Business Asset Disposal Relief 2026: UK Guide for Small Business Owners

Business Asset Disposal Relief 2026 explained, with the 18% CGT rate, £1m lifetime limit, eligibility checks, and worked examples.

Business Asset Disposal Relief 2026: UK Guide for Small Business Owners

Business Asset Disposal Relief 2026 is no longer the 10% Capital Gains Tax break many business owners still have in their heads. For qualifying disposals made from 6 April 2026, the relief gives an 18% CGT rate, with a standard £1 million lifetime limit on qualifying gains. That still matters, but it changes the numbers for directors, sole traders, partners, and anyone planning a sale, closure, or solvent liquidation.

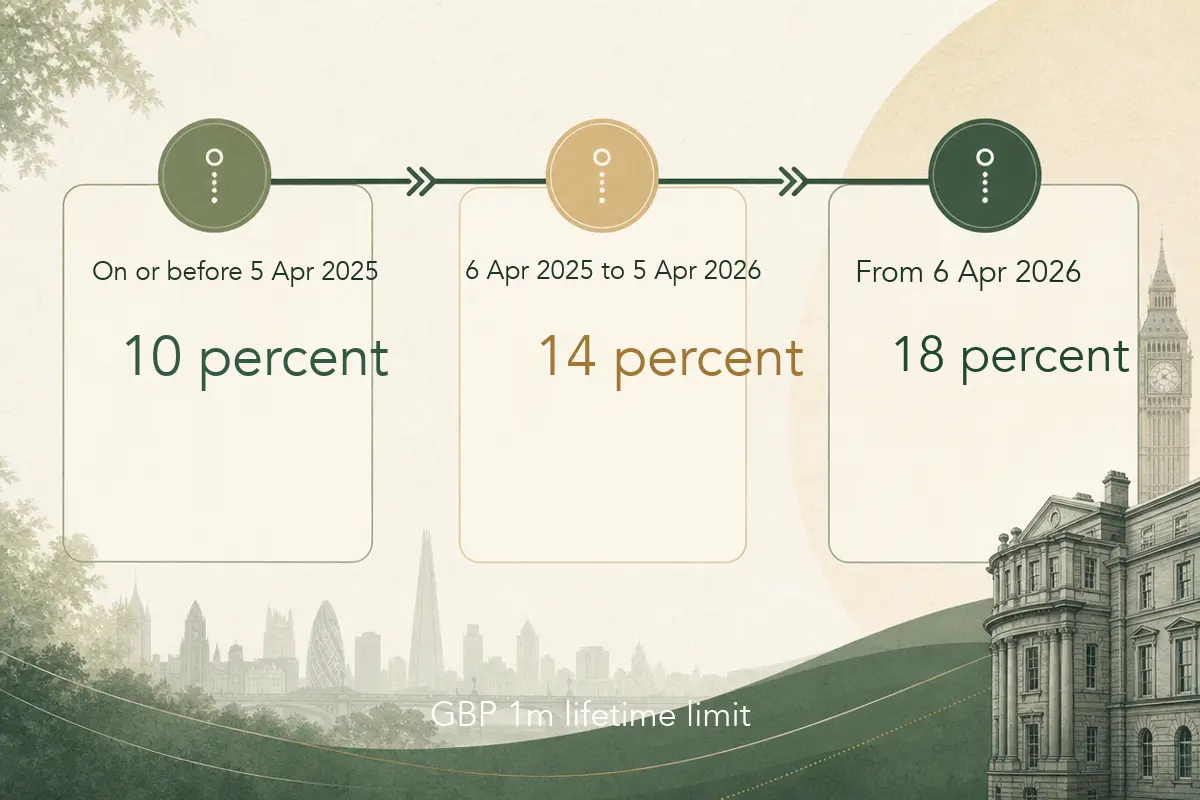

The timing matters because the rate has moved twice in quick succession. The relief was 10% for qualifying disposals on or before 5 April 2025, 14% for qualifying disposals between 6 April 2025 and 5 April 2026, and 18% from 6 April 2026. If your exit plan was based on old advice, a rough memory, or a chat from a few years ago, it needs a fresh calculation.

Quick summary: Business Asset Disposal Relief can still reduce CGT on a qualifying business sale, share sale, or closure, but from 6 April 2026 the rate is 18%, not 10%. Check the two-year conditions, the 5% personal company tests, the trading status of the business, the £1 million lifetime limit, and the claim deadline before you sign or wind up the company.

If you are planning a sale, closing a company, or trying to work out whether a claim is realistic, we can help through our company accounts service, Self Assessment service, bookkeeping service, or contact page.

Business Asset Disposal Relief 2026: the rates and limits

Business Asset Disposal Relief, often shortened to BADR, reduces the Capital Gains Tax rate on qualifying business gains. It used to be called Entrepreneurs’ Relief, which is why you may still hear both names. The old name is not the only thing that lingers. The old 10% rate does too, and that is now a problem.

Here are the rates that matter for current planning:

| Disposal date | BADR rate on qualifying gains |

|---|---|

| On or before 5 April 2025 | 10% |

| 6 April 2025 to 5 April 2026 | 14% |

| From 6 April 2026 | 18% |

The standard lifetime limit is £1 million of qualifying gains. You can claim more than once, but all qualifying gains claimed against the relief count towards that lifetime cap. Once the cap has been used, later gains are taxed under the normal CGT rules.

The official GOV.UK guidance confirms the current BADR rates and conditions on its Business Asset Disposal Relief page. GOV.UK also confirms that the annual exempt amount for individuals is £3,000 for 2026/27, and that the main CGT rates from 6 April 2026 are 18% and 24% for individuals, with 18% for gains qualifying for BADR or Investors’ Relief. You can check those figures on HMRC’s Capital Gains Tax rates and allowances page.

Why the move to 18% changes the planning conversation

An 18% rate is still lower than the 24% CGT rate that can apply to higher-rate taxpayers on gains from 6 April 2026. It is just not the eye-catching 10% rate people remember. For some owners, BADR still saves a meaningful amount. For others, the eligibility work, valuation work, and timing risks need to be weighed against a smaller tax difference.

That does not mean you should ignore it. A six percentage point saving on a large gain is still real money. It does mean you should stop using old shorthand such as “sell the company and pay 10% tax”. That phrase is now a warning sign.

Worked example 1: the rate rise on a £400,000 qualifying gain

Assume a director sells qualifying shares and makes a £400,000 gain. Ignore the annual exempt amount for a moment so the rate difference is easy to see.

If the disposal qualified at the 14% rate in 2025/26:

- £400,000 x 14% = £56,000 CGT

If the disposal qualifies at the 18% rate from 6 April 2026:

- £400,000 x 18% = £72,000 CGT

Difference:

- £16,000

That is not a small rounding adjustment. If a deal slipped from late March into April, or if the owner delayed a solvent liquidation without checking the tax effect, the rate change could be felt straight away.

There is a caveat. Tax should not be the only reason to rush or delay a sale. Price, buyer certainty, legal risk, earn-outs, warranties, funding, and the business itself can matter more than the rate. We would rather see a good deal taxed correctly than a weak deal forced through for a tax date.

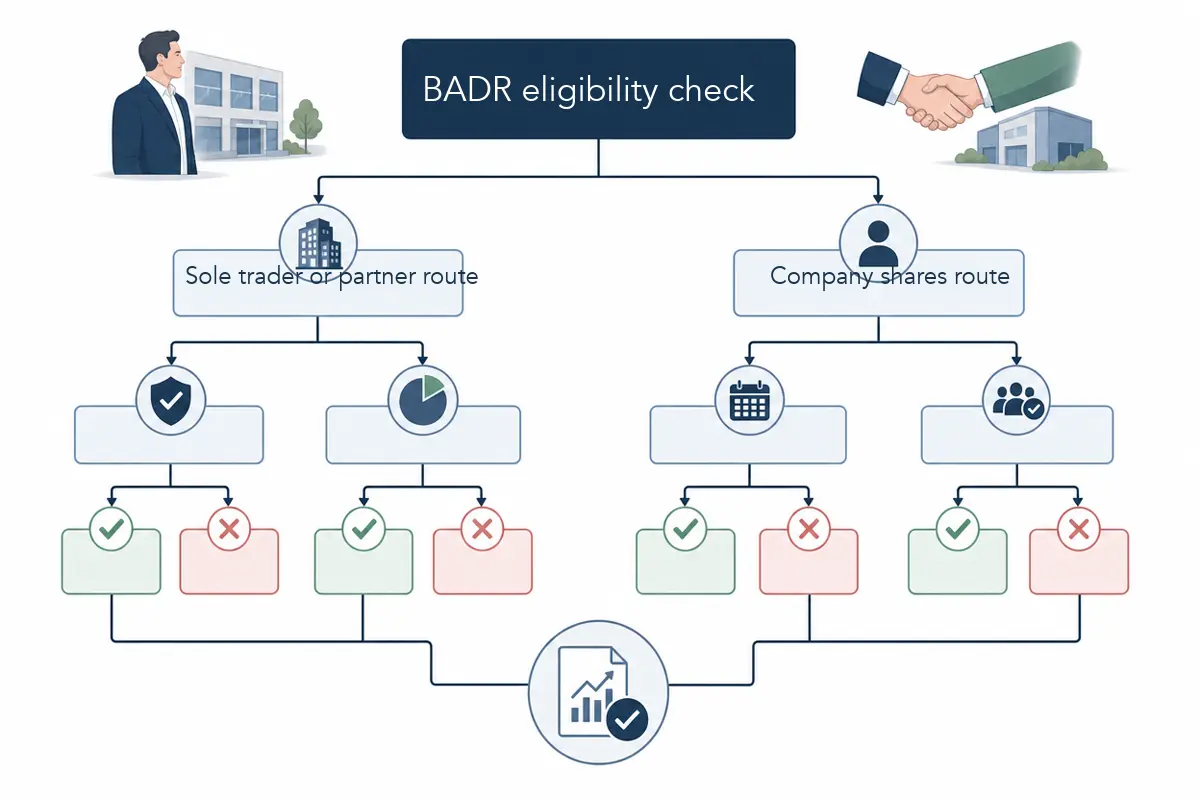

Who can qualify for Business Asset Disposal Relief?

The relief can apply to several kinds of business disposal. The most common for Golden Tree clients are:

- a sole trader selling all or part of a trading business

- a business partner selling all or part of their partnership interest

- a limited company director or shareholder selling shares in a personal trading company

- a shareholder receiving a capital distribution during a qualifying company winding-up

- an associated disposal, such as an asset personally owned by the business owner and used by the business, where the extra conditions are met

The rules are not identical for each case. That is where the trouble starts.

For a sole trader or partner selling all or part of the business, GOV.UK says you must generally have owned the business for at least 2 years up to the date of sale. If you are closing the business, the assets usually need to be disposed of within 3 years of closure to qualify.

For shares in a company, the tests are more detailed. For at least 2 years before the sale, you usually need to be an employee or office holder of the company or group, the company must be a trading company or holding company of a trading group, and the company must be your personal company.

For non-EMI shares, the personal company test broadly means you must hold at least 5% of the ordinary share capital and 5% of the voting rights. You must also be entitled to at least 5% of either profits and assets on a winding-up, or sale proceeds if the company is sold.

The limited company tests that catch directors out

Most director misunderstandings sit in three areas: share structure, trading status, and the two-year clock.

The share structure point is easy to miss when a company has alphabet shares, growth shares, investor shares, or several family shareholders. Holding 5% of the ordinary share capital and votes may not be enough if the economic entitlement test is not met. That is why you should not assume BADR applies just because you are a director and own shares.

The trading status point matters because investment activity can spoil the position. A company that mainly trades is one thing. A company that has become mostly an investment vehicle, holds surplus property, or has built up non-trading activity may need a proper review before any claim is made. A healthy cash balance is not automatically fatal, but it should be understood.

The two-year clock is the one that creates the most frustration. You cannot normally fix a missing two-year condition a week before completion. If the shareholding, voting rights, officer role, or trading status has not been in place for the required period, the claim may fail even where the owner feels they are obviously the person who built the business.

Worked example 2: a director whose shareholding falls below 5%

Assume Ravi owns 6% of the ordinary shares and voting rights in a trading company. He has been a director for six years and is expecting BADR to apply if the company is sold.

The company then issues new shares to investors. Ravi does not sell any shares, but his holding is diluted to 4.8%.

On a simple reading, Ravi may no longer meet the 5% personal company test. That could put BADR at risk on a later sale. GOV.UK guidance explains that there can be elections where a holding falls below 5% because of a relevant share issue, but those elections have their own mechanics and timing.

The practical lesson is blunt: check BADR before issuing shares, reorganising the cap table, or signing investment paperwork. Once the deal is done, the tax fix may be narrower than you hoped.

How BADR interacts with normal Capital Gains Tax

BADR is not a separate tax system. It sits inside the CGT calculation. You still need to work out the gain, deduct allowable costs, offset capital losses where relevant, apply the annual exempt amount where available, and then apply the right rates.

For 2026/27, the annual exempt amount for most individuals is £3,000. GOV.UK says the annual exempt amount can be used against gains charged at the highest rates. That can affect calculations where a person has more than one gain in the year, for example a business share sale and a separate investment disposal.

The normal CGT rates from 6 April 2026 are 18% and 24% for individuals. If BADR applies, the qualifying gain within the lifetime limit is charged at 18%. So for a higher-rate taxpayer, the difference is often 24% vs 18% on the qualifying slice, not 24% vs 10%.

Worked example 3: sale proceeds, exemption, and BADR at 18%

Assume Priya sells qualifying shares in her trading company in June 2026.

The numbers are:

| Item | Amount |

|---|---|

| Sale proceeds after professional costs | £520,000 |

| Original share cost and other allowable base cost | £220,000 |

| Chargeable gain before exemption | £300,000 |

| 2026/27 annual exempt amount | £3,000 |

| Taxable gain | £297,000 |

If the full taxable gain qualifies for BADR and Priya has enough of her lifetime limit left:

- £297,000 x 18% = £53,460 CGT

If the same taxable gain were taxed at 24% instead:

- £297,000 x 24% = £71,280 CGT

Illustrative BADR saving:

- £71,280 - £53,460 = £17,820

That saving is worth claiming if the facts support it. It is not worth claiming casually if the conditions are weak. HMRC can ask questions, and ICAEW’s tax news in May 2026 noted HMRC one-to-many letters about BADR claims where taxpayers may have exceeded the lifetime limit.

Claim deadlines and paperwork

You usually claim BADR through your Self Assessment tax return, with the Capital Gains summary pages where needed. GOV.UK also refers to Section A of the Business Asset Disposal Relief helpsheet. For 2025/26, the claim deadline shown by GOV.UK is 31 January 2028. For 2024/25, it is 31 January 2027.

That deadline is longer than the normal filing deadline, but you should not treat it as permission to leave the evidence until later. The best time to collect support for the claim is while the sale or closure is happening.

Keep records such as:

- sale agreement or completion statement

- share register and cap table

- Companies House records

- board minutes and shareholder documents

- employment or office holder evidence

- accounts showing trading activity

- valuation notes and professional fee invoices

- earlier BADR or Entrepreneurs’ Relief claims that used part of the lifetime limit

That last point is worth its own line. The lifetime limit looks simple until someone has made an earlier claim, changed accountant, or sold part of a business years ago. Do not rely on memory for this. Check old tax returns.

If you need help preparing the return and checking the supporting numbers, our Self Assessment service can sit alongside the company accounts and disposal paperwork.

Common BADR mistakes we would check before filing

Some BADR claims are strong. Others rely on a chain of assumptions that has not been tested. Before filing, we would look closely at these points:

| Risk area | What can go wrong |

|---|---|

| Lifetime limit | Old Entrepreneurs’ Relief or BADR claims are forgotten |

| Share percentage | Dilution, alphabet shares, or rights changes mean the 5% tests are not met |

| Officer or employee status | A shareholder is not actually an employee or office holder during the required period |

| Trading status | The company has drifted into investment activity or excessive non-trading assets |

| Timing | The two-year test or three-year disposal window is missed |

| Associated disposals | A personally owned asset does not meet the linked withdrawal conditions |

| Claim paperwork | The gain is entered, but the relief claim or supporting details are weak |

One more point for solvent company closures. A Members’ Voluntary Liquidation can produce capital distributions, which may be relevant for BADR, but the tax treatment depends on the facts. Anti-avoidance rules can apply where a person winds up a company and then carries on a similar trade or activity. That is not a corner to guess your way through.

Should you still plan around BADR?

Yes, where a real business disposal is being planned and the conditions can be met. No, if the only plan is to bolt a relief onto a transaction after the commercial decisions have already been made.

A sensible pre-sale review should answer these questions:

- What exactly is being sold: shares, trade assets, goodwill, property, or a mix?

- Is the business trading for BADR purposes?

- Has the owner met the two-year condition?

- Do the shares meet the 5% voting, capital, and economic entitlement tests?

- Has any lifetime limit already been used?

- Are there capital losses, other gains, or annual exempt amount planning points?

- Does the expected tax result still work if completion moves by a few weeks?

For owner-managed companies, this review often sits naturally with year-end accounts, management accounts, and director tax planning. The earlier it happens, the more options you have. Our annual accounts service and bookkeeping service can help get the numbers in a state where the tax advice is based on records, not guesswork.

FAQs

Is Business Asset Disposal Relief still 10%?

No. For qualifying disposals from 6 April 2026, BADR is 18%. It was 14% for qualifying disposals between 6 April 2025 and 5 April 2026, and 10% for qualifying disposals on or before 5 April 2025.

What is the Business Asset Disposal Relief lifetime limit?

The standard limit is £1 million of qualifying gains over your lifetime. You can claim more than once, but claims count towards that overall cap. If you used Entrepreneurs’ Relief in earlier years, that can matter too.

Can I claim BADR if I sell shares in my limited company?

Possibly. You usually need the company to be a trading company or holding company of a trading group, and for at least 2 years you need to be an employee or office holder and meet the personal company tests. For non-EMI shares, those tests include 5% share capital, 5% voting rights, and a 5% economic entitlement test.

Can landlords claim Business Asset Disposal Relief?

Usually not for ordinary letting activity. HMRC’s helpsheet says references to business do not include the letting of property. There have been special and transitional points around furnished holiday lettings, so property-related cases need careful checking.

How do I claim BADR?

Most claims are made through your Self Assessment tax return, with the Capital Gains pages and relief details completed correctly. GOV.UK also refers to the Business Asset Disposal Relief helpsheet. Keep the sale documents, share records, accounts, and evidence of earlier claims.

What should I do before selling my business?

Before signing, get the structure, shareholding, trading status, likely gain, lifetime limit, and claim evidence reviewed. Do this before completion if you can. Once the sale has happened, the tax calculation becomes more about reporting correctly than changing the result.

The practical next step is simple: if a sale, closure, or share restructuring is even a possibility in the next year, check BADR before the paperwork is locked. A one-page review now is much cheaper than finding out after completion that the relief you expected is not there.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

ERS Return Deadline 6 July 2026: Share Scheme Guide for UK Employers

ERS return deadline 6 July 2026 explained, with EMI notifications, nil returns, penalties, share events, and employer checklist.

Companies House Identity Verification 2026: Director and PSC Guide

Companies House identity verification explained for directors and PSCs in 2026, with personal codes, deadlines, and examples.

Self Assessment Payment on Account 31 July 2026: What to Pay and When

Self Assessment payment on account 31 July 2026 explained, with calculations, reduction rules, late interest, and cash-flow planning.