Cash Basis Accounting for Sole Traders 2026: Rules, Examples, and When to Use Traditional Accounting

Cash basis accounting for sole traders in 2026, with current HMRC rules, worked examples, MTD points, and when traditional accounting is better.

Cash Basis Accounting for Sole Traders 2026: Rules, Examples, and When to Use Traditional Accounting

Cash basis accounting for sole traders changed from a small-business option into the normal starting point for many Self Assessment accounts. The old rule of thumb, “cash basis is only for very small traders under £150,000 turnover”, is out of date for current tax years. From 6 April 2024, HMRC says cash basis became the standard way to record income and expenses if you are a sole trader or a partnership without corporate partners, unless you choose traditional accounting instead.

That sounds simpler than it feels in real bookkeeping. Cash basis changes when income and costs appear in your tax calculation. It can help if customers pay late, but it can also hide unpaid invoices, supplier bills, stock movements, and finance needs. With Making Tax Digital for Income Tax now in force for the first group of sole traders from 6 April 2026, the choice matters because your software, quarterly updates, and year-end tax return all need to tell the same story.

Quick summary: cash basis usually records income when you receive money and expenses when you pay them. Traditional accounting records income and costs when they are earned or incurred, even if cash moves later. Cash basis is now the standard method for eligible sole traders and partnerships without corporate partners, but traditional accounting may still be better if you carry stock, need bank finance, have unpaid work at year end, or want accounts that show a fuller trading picture.

If you are setting up or cleaning up your records, we can help through our bookkeeping service, Self Assessment support, and self-employment tax advice.

Cash basis accounting for sole traders: the 2026 rule in plain English

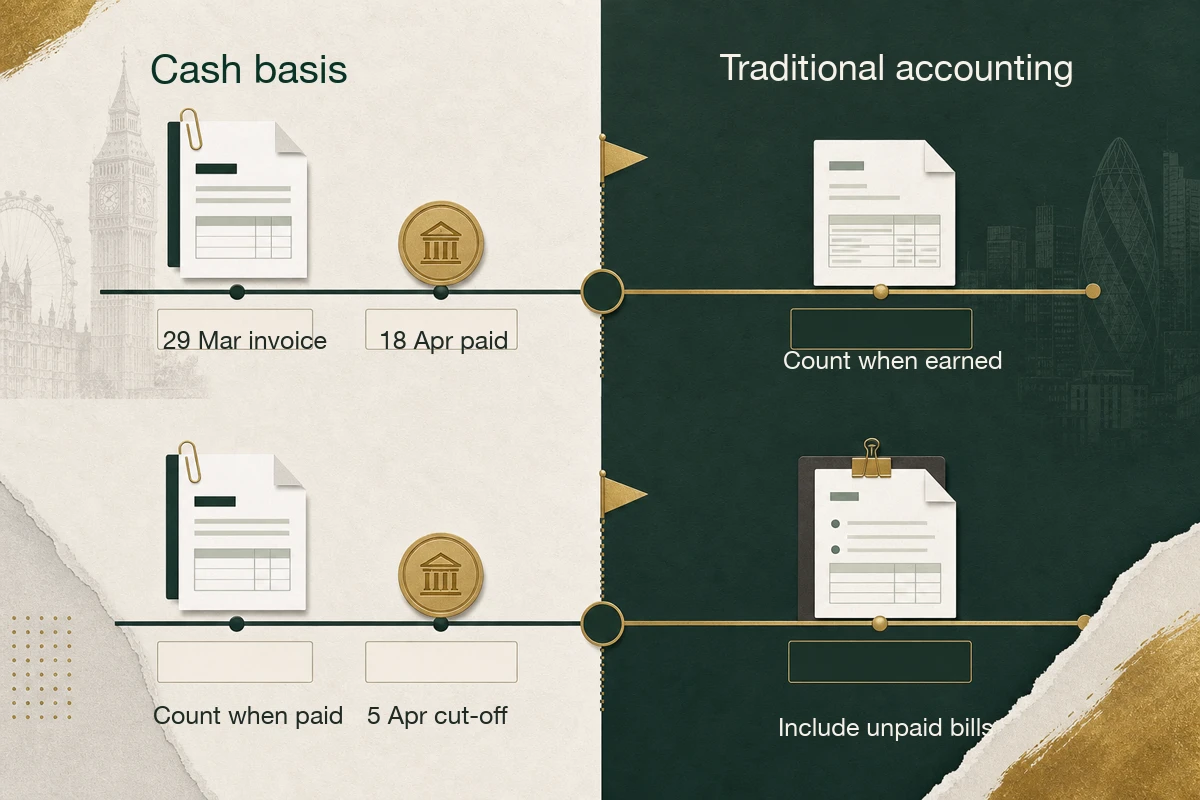

Under cash basis accounting, you usually count business income when the money is actually received. You usually count expenses when the money is actually paid. If you invoice a customer on 28 March 2027 and they pay on 20 April 2027, the income normally belongs in the 2027/28 tax year under cash basis, not the 2026/27 tax year.

Under traditional accounting, sometimes called accruals accounting, the same invoice normally belongs in the tax year when the work was done and invoiced. The payment date is still important for cash flow, but it does not decide the tax year by itself.

GOV.UK’s cash basis guidance says cash basis is the standard way to record income and expenses if you are a sole trader or partnership without corporate partners. The same guidance says limited companies cannot use it. A limited company prepares company accounts and Corporation Tax returns under different rules, so directors should look at our company accounts service rather than assuming sole trader rules apply.

Here is the core difference.

| Situation | Cash basis | Traditional accounting |

|---|---|---|

| Customer invoice sent but not paid | Not usually counted until paid | Usually counted when invoiced or earned |

| Supplier invoice received but not paid | Not usually claimed until paid | Usually counted when billed or incurred |

| Equipment bought and paid for | Often claimed as a normal business expense, with special rules for cars | Often dealt with through capital allowances |

| Business loan application | May be too thin for a lender because debtors and creditors are missing | Usually gives a fuller view of what is owed and due |

| Tax return choice | Standard method for many eligible traders | You need to say you used traditional accounting |

The practical question is not “which one sounds easier?” It is “which one gives you the right tax result and enough information to run the business?”

Who can use cash basis in 2026?

You can usually use cash basis if you are a sole trader or a partnership without corporate partners. If you run more than one business, HMRC says you can choose whether each business uses cash basis or traditional accounting.

You cannot use cash basis if your business is a:

- limited company

- limited liability partnership

- partnership with one or more corporate partners

HMRC also lists specialist exclusions, including Lloyd’s underwriters, certain farming or creative businesses using averaging, mineral extraction trades, and businesses that have ever claimed research and development allowance. Most freelancers, consultants, trades, local service businesses, online sellers, and small professional firms will not be in those categories, but do not guess if your work sits near a specialist rule.

The key 2026 update is the missing turnover cap. Before the 2024/25 tax year, GOV.UK’s old cash basis page referred to a £150,000 turnover entry limit and a £300,000 exit point. The current cash basis page treats cash basis as the standard method for eligible sole traders and partnerships without corporate partners. That means an old blog post, template, or spreadsheet note mentioning a £150,000 limit may now be misleading.

That said, bigger turnover can still make traditional accounting more useful. A business taking £280,000 a year with stock, deposits, supplier credit, finance agreements, and unpaid invoices may technically be able to use cash basis, but the owner may need accounts that show more than bank movements.

Worked example: unpaid invoices around 5 April

Assume Priya is a freelance designer. Her tax year runs to 5 April 2027. She sends a final project invoice on 29 March 2027:

- project fee: £4,000

- no VAT for this example

- customer pays: 18 April 2027

- Priya’s other paid income in 2026/27: £47,000

- paid expenses in 2026/27: £12,000

Under cash basis, the £4,000 is not usually included in Priya’s 2026/27 income because she had not received it by 5 April. Her 2026/27 profit is:

| Item | Amount |

|---|---|

| Paid income received by 5 April 2027 | £47,000 |

| Paid expenses by 5 April 2027 | £12,000 |

| Cash basis profit | £35,000 |

Under traditional accounting, the March invoice is normally included because the work was done and the invoice was raised before 5 April:

| Item | Amount |

|---|---|

| Income earned or invoiced in 2026/27 | £51,000 |

| Expenses incurred in 2026/27 | £12,000 |

| Traditional accounting profit | £39,000 |

The tax has not disappeared under cash basis. It has moved into the next tax year when the customer pays. That timing can be helpful if cash is tight, but it also means Priya’s tax result depends heavily on payment dates.

Now change the facts. Suppose Priya needs a mortgage or business loan in summer 2027. The lender may want accounts showing work completed, unpaid invoices, and a proper year-end position. A cash basis tax return may not be enough on its own, even if it is valid for HMRC.

What expenses can you claim under cash basis?

The basic rule is simple: only count expenses you have actually paid. GOV.UK’s income and expenses under cash basis guidance gives examples such as day-to-day running costs, admin costs, training costs, things used in the business such as computers and vans, interest and bank charges, and goods bought for resale.

There are still rules. “Paid” does not turn a private cost into a business cost. The expense must still be allowable for tax, and you need records to support it. You also need to split mixed-use costs, such as a phone bill or home office cost, between business and personal use where appropriate.

Equipment is a common difference. Under cash basis, many items you buy to keep and use in the business can be treated as normal allowable expenses when paid. Cars are different. GOV.UK says if you buy a car for your business, you can claim the purchase as a capital allowance, but not if you are using simplified expenses for that vehicle.

Here is a simple equipment example.

Worked example: laptop bought near year end

Assume Omar is a sole trader consultant. He buys and pays for a laptop on 2 April 2027:

- laptop cost: £1,200

- business use: 90%

- private use: 10%

Under cash basis, Omar may be able to claim the business part as an expense because he paid for it before 5 April. The claim would be:

| Calculation | Amount |

|---|---|

| Laptop cost | £1,200 |

| Business use | 90% |

| Allowable expense | £1,080 |

If the laptop was ordered on 2 April but paid on 8 April, the timing may fall into the next tax year under cash basis. That small date difference can affect payments on account and year-end tax planning.

If you regularly buy vans, tools, computers, or equipment around the tax year end, do not rely only on the invoice date. Check the payment date, business-use percentage, and whether any special capital allowance rule applies.

VAT, stock, loans, and other areas where cash basis gets fiddly

Cash basis is not a licence to ignore the shape of the business. It only changes the method used to calculate taxable profit for Self Assessment. Other records still matter.

VAT is the first trap. GOV.UK says VAT-registered businesses using cash basis for Income Tax can record income and expenses either including or excluding VAT, but they must treat income and expenses the same way. If you include VAT in your bookkeeping, VAT payments to HMRC are recorded as expenses and VAT repayments from HMRC are recorded as income. Many businesses find it clearer to keep net amounts and VAT control accounts in software, especially where they already submit VAT returns under Making Tax Digital for VAT.

Stock is another awkward area. A shop, online seller, caterer, or trades business may hold goods at the year end. Cash basis may be simpler for tax, but stock levels still matter for pricing, insurance, gross margin checks, and cash tied up in unsold items. If you buy £18,000 of stock on 30 March and sell most of it in May, cash basis can make the March tax result look very different from the underlying trading pattern.

Finance can also push you towards traditional accounting. A bank may ask for accounts showing debtors, creditors, stock, loans, and work in progress. Cash basis records can be perfectly acceptable for HMRC while still being too thin for a lender, investor, landlord, or grant provider.

There is a timing point with supplier credit too.

Worked example: supplier bill paid after year end

Assume a sole trader electrician receives a materials bill on 31 March 2027:

- materials invoice: £3,600

- payment date: 15 April 2027

- job invoiced and paid by the customer before 5 April

Under cash basis, the income may be counted in 2026/27 because the customer paid before 5 April, but the materials cost may not be claimed until 2027/28 because the supplier was paid after 5 April. That can create a higher profit in the first year and a lower profit in the next year.

Under traditional accounting, the cost would usually be matched to the period it relates to, assuming the materials were used for the March job. That can give a more balanced result.

Neither method is automatically better. The issue is timing. If your income and costs regularly fall either side of 5 April, a quick comparison before filing the return can prevent surprises.

Cash basis and Making Tax Digital for Income Tax

Making Tax Digital for Income Tax does not remove the cash basis question. From 6 April 2026, sole traders and landlords with qualifying income over £50,000 for the 2024/25 tax year need to use MTD for Income Tax if the rest of the conditions apply. The threshold then falls to £30,000 from 6 April 2027 and £20,000 from 6 April 2028, based on the tax years HMRC uses for each phase.

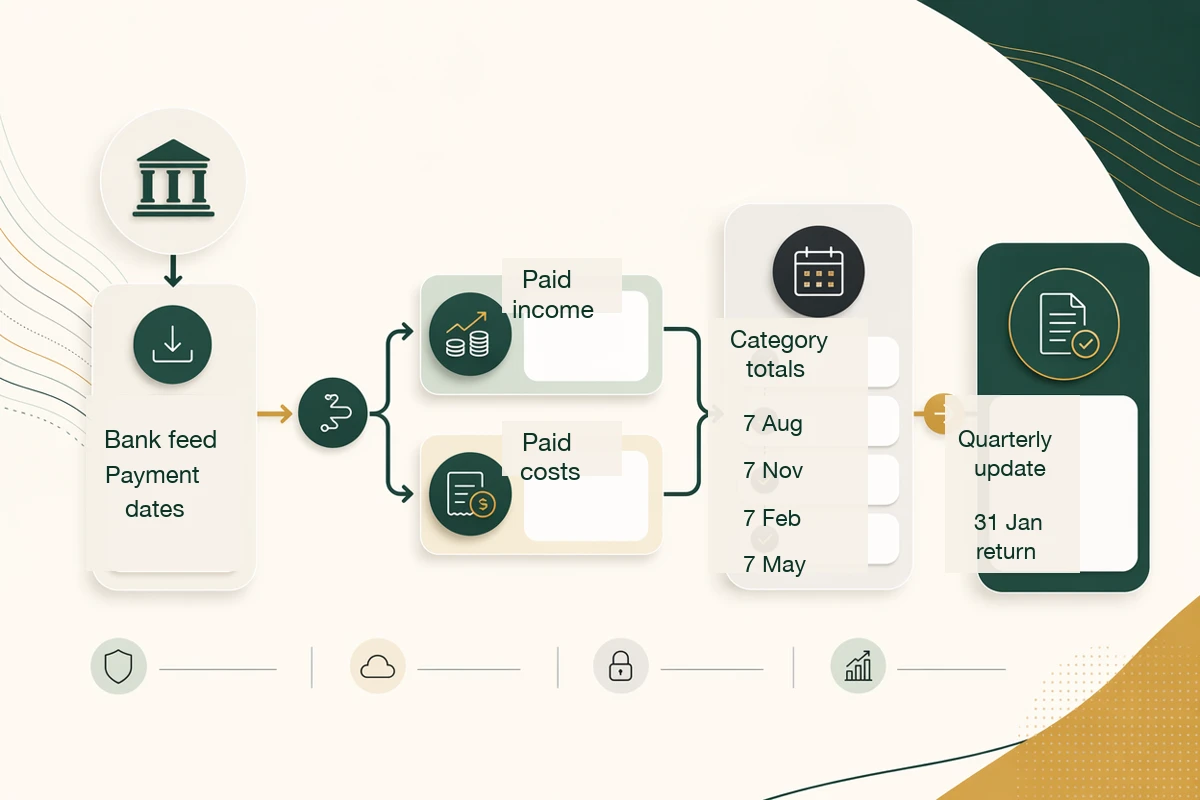

HMRC’s MTD quarterly update guidance says quarterly updates are summaries, not tax returns. Your compatible software sends totals for income and expense categories. HMRC does not receive individual receipts or invoice lines through the quarterly update.

That is useful, but it does not mean quarterly updates can be casual. If your software is on cash basis, payment dates and bank matching become central. If your software is on traditional accounting, invoice dates, bills, debtors, creditors, and year-end adjustments need more care.

The standard MTD update deadlines are:

| Standard update period | Deadline |

|---|---|

| 6 April to 5 July | 7 August |

| 6 April to 5 October | 7 November |

| 6 April to 5 January | 7 February |

| 6 April to 5 April | 7 May after the tax year |

The calendar update periods use 1 April to 30 June, 30 September, 31 December, and 31 March, with the same deadlines. HMRC says you need to choose calendar update periods in your software before sending the first quarterly update, and you cannot change update periods for that tax year after an update has been sent.

For a sole trader using cash basis, the setup checks are practical:

- bank feeds should import the actual payment dates

- card processor payouts should be split from fees where needed

- invoices should be matched to receipts, not left floating

- costs paid personally should be recorded with evidence

- business and private spending should be separated before the quarterly update

- year-end tax adjustments should not be confused with quarterly category totals

Our MTD compatible software guide covers the software choice in more detail. If you are still using spreadsheets, the question is not only whether the spreadsheet can be bridged to HMRC. It is whether it records payment dates, categories, and evidence well enough for cash basis.

When traditional accounting may be better

Traditional accounting can feel like extra admin, but it earns its keep when the business needs a fuller picture.

It may be better where you:

- carry meaningful stock or work in progress

- invoice customers on credit and have large year-end debtors

- receive supplier credit and have large unpaid bills

- need accounts for a mortgage, bank loan, grant, or investor

- want to track gross margin properly

- have deposits, staged jobs, retainers, or long projects

- expect to sell the business or bring in a partner

- want management accounts that show profit earned, not just cash received

Take a trades business with £95,000 of paid receipts, £20,000 of unpaid customer invoices, £11,000 of unpaid supplier bills, and £9,000 of stock at 5 April. Cash basis may produce a tax return from payments alone, but it will not show the owner the true trading position. Traditional accounting can show whether the business is profitable, slow to collect debts, overstocked, or underpricing work.

That does not mean every sole trader should opt out of cash basis. A consultant with low costs, no stock, and customers who pay quickly may get a clean result from cash basis with less year-end adjustment. A landlord with simple rental income and few expenses may also find cash basis workable, although property rules have their own wrinkles.

The sensible approach is to run a quick annual check. If the cash basis profit and traditional accounting profit would be very different, ask why. The reason may tell you more about the business than the tax return does.

Switching between cash basis and traditional accounting

Switching methods can create adjustment issues. HMRC warns that you might have to make adjustments if you switch to traditional accounting. That is because income or expenses could otherwise be counted twice or missed entirely.

Here is a simple example.

Worked example: avoiding a double count when switching

Assume Jade used cash basis in 2025/26. She had an unpaid customer invoice of £2,500 at 5 April 2026, which was not taxed in 2025/26 because the customer had not paid.

Jade switches to traditional accounting for 2026/27. The customer pays the old invoice on 20 April 2026.

If nobody checks the switch, there is a risk the £2,500 is treated incorrectly. Under cash basis it was not taxed in 2025/26. Under traditional accounting, it relates to work done before the new accounting year. The return needs an adjustment so the income is taxed once, not missed and not counted twice.

The same issue can arise with unpaid supplier bills, equipment, capital allowances, VAT treatment, and opening balances in bookkeeping software. This is why switching methods should be a planned year-end decision, not a late-night tax return checkbox.

If you are moving software at the same time, keep a simple bridge schedule:

| Item to check | Why it matters |

|---|---|

| Unpaid sales invoices at the switch date | Avoid missing income or taxing it twice |

| Unpaid supplier bills | Avoid claiming costs in the wrong year |

| Stock and work in progress | Traditional accounts may need opening figures |

| Equipment already claimed | Prevent duplicate claims |

| VAT balances | Keep VAT returns and Income Tax records consistent |

If your records have already become messy, our bookkeeping team can help rebuild the year-end position before the Self Assessment deadline.

A practical checklist before you file

Use this list before submitting a Self Assessment return under cash basis.

| Check | Done |

|---|---|

| Confirm the business is eligible for cash basis | |

| Check whether traditional accounting would give a materially different result | |

| Review unpaid customer invoices at 5 April | |

| Review unpaid supplier bills at 5 April | |

| Check paid expenses are genuinely business costs | |

| Split mixed-use costs between business and private use | |

| Check equipment, cars, and simplified expenses treatment | |

| Reconcile bank, card, and platform receipts | |

| Confirm VAT treatment is consistent if VAT registered | |

| Save evidence for income, receipts, invoices, and adjustments |

The biggest mistake is treating cash basis as “bank statement equals tax return”. It is not that loose. You still need to know what each payment was for, whether it was business or private, whether VAT has been handled correctly, and whether a year-end adjustment is needed.

FAQ: cash basis accounting for sole traders

Is cash basis accounting now the default for sole traders?

For many eligible sole traders and partnerships without corporate partners, yes. GOV.UK says cash basis is the standard way to record income and expenses, unless you choose traditional accounting instead.

Does the old £150,000 cash basis turnover limit still apply?

Not for current tax years from 2024/25 onwards. GOV.UK says the £150,000 entry limit applied before the 2024/25 tax year. Current guidance does not use that old entry limit for eligible sole traders and partnerships without corporate partners.

Can a limited company use cash basis accounting?

No. GOV.UK says limited companies cannot use cash basis for this Self Assessment method. Limited companies prepare company accounts and Corporation Tax returns under company tax rules.

Is cash basis better if customers pay late?

It can help because you usually do not pay Income Tax on unpaid customer invoices until the money is received. It may still be a poor fit if you need accounts showing debtors, stock, creditors, or a fuller profit picture.

Can I use cash basis with Making Tax Digital for Income Tax?

Yes, if you are eligible and your software is set up correctly. MTD quarterly updates send category totals from your digital records. Cash basis means the payment dates and matching process need to be reliable.

Should I choose traditional accounting instead?

Consider it if your business has stock, unpaid invoices, supplier credit, long projects, finance applications, or management reporting needs. Your specific situation may differ, so check the numbers before filing.

The decision to make before the return

Before you file, compare the cash basis result with what traditional accounting would show. If the difference is small and your records are simple, cash basis may be the cleanest route. If the difference is large, do not ignore it. The gap is telling you something about unpaid work, supplier credit, stock, or cash-flow timing.

For a straightforward sole trader, the answer can be settled in an hour with bank records, unpaid invoice lists, supplier bills, and the previous tax return. If you are not sure which method fits, send us the records before you press submit. The tax return is easier to fix before it is filed.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

Traditional Accounting vs Cash Basis: 2026/27 Guide for Sole Traders

Traditional accounting vs cash basis explained for 2026/27, with examples, MTD checks, stock, debtors, and tax timing.

MTD Compatible Software for Sole Traders: 2026 Setup Guide

MTD compatible software for sole traders explained: what HMRC expects, how to choose tools, and what to test before quarterly updates.

MTD Quarterly Update Deadline 7 August 2026: Sole Trader and Landlord Guide

MTD quarterly update deadline 7 August 2026 explained for sole traders and landlords, with records, examples, and filing steps.