Employment Allowance UK 2026/27: Who Can Claim, Who Cannot, and How to Apply

Employment Allowance UK 2026/27 explained, with who can claim, who cannot, EPS steps, and worked examples for small employers.

Employment Allowance UK 2026/27: Who Can Claim, Who Cannot, and How to Apply

Employment Allowance UK 2026/27 is worth up to £10,500 off your employer National Insurance bill, which is a meaningful number now that the employer NIC rate is 15% and the annual secondary threshold is only £5,000. Plenty of small employers still miss it, and plenty of others claim it when they should not. Both problems are expensive in their own way.

April is a good moment to sort it out. The new tax year is live, the first PAYE runs are already moving, and HMRC says you need to claim Employment Allowance every tax year. If nobody has checked the payroll settings yet, you can end up paying more employer NIC than you need to, or building a claim on the wrong facts.

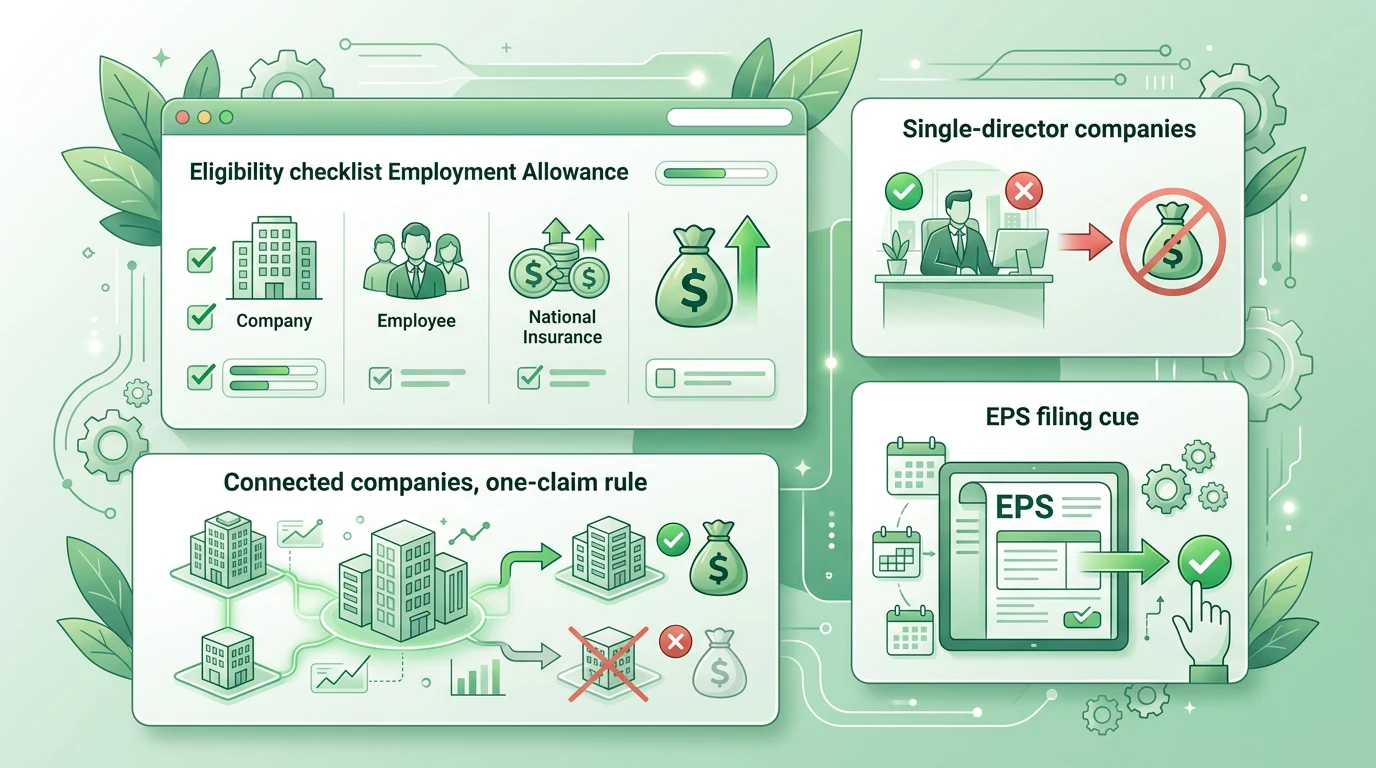

Quick summary: Employment Allowance for 2026/27 is up to £10,500. You claim it through an Employment Payment Summary (EPS). Many small employers can use it, including businesses with employer NIC liabilities above the old £100,000 limit, because HMRC says that restriction was removed from April 2025. A common trap is the single-director company rule. If your company has one director and that director is the only employee liable for secondary Class 1 NIC, you cannot claim.

If you want us to check your payroll setup and claim position before the next filing, we can help through our payroll services, bookkeeping service, and contact page.

What Employment Allowance is, and why it matters more in 2026/27

Employment Allowance reduces an eligible employer’s annual Class 1 employer National Insurance bill. HMRC’s published rates and thresholds say the allowance for 2026/27 is £10,500. That is not a tax refund in the abstract. It is a direct reduction against the employer NIC you would otherwise pay across the year.

That is why the timing matters. HMRC says you can claim at any point in the tax year, though the earlier you claim, the sooner the allowance starts reducing what you owe. If you leave it until later, the allowance is still there in principle, but your cash flow has already taken the hit.

The old £100,000 Class 1 NIC restriction also catches people out because they remember the previous rule. HMRC now says that from April 2025, employers paying more than £100,000 in Class 1 National Insurance liabilities can apply for Employment Allowance. In plain English, plenty of businesses that used to be outside the rules should now be checking again instead of assuming the answer is still no.

Useful HMRC references:

- Employment Allowance eligibility

- Employment Allowance: what you’ll get

- Rates and thresholds for employers 2026 to 2027

- Employment Allowance: when to claim

- Employment Allowance: how to claim

If you have already read our employer National Insurance changes guide for 2026/27, think of this post as the narrower follow-up. That guide covers the wider payroll cost picture. This one is about one question only: can you reduce that employer NIC bill legally, and if so, how do you do it properly?

Employment Allowance UK 2026/27: who can usually claim and who cannot

HMRC says you can claim Employment Allowance for the current tax year if both of these apply:

- you are a business or public body

- you do less than half your work in the public sector

There are also special routes for charities and for employers of care or support workers. On the other side of the line, HMRC highlights a few recurring exclusions and restrictions that small employers should know cold.

| Position | Usually eligible? | Why it matters |

|---|---|---|

| Ordinary trading business with employees on payroll | Usually yes | The common small employer case |

| Business doing more than half its work in the public sector | Usually no | HMRC blocks many public-sector-heavy organisations |

| Charity or CASC | Often yes | Subject to the normal detailed rules |

| Employer of a care or support worker | Often yes | Household work can be excluded unless it is care or support |

| Single-director company where the director is the only employee liable for secondary Class 1 NIC | No | One of the biggest traps |

| Connected group of companies | Only one company can claim | The allowance cannot be duplicated across the group |

| Employer with multiple payrolls | Only against one payroll | Needs planning so the claim goes in the right place |

| Worker within IR35 off-payroll rules | Cannot be included | HMRC excludes those earnings for the claim |

The thing that causes the most confusion is that people often focus on employee count, not on who is liable for secondary Class 1 NIC. HMRC’s wording is tighter than everyday shorthand. A company can have several workers and still fail the single-director test if the director is the only person above the secondary threshold.

For 2026/27, HMRC’s published thresholds show the annual secondary threshold is £5,000, or £417 per month. So when you are testing the single-director point, that threshold is the number to keep in mind.

The single-director company rule is where most wrong claims start

HMRC’s single-director guidance says limited companies cannot claim Employment Allowance if they have just one director and that director is the only employee liable for secondary Class 1 National Insurance. It also says companies with several employees are still not eligible where the director is the only employee paid above the secondary threshold.

That is why a lot of owner-managed companies get caught. Someone hears “we have more than one person involved in the business” and assumes the allowance is fine. HMRC is not asking whether there is more than one human around. It is asking whether there is more than one employee or director above the relevant threshold for employer NIC purposes.

There is a useful flip side here. HMRC also says that if more than one employee or director earns above the secondary threshold, the company can be eligible for Employment Allowance for the whole tax year. That can include husband-and-wife director companies, seasonal worker setups, or businesses that add another qualifying employee during the year.

Your exact position depends on the facts. We would not suggest changing payroll just to chase one relief without looking at salary, dividends, pensions, and wider tax effects. If you run a director-led limited company, read this alongside our salary vs dividends guide for 2026/27 before you make a move.

Worked example 1: single-director company that cannot claim

Assume Maya runs a limited company and is the only director. She pays herself a salary of £12,570 for 2026/27. There are no other employees paid above the secondary threshold.

HMRC’s annual secondary threshold is £5,000.

Employer NIC-able salary:

- £12,570 - £5,000 = £7,570

Employer NIC at 15%:

- £7,570 x 15% = £1,135.50

Potential Employment Allowance available in the tax year:

- £10,500

Can Maya use the allowance to wipe out the £1,135.50?

- No

Why not? Because she is the only director, and HMRC says a single-director company cannot claim where that director is the only employee liable for secondary Class 1 NIC.

That is exactly the sort of case where payroll software being set to “yes” can create a wrong claim that later needs reversing.

Worked example 2: husband-and-wife director company that can claim

Assume Tom and Aisha are both directors of the same limited company. Each takes a salary of £12,570 in 2026/27.

Employer NIC-able pay for each director:

- £12,570 - £5,000 = £7,570

Employer NIC per director at 15%:

- £7,570 x 15% = £1,135.50

Combined employer NIC:

- £1,135.50 x 2 = £2,271.00

Because both directors are above the annual secondary threshold, HMRC’s additional employee test is met. In that simple example, the company can usually claim Employment Allowance and reduce the £2,271.00 employer NIC bill to nil for the year, with plenty of the £10,500 allowance still unused.

One caveat though. Do not force salary decisions just to fit a relief headline. A higher second salary may affect Income Tax, employee NIC, pension planning, or the wider extraction mix. You need the numbers done together, not one rule looked at in isolation.

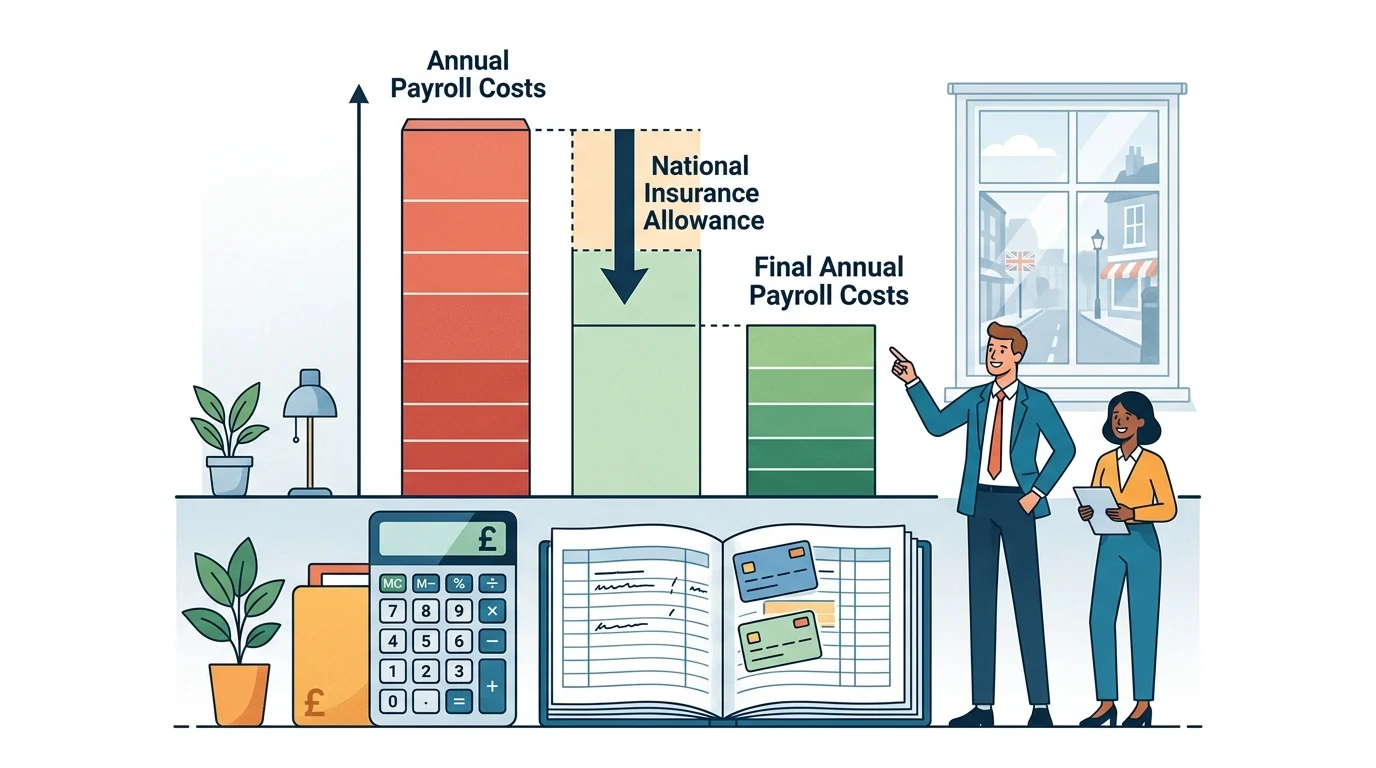

How much can Employment Allowance actually save a small employer?

HMRC says Employment Allowance can reduce your annual employer NIC liability by up to £10,500. For many small employers, that can cover the full Class 1 employer NIC bill. For slightly larger employers, it can still take a useful chunk out of it.

The practical point is easier to see with a payroll example than with another paragraph.

Worked example 3: small team payroll where the full allowance is used

Assume a business has 4 employees, each earning £30,000 a year, all on normal category A NIC.

Employer NIC-able pay per employee:

- £30,000 - £5,000 = £25,000

Employer NIC per employee at 15%:

- £25,000 x 15% = £3,750

Total annual employer NIC for 4 employees:

- £3,750 x 4 = £15,000

Employment Allowance available:

- £10,500

Employer NIC left to pay after the allowance:

- £15,000 - £10,500 = £4,500

That is not a marginal saving. It cuts the employer NIC bill by 70% in this example.

You can also turn that into a monthly cash-flow picture. If the business would otherwise average about £1,250 of employer NIC a month, the allowance covers the first £10,500, so the NIC payments are reduced until the allowance is used up. On rough numbers, that could mean around the first 8 months of employer NIC are covered in full, then the business starts paying again later in the tax year.

How to claim Employment Allowance through payroll software

HMRC says you claim Employment Allowance by submitting an Employment Payment Summary (EPS). If you use your own payroll software, you put “Yes” in the Employment Allowance indicator field the next time you send an EPS. If your software does not support that field, you can use HMRC’s Basic PAYE Tools.

The sequence is usually:

- Check eligibility for the current tax year.

- Turn on the Employment Allowance indicator in payroll software.

- Submit the next EPS to HMRC.

- Let the software offset the allowance against employer Class 1 NIC as payroll runs through the year.

HMRC also says you need to claim Employment Allowance every tax year. That point matters. We still see businesses assume last year’s claim simply rolls on. HMRC’s current guidance says to treat the claim as a new annual step.

If you stop being eligible, HMRC says you should select “No” in the indicator field in the next EPS. It also says not to switch it off just because you have already used the full £10,500 for the year. Using it up does not make you ineligible. It just means the relief has done its job for that tax year.

Worked example 4: late claim in September 2026

Assume an eligible employer forgets to claim from April and only notices in September 2026. By then, it has paid £4,800 of employer Class 1 NIC for the year.

Remaining allowance still available for 2026/27:

- £10,500

NIC already paid:

- £4,800

Once the claim goes in, HMRC says late claim cases can be dealt with by using the allowance against amounts owed or by refund after year end if nothing is owed. So the business has not lost the relief completely, but it has lost the earlier cash-flow benefit from April to September.

That is why we would rather see the claim checked in the first payroll review of the tax year, not left until half the year has gone.

Common Employment Allowance mistakes we are seeing in April 2026

Most of the problems are not technical. They come from assumptions.

Assuming the old £100,000 limit still blocks the claim

HMRC says that from April 2025, employers paying more than £100,000 in Class 1 NIC can apply for Employment Allowance. A lot of businesses still have the old rule stuck in their heads.

Confusing “more than one person in the company” with the actual test

The single-director restriction is about who is liable for secondary Class 1 NIC, not about whether there is a spouse helping in the office or an admin worker below the threshold.

Claiming across connected companies

HMRC says if you are part of a connected group, only one company in the group can claim the allowance. That is easy to miss where payrolls are run separately.

Forgetting that each tax year needs its own claim

HMRC’s current guidance says you need to claim Employment Allowance every tax year. If the indicator is not checked and the EPS is not sent correctly, the allowance does not simply appear by magic.

Treating payroll software as the final word on eligibility

Software is good at maths. It is not always good at judgement. If the input facts are wrong, the claim can still be wrong.

When it is worth getting someone to review the claim

You do not need an accountant to tick every payroll box. You probably do need someone to review things if any of the following apply:

- you are a director-led company with one or two people on payroll

- your group has connected companies or multiple PAYE schemes

- you moved staff pay levels around at the start of the tax year

- you are not sure whether more than half your work is in the public sector

- you are trying to balance salary, dividends, and pension contributions at the same time

That last point matters more than it might seem. Employment Allowance is only one line in the payroll picture. A claim that looks clever on its own can still be the wrong wider move if it pushes up Income Tax or changes the way you draw money from the company.

If you want the clean answer without spending your Friday afternoon inside HMRC guidance, get in touch. We can review the payroll facts, tell you whether the claim is available, and make sure it is reflected properly in the numbers.

FAQ: Employment Allowance UK 2026/27

How much is Employment Allowance in 2026/27?

HMRC says Employment Allowance for 2026/27 is up to £10,500.

Do I need to claim Employment Allowance every year?

Yes. HMRC says you need to claim Employment Allowance every tax year.

How do I claim Employment Allowance?

You usually claim by putting “Yes” in the Employment Allowance indicator field and sending an EPS through your payroll software.

Can a single-director company claim Employment Allowance?

Usually not, if the director is the only employee liable for secondary Class 1 National Insurance. That is one of HMRC’s clearest restrictions.

Can companies with more than one director claim it?

Often yes, if more than one employee or director is above the secondary threshold and the other rules are met. HMRC says that can make the company eligible for the whole tax year.

Can connected companies both claim Employment Allowance?

No. HMRC says only one company in a connected group can claim.

What if I claim late in the tax year?

You can still claim during the year, though the cash-flow benefit arrives later. HMRC says unclaimed allowance may be used against tax or National Insurance owed, or refunded after year end if nothing is owed.

Your next step

Pull your April payroll settings, check who is actually above the £5,000 annual secondary threshold, and confirm whether the EPS claim has been made for 2026/27. That one review will usually tell you whether you are missing a relief worth up to £10,500, or whether you need to switch off a claim that should never have been there in the first place.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

Employer National Insurance and Payroll Changes UK 2026/27: Small Business Checklist

Employer National Insurance and payroll changes UK 2026/27 explained with rates, deadlines, and worked cost examples for small employers.

How to Run Payroll for the First Time in the UK: New Employer Checklist for 2026

Learn how to run payroll for the first time in the UK, from HMRC registration and pensions to PAYE deadlines, costs, and first payday checks.

PAYE Deadline 22 May 2026: What Happens If You Pay HMRC Late?

PAYE deadline 22 May 2026 explained for UK employers, with late payment penalties, interest, Time to Pay options, and worked examples.