How to Run Payroll for the First Time in the UK: New Employer Checklist for 2026

Learn how to run payroll for the first time in the UK, from HMRC registration and pensions to PAYE deadlines, costs, and first payday checks.

How to Run Payroll for the First Time in the UK: New Employer Checklist for 2026

The first payroll run is usually where a new employer realises that hiring someone is not just about agreeing a salary. If you want to know how to run payroll for the first time in the UK, you need the PAYE scheme in place, the employee set up properly, pension duties checked, and HMRC deadlines in your diary before the first payday lands.

Most of the stress comes from doing these jobs in the wrong order. Owners often focus on the payslip, then discover they still need a PAYE reference, a starter checklist, or a pension setup that should have been sorted earlier. That is fixable. The process is not especially hard, but it does punish last-minute improvising.

Quick summary: register as an employer before the first payday, choose payroll software or an outsourced provider, collect the employee’s starter information, run payroll and send the FPS on or before payday, check workplace pension duties from the employee’s first day, and pay HMRC by 22 May 2026 for April payroll liabilities if you pay electronically.

If you want the first run checked before money goes out, we can help through our payroll services, bookkeeping service, and contact page.

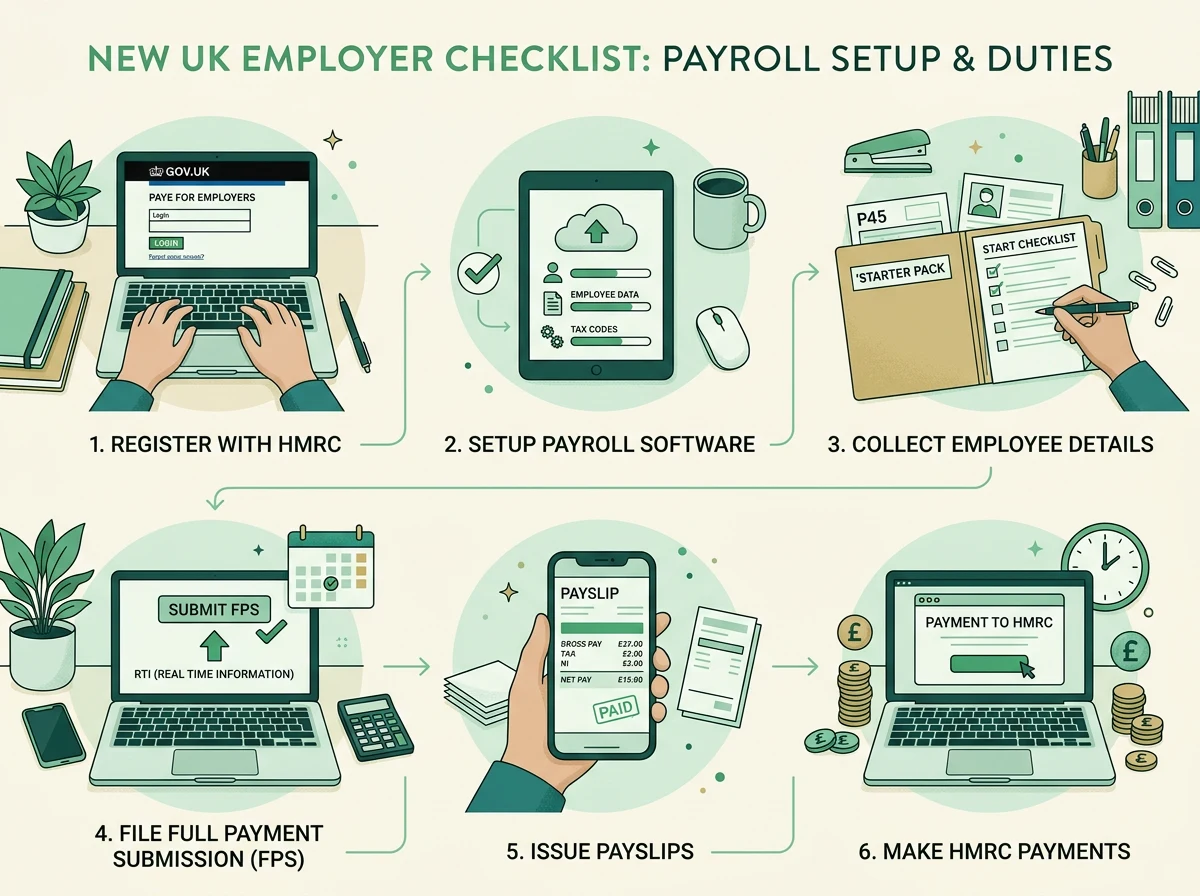

How to run payroll for the first time in the UK: the order that works

The basic sequence is simpler than many first-time employers expect:

- Register as an employer with HMRC.

- Decide whether you are running payroll yourself or paying a provider.

- Gather your employee’s payroll details before they are paid.

- Check workplace pension duties from the employee’s first day.

- Run payroll, issue the payslip, and send the Full Payment Submission, or FPS, on or before payday.

- Pay HMRC on time and file any Employer Payment Summary, or EPS, that applies.

HMRC says you must register before the first payday, and you cannot register more than 2 months before you start paying people. If your PAYE reference has not arrived in time, you can still run payroll, store the FPS, and submit a late FPS once you have the reference. HMRC also makes the point that even if you pay a payroll provider to do the work, you are still legally responsible for PAYE compliance. Register as an employer and choose how to run payroll.

That last point matters more than it sounds. Outsourcing payroll is often a good idea, especially when this is your first employee, but it does not transfer the legal duty. If dates are missed or starter information is wrong, HMRC will still regard it as your payroll.

Register as an employer before you start thinking about payslips

If you are employing staff for the first time, this is the job to do first. You normally need to register as an employer with HMRC when you start employing staff. HMRC says you must also register if you are only employing yourself, for example as the only director of a limited company.

This is where plenty of businesses lose a week for no good reason. They assume they can get the paperwork moving after the employee has started. In reality, the PAYE reference is the anchor for the whole process, from software setup to pension declaration.

Here is the practical rule:

| Task | Timing | Why it matters |

|---|---|---|

| Register as an employer with HMRC | Before first payday | You need your PAYE reference to file payroll normally |

| Earliest you can register | No more than 2 months before first payday | HMRC will not let you register too far in advance |

| If PAYE reference has not arrived | Run payroll, store FPS, send late FPS once reference arrives | This avoids delaying wages unnecessarily |

One more point worth keeping in view. If you are a limited company with just one director and no one else on payroll above the secondary NIC threshold, the Employment Allowance rules are often less generous than owners expect. HMRC says a company with only one director cannot claim Employment Allowance if that director is the only employee liable for employer’s National Insurance. Once you take on another employee who is paid above the threshold, the position can change. That is one reason first payroll is a useful moment to review the company setup rather than repeating last year’s director-only arrangement by habit.

If you are already comparing costs of taking on staff, our employer National Insurance guide for 2026/27 is a good companion piece.

Choose payroll software or outsource it, but decide before the employee starts

HMRC gives you two broad choices. You can run payroll yourself using software, or you can pay a payroll provider to do it for you. For a one-person team, both routes can work. The deciding factor is usually how much admin discipline you already have.

Running it yourself can be fine if:

- you have one or two employees

- pay is straightforward

- you are comfortable checking deadlines every month

- you are happy learning how FPS and EPS reporting works

Outsourcing usually makes more sense if:

- directors, staff, and benefits are all mixed together

- pay changes often because of overtime, bonuses, or commission

- you do not want to deal with pension letters, starter declarations, and corrections yourself

- bookkeeping is already behind and payroll would be another loose end

HMRC keeps a list of recognised payroll software, including free options for businesses with fewer than 10 employees. That can be useful if you want a low-cost start. Even so, software does not remove judgement. You still need the right tax code basis, the right pension treatment, and the right payment date.

The thing that trips up first-time employers is not usually the software screen. It is missing information before they open it.

Get the employee details before the first pay run, not after

To put someone on payroll properly, you need starter information first. If the employee has a recent P45, you will normally use that. If they do not, HMRC says they should complete the starter checklist, which replaced the old P46. On the first FPS, you register the new employee by including their details the first time you pay them.

You will usually need:

- full name

- address

- date of birth

- National Insurance number, if available

- start date

- bank details for payment

- P45 details, if they have one

- starter checklist details if they do not have a usable P45

- student loan or postgraduate loan information if relevant

HMRC says you must keep this payroll information for the current tax year and the 3 following tax years. The record-keeping part is dull, but it matters when somebody queries tax, statutory pay, or year-end figures later on. Get employee information and starter checklist guidance.

It is also worth separating payroll setup from general hiring paperwork. Right-to-work checks, the written statement of employment particulars, and employers’ liability insurance all matter, but they are not substitutes for starter payroll data. GOV.UK says employers’ liability insurance should be in place as soon as you become an employer, with cover of at least GBP 5 million, and the penalty can be GBP 2,500 a day if you are not properly insured. Employers’ liability insurance.

What happens on payday itself

Right, so here is the part people usually mean when they say “run payroll”.

On or before payday, your payroll process should do five things:

- record gross pay

- work out deductions such as Income Tax and National Insurance

- work out employer’s National Insurance

- produce the payslip

- send the FPS to HMRC on or before the payment date

HMRC says employees must get a payslip on or before payday. It also says the FPS should be sent on or before payday, even if you pay HMRC quarterly rather than monthly. If you find a mistake quickly, you usually correct it through a corrected FPS or the next regular report, depending on what went wrong and when you spotted it. Running payroll: FPS and payslips.

For 2026/27, some of the figures most new employers need are:

| Item | 2026/27 figure |

|---|---|

| Employee NIC primary threshold | GBP 12,570 a year |

| Employer NIC secondary threshold | GBP 5,000 a year |

| Main employer NIC rate | 15% |

| Employment Allowance | Up to GBP 10,500 for eligible employers |

| National Living Wage, age 21+ | GBP 12.71 an hour from 1 April 2026 |

| Auto-enrolment earnings trigger | GBP 10,000 a year |

| Qualifying earnings band | GBP 6,240 to GBP 50,270 |

| Minimum employer pension contribution | 3% of qualifying earnings |

Those are the figures that shape the first payroll run far more than most glossy hiring checklists do. If you need a wage-rate refresher, our National Minimum Wage guide for April 2026 covers the hourly bands in detail.

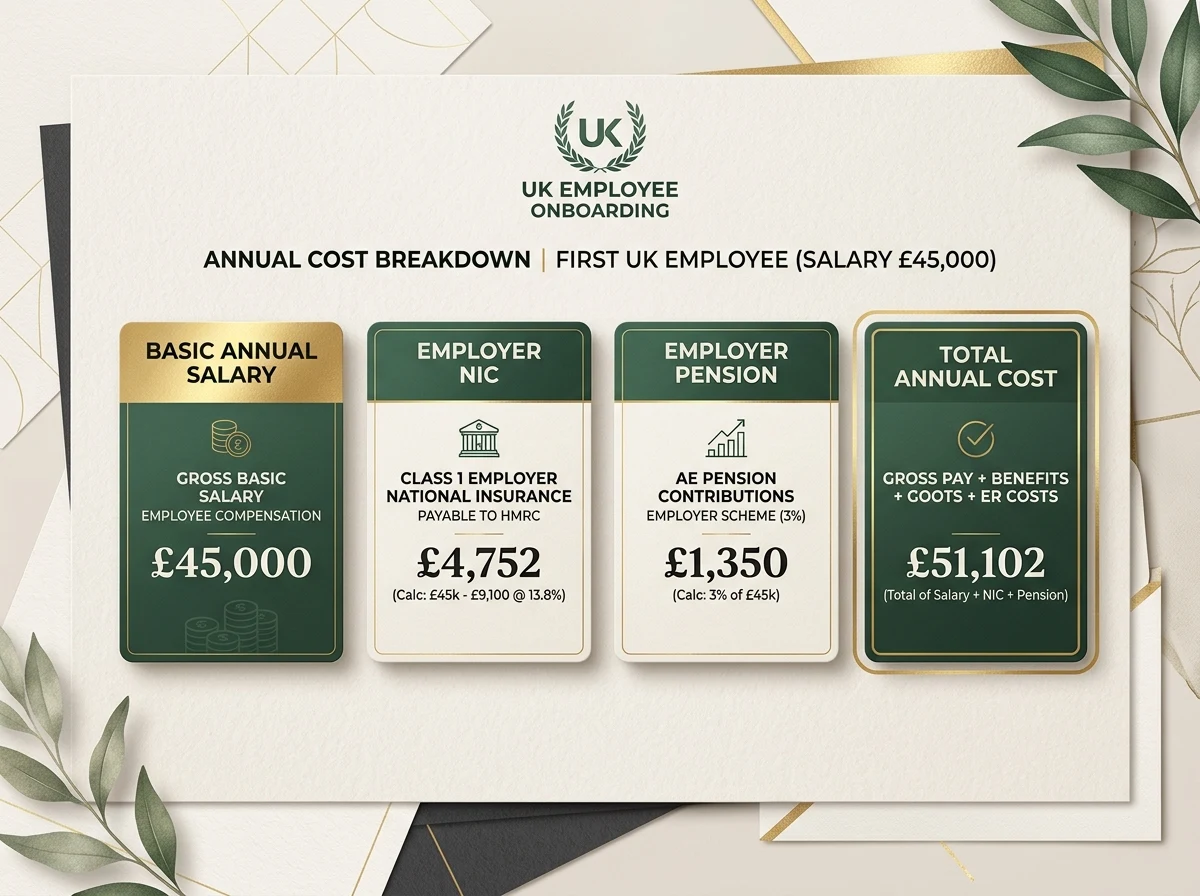

Worked example 1: what one employee on GBP 30,000 actually costs

Assume you hire one employee on a salary of GBP 30,000 for 2026/27 and they are eligible for automatic enrolment. Ignore holiday accrual and software fees for the moment so we can see the tax and pension core clearly.

Employer’s National Insurance

Employer NIC is due on earnings above the GBP 5,000 annual secondary threshold.

- salary: GBP 30,000

- less secondary threshold: GBP 5,000

- NIC-able amount: GBP 25,000

- employer NIC at 15%: GBP 3,750

Minimum employer pension contribution

Under most automatic enrolment setups, qualifying earnings run from GBP 6,240 to GBP 50,270.

- salary: GBP 30,000

- less lower qualifying earnings limit: GBP 6,240

- qualifying earnings: GBP 23,760

- employer contribution at 3%: GBP 712.80

Headline annual employer cost before other staff costs

- gross salary: GBP 30,000

- employer NIC: GBP 3,750

- minimum employer pension: GBP 712.80

- total: GBP 34,462.80

That total usually surprises owners who have only budgeted for salary. Once you add paid holiday, software, insurance, training time, and the odd payroll correction that eats half an afternoon, the real cost is higher.

Your own figures may differ if you can claim Employment Allowance, the employee is under 21, or pension contributions are calculated on a different basis under your scheme. Even so, this kind of rough costing is the right place to start. Better to be mildly annoyed by the maths now than shocked by it later.

Workplace pension duties start on day one, not when you get around to them

The Pensions Regulator says your automatic enrolment duties start from the day your first member of staff starts working. That is your duties start date. Even if you think the employee will not need to be put into a pension scheme straight away, you still have duties.

For most small employers, the key tests are:

- is the worker aged between 22 and State Pension age

- do they earn at least GBP 10,000 a year, or the pay-period equivalent

- do they normally work in the UK

If the answer is yes, you generally need to enrol them and make an employer contribution. If they are not eligible straight away, you still need to assess them. The Pensions Regulator says you must write to staff no later than 6 weeks after the duties start date, and the declaration of compliance must be completed within 5 months. Duties for new employers and declaration deadline.

The minimum contribution structure is still the familiar one:

- total minimum contribution: 8%

- minimum employer contribution: 3%

- usual employee share: 5%, including tax relief mechanics under the scheme

Worked example 2: part-time employee at the National Living Wage

Assume your first employee is aged 23, works 20 hours a week, and is paid the April 2026 National Living Wage of GBP 12.71 an hour.

Annual gross pay:

- 20 x 52 x GBP 12.71 = GBP 13,218.40

That salary is above the GBP 10,000 auto-enrolment trigger, so pension duties will usually apply.

Qualifying earnings:

- GBP 13,218.40 - GBP 6,240 = GBP 6,978.40

Minimum employer pension contribution:

- 3% x GBP 6,978.40 = GBP 209.35

Employer NIC:

- NIC-able earnings: GBP 13,218.40 - GBP 5,000 = GBP 8,218.40

- employer NIC at 15%: GBP 1,232.76

Headline annual employer cost before holiday and other extras:

- wages: GBP 13,218.40

- employer NIC: GBP 1,232.76

- employer pension: GBP 209.35

- total: GBP 14,660.51

That is a useful reminder that even a genuinely part-time first hire needs a proper payroll budget.

Paying HMRC after the first run

Running payroll and paying HMRC are related, but they are not the same job.

HMRC says you normally pay what you owe by the 22nd of the month if paying electronically, or the 19th if paying by post. If you usually pay less than GBP 1,500 a month, you may be able to pay quarterly instead of monthly. If you need an EPS, for example to claim Employment Allowance or recover statutory payments, HMRC says it should usually be sent by the 19th of the following tax month for the reduction to be reflected against what you owe. Paying HMRC and EPS reporting.

For a first employer with an April payroll, the practical calendar often looks like this:

| Date | Action |

|---|---|

| Before payday | Run payroll and send FPS |

| On or before payday | Give the employee a payslip |

| By 19 May 2026 | Send EPS if you need to claim reductions for April liabilities |

| By 22 May 2026 | Pay HMRC electronically for April PAYE liabilities |

Worked example 3: why the monthly HMRC bill can feel bigger than expected

Assume you pay one employee GBP 2,500 a month and the annual figures stay consistent through the year.

Using the same annual position as our GBP 30,000 salary example:

- annual employer NIC: GBP 3,750

- rough monthly employer NIC: GBP 312.50

- annual employer pension at minimum: GBP 712.80

- rough monthly employer pension: GBP 59.40

Now imagine the employee’s tax and employee NIC deductions also total around GBP 406.70 a month combined, based on their code and pay level.

Your cash movements are now split three ways:

- GBP 2,500 gross salary entering payroll

- employee net pay going to the staff member after deductions

- PAYE/NIC money going to HMRC

- pension money going to the pension provider

That is why first-time employers often say, “I paid the employee, why am I still paying out more this month?” Because payroll is never just the net wage. HMRC and the pension provider are part of the same cycle.

Common first-payroll mistakes we see

The mistakes are not glamorous. They are the same handful again and again:

- registering with HMRC too late

- waiting for a P45 instead of using the starter checklist when needed

- forgetting that pension duties start on the employee’s first day

- sending the FPS after payday without a valid reason

- treating the PAYE payment as optional until “the end of the quarter”

- assuming the Employment Allowance applies automatically

- budgeting only for gross wages and not employer NIC or pension

A slightly more fiddly mistake is using the wrong payment date on the FPS because the payroll was prepared early. HMRC expects the usual payday to be entered even if, say, wages are paid earlier due to a bank holiday. Get that wrong and the report can land in the wrong tax month, which is the sort of boring admin problem that turns into a larger clean-up than it should.

If your bookkeeping is messy, payroll mistakes get worse because there is no clean audit trail for wages, pension, or HMRC liabilities. That is where joined-up bookkeeping matters more than software brand names.

Should you run payroll yourself or get help?

If this is your first employee and you already feel short on time, outsourcing is often the sensible move. You can still keep visibility over costs and deadlines without personally wrestling every FPS field.

We would usually say DIY payroll is reasonable when:

- pay is fixed

- there are no benefits in kind

- the staff count is tiny

- you do not mind checking HMRC and pension deadlines each month

We would usually say get help when:

- you are a director hiring your first employee and want the salary, pension, and NIC mix checked properly

- staff hours vary

- maternity, sickness, or statutory pay may be involved

- you are already behind on the books

- you want one less compliance job on your plate

Our payroll services can take care of the payroll cycle itself, and our bookkeeping service helps if wage costs, HMRC liabilities, and monthly management numbers are all starting to blur together.

FAQ: how to run payroll for the first time in the UK

Do I need to register as an employer if I am only paying myself as a director?

Usually, yes. HMRC says you must register even if you are only employing yourself, for example as the only director of a limited company.

Can I pay an employee before my PAYE reference arrives?

Yes, if needed. HMRC says you can run payroll, store the FPS, and send a late FPS once your employer PAYE reference arrives.

What if my employee does not have a P45?

Use the starter checklist. HMRC says the starter checklist is used when an employee does not have a P45 or the new employer needs more information.

When do I send the first FPS?

HMRC says the FPS should be sent on or before payday, even for the first payroll run.

When do I need to write to staff about workplace pensions?

The Pensions Regulator says you must write to staff no later than 6 weeks after the duties start date.

When do I need to complete the declaration of compliance?

The declaration of compliance must normally be completed within 5 months of the duties start date.

Do I have to pay HMRC every month?

Usually, yes. HMRC says PAYE liabilities are normally paid monthly, though employers with PAYE bills usually below GBP 1,500 a month may be able to arrange quarterly payments.

The practical next step

If your first employee is starting soon, do three things this week: register the PAYE scheme, choose who is actually running payroll, and get the pension setup checked before day one. That gets the critical admin done in the right order. If you want a second pair of eyes before the first payday, speak to us. It is much easier to review a payroll before it goes out than to repair it after HMRC, the pension provider, and the employee have all seen different numbers.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

How to Run Payroll for One Employee UK: 2026/27 First Employer Guide

How to run payroll for one employee UK in 2026/27, with PAYE registration, FPS deadlines, employer NI, pensions, and costs.

1257L M1 Tax Code Explained: Emergency Tax Guide for 2026/27

1257L M1 tax code explained for 2026/27, with emergency tax calculations, refund examples, and practical steps to correct your code.

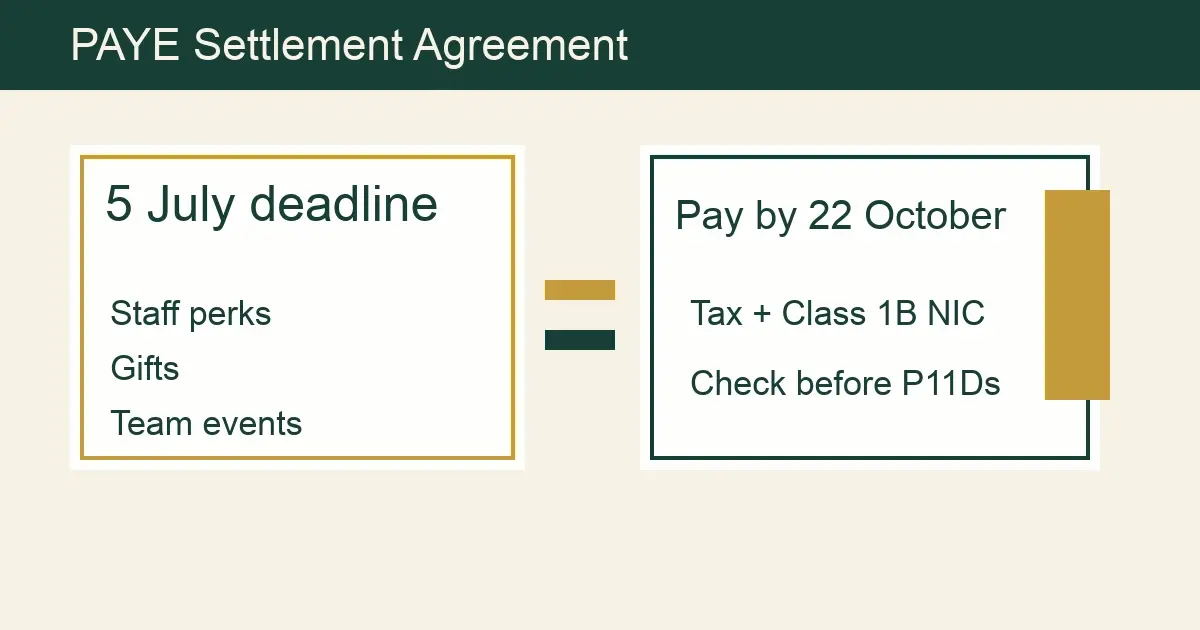

PAYE Settlement Agreement Deadline 5 July 2026: Employer Guide

PAYE Settlement Agreement deadline guide for 2026, with PSA dates, eligible benefits, tax gross-up examples, and employer checklist.