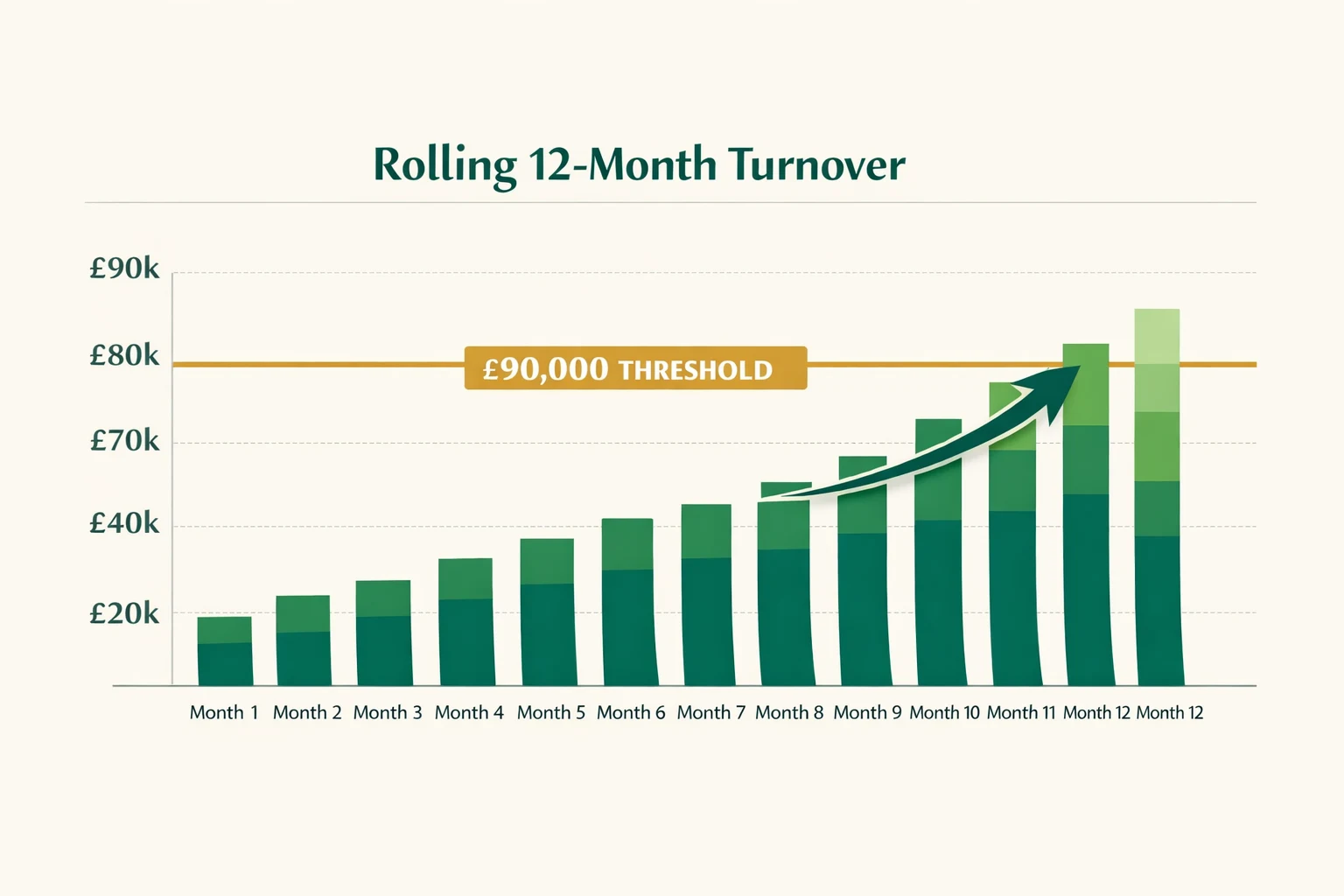

Worked example 1: rolling 12-month test catches a growing business

Assume a marketing consultancy has the following monthly VAT taxable turnover (before VAT):

| Month | Turnover |

|---|---|

| Apr 2025 | GBP 5,800 |

| May 2025 | GBP 6,200 |

| Jun 2025 | GBP 6,500 |

| Jul 2025 | GBP 6,900 |

| Aug 2025 | GBP 7,100 |

| Sep 2025 | GBP 7,300 |

| Oct 2025 | GBP 7,900 |

| Nov 2025 | GBP 8,400 |

| Dec 2025 | GBP 8,900 |

| Jan 2026 | GBP 9,400 |

| Feb 2026 | GBP 10,100 |

| Mar 2026 | GBP 10,300 |

| Total rolling 12-month taxable turnover at end of March 2026: GBP 94,800. |

That is above GBP 90,000, so compulsory registration is triggered.

If this threshold was first exceeded in March, registration action is due within the next month-end window. If registration is delayed, output tax may still be due from the effective registration date even where VAT was not added to original invoices.

That is the cash-flow hit owners tend to miss.

Worked example 2: 30-day forward look rule after a new contract

Assume a software contractor has rolling 12-month turnover of GBP 72,000 at 31 March 2026. They sign a UK contract on 2 April worth GBP 95,000 to be invoiced within 30 days.

Even though historic rolling turnover is below GBP 90,000, the forward look rule can trigger compulsory registration because expected VAT taxable turnover in the next 30 days alone exceeds the threshold.

Practical steps in this scenario:

- confirm contract timing and VAT liability of the supply

- register quickly rather than waiting for normal monthly review

- align invoice terms so VAT is charged correctly from the effective date

When this is handled early, it is manageable. When it is handled late, you can end up paying VAT out of margin.

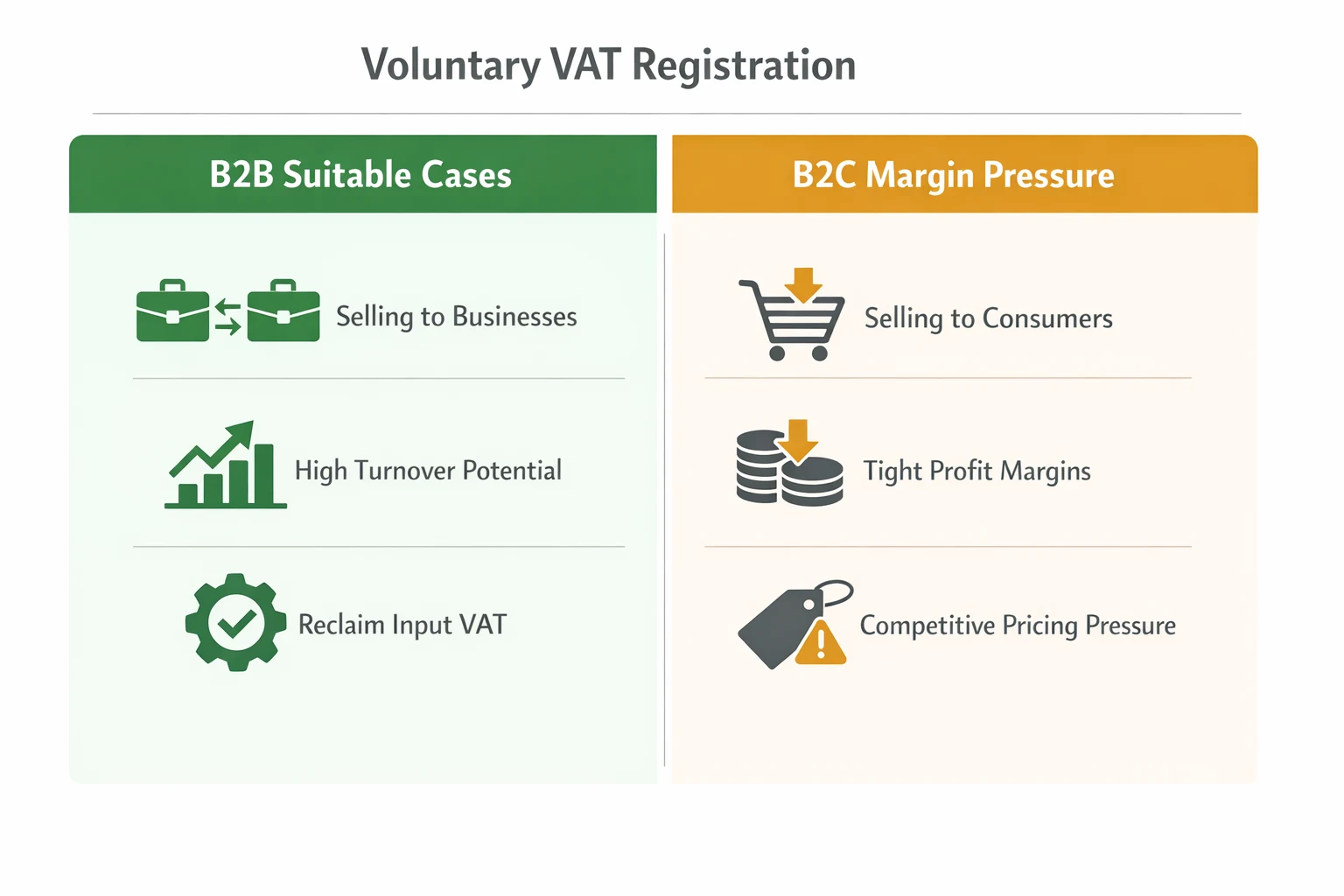

Voluntary VAT registration: when it helps and when it does not

You can register voluntarily below the threshold. That can be a smart move in the right business model, but not always.

Situations where voluntary registration can work well

- your clients are VAT-registered businesses that can usually reclaim input VAT

- you have significant VAT-bearing costs and want to recover input tax

- you want a cleaner VAT track record before growth accelerates

Situations where it can hurt margins

- many of your clients are consumers or non-VAT registered businesses

- your sector is price sensitive and adding VAT affects conversion

- admin capacity is weak and filing compliance is already stretched

Worked example 3: voluntary registration cash impact

Assume a design studio below threshold with annual sales of GBP 70,000 and VAT-bearing costs of GBP 18,000 + VAT.

If it registers voluntarily and invoices standard-rated supplies:

- output VAT on sales at 20%: about GBP 14,000

- input VAT recoverable on costs at 20%: about GBP 3,600

- net VAT payable to HMRC (illustrative): about GBP 10,400

If most clients can reclaim VAT, pricing pressure may be low, so registration can still make sense operationally.

Now change one assumption. If clients are mainly consumers who cannot reclaim VAT, adding 20% can reduce demand unless net prices are cut. In that case, voluntary registration can be expensive in commercial terms even if tax mechanics are correct.

So the decision is commercial first, tax second.

Flat Rate Scheme and cash accounting: useful options to compare

Some businesses ask about joining the Flat Rate Scheme once registered.

Current headline entry limits commonly used:

- Flat Rate Scheme turnover limit to join: up to GBP 150,000 (excluding VAT)

- Leave threshold: more than GBP 230,000 (including VAT)

There is also VAT cash accounting, generally available up to a higher turnover ceiling, often used for cash-flow control where customers pay late.

These schemes can simplify admin for some businesses, but they are not automatic wins. Flat rate percentages vary by sector, and limited cost trader rules can reduce the benefit.

Reference pages:

MTD for VAT and return deadlines you need in the diary

Every VAT-registered business has to keep digital records and submit VAT returns through compatible software under MTD for VAT.

| Item | Rule |

|---|---|

| Record keeping | Keep digital VAT records |

| Filing method | Submit through compatible software |

| Typical deadline | VAT return and payment due 1 month and 7 days after VAT period end |

| Planning point | Leave time for reconciliations before submission date |

If your bookkeeping is delayed each month, quarterly VAT filing becomes a scramble. If monthly bookkeeping is clean, VAT filings become routine.

Useful links:

Common VAT registration mistakes we keep seeing

Only checking turnover at year end

HMRC uses rolling 12 months. Annual-only checks miss threshold breaches.

Using profit instead of VAT taxable turnover

A low-margin business can hit VAT threshold long before profits feel high.

Registering late after a single large contract

The 30-day forward look test is often missed in fast growth periods.

Assuming voluntary registration is always “more professional”

Image matters less than pricing reality. If your clients cannot reclaim VAT, margin pressure can outweigh the branding argument.

Not preparing systems before registration date

If software, invoice templates, and bookkeeping rules are not ready, first-quarter VAT compliance gets messy quickly.

Forgetting to review invoice wording and contracts

If VAT wording is unclear, disputes over whether quoted prices are VAT inclusive can appear at the worst moment.

Practical registration checklist for the next 30 days

Use this as a working plan before and just after 6 April 2026.

- Pull monthly VAT taxable turnover for the previous 12 months.

- Recalculate rolling totals at each month-end point.

- Check forecast contracts for the next 30 days.

- Decide whether compulsory or voluntary registration applies.

- Register with HMRC and confirm your effective date.

- Update invoice templates to show VAT details correctly.

- Confirm bookkeeping categories and VAT codes in software.

- Build a VAT reserve into weekly cash-flow planning.

- Set return and payment reminders for each VAT quarter.

- Review your scheme choice after the first full quarter.

It is not glamorous work, but it prevents expensive surprises.

How this fits with your wider tax and accounts timeline

VAT should not be managed in isolation. It links directly to bookkeeping quality, pricing, and year-round compliance.

If you are also juggling Self Assessment, payroll, or company accounts deadlines, pull those dates into one cash-flow calendar so tax payments are planned as a sequence rather than one-off shocks.

You may find these pages useful:

For many owners, one monthly finance review meeting is enough to keep all of this under control.

FAQ: VAT registration threshold UK

What is the VAT registration threshold UK businesses use in 2026?

The compulsory VAT registration threshold is GBP 90,000 of VAT taxable turnover, measured on a rolling 12-month basis.

Is the threshold based on profit or turnover?

It is based on VAT taxable turnover, not profit.

Do I check the threshold by tax year?

No. You should check the previous rolling 12 months regularly, usually every month.

Can I register for VAT before reaching GBP 90,000?

Yes. Voluntary VAT registration is possible below the compulsory threshold.

What is the typical VAT return deadline after I register?

VAT returns and payments are usually due 1 month and 7 days after the end of the VAT period.

What if my situation is complex or borderline?

The guide gives general information, not personal tax advice. If your supplies include mixed VAT treatment or unusual contract terms, we recommend a tailored review before acting.

Your next step this week

Run a rolling 12-month VAT turnover check now, then set a recurring monthly reminder so you spot threshold issues early. If you want us to sense-check your numbers and registration date before April gets busy, get in touch.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

MTD for Income Tax UK: April 2026 Checklist for Sole Traders and Landlords

MTD for Income Tax starts in April 2026 for many sole traders and landlords. Use this practical checklist to get ready, avoid penalties, and file with confidence.

Allowable Expenses Self-Employed UK: What You Can Claim Before 5 April 2026

Allowable expenses self-employed UK rules explained with practical examples before 5 April 2026, so you can claim correctly and avoid HMRC issues.

Employer National Insurance and Payroll Changes UK 2026/27: Small Business Checklist

Employer National Insurance and payroll changes UK 2026/27 explained with rates, deadlines, and worked cost examples for small employers.