Traditional Accounting vs Cash Basis: 2026/27 Guide for Sole Traders

Traditional accounting vs cash basis explained for 2026/27, with examples, MTD checks, stock, debtors, and tax timing.

Traditional Accounting vs Cash Basis: 2026/27 Guide for Sole Traders

Traditional accounting vs cash basis is no longer a small technical choice hidden at the back of a tax return. For most sole traders and ordinary partnerships, cash basis is now the standard way to work out taxable profit. You can still choose traditional accounting, but you need a reason for doing it and clean records to support the choice.

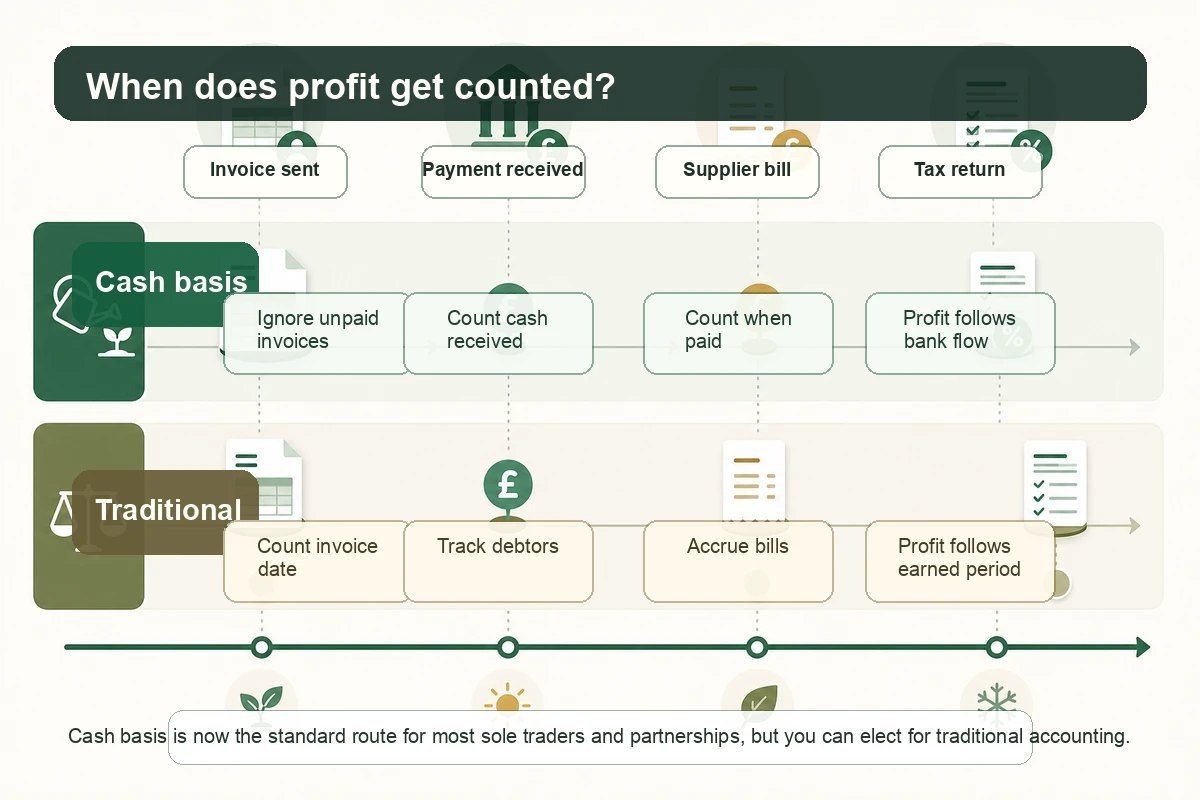

The point is simple enough. Cash basis follows money actually received and paid. Traditional accounting follows invoices, bills, stock, debtors, and creditors. The tax bill can change from one year to the next because the timing is different, even when the long-term profit is the same.

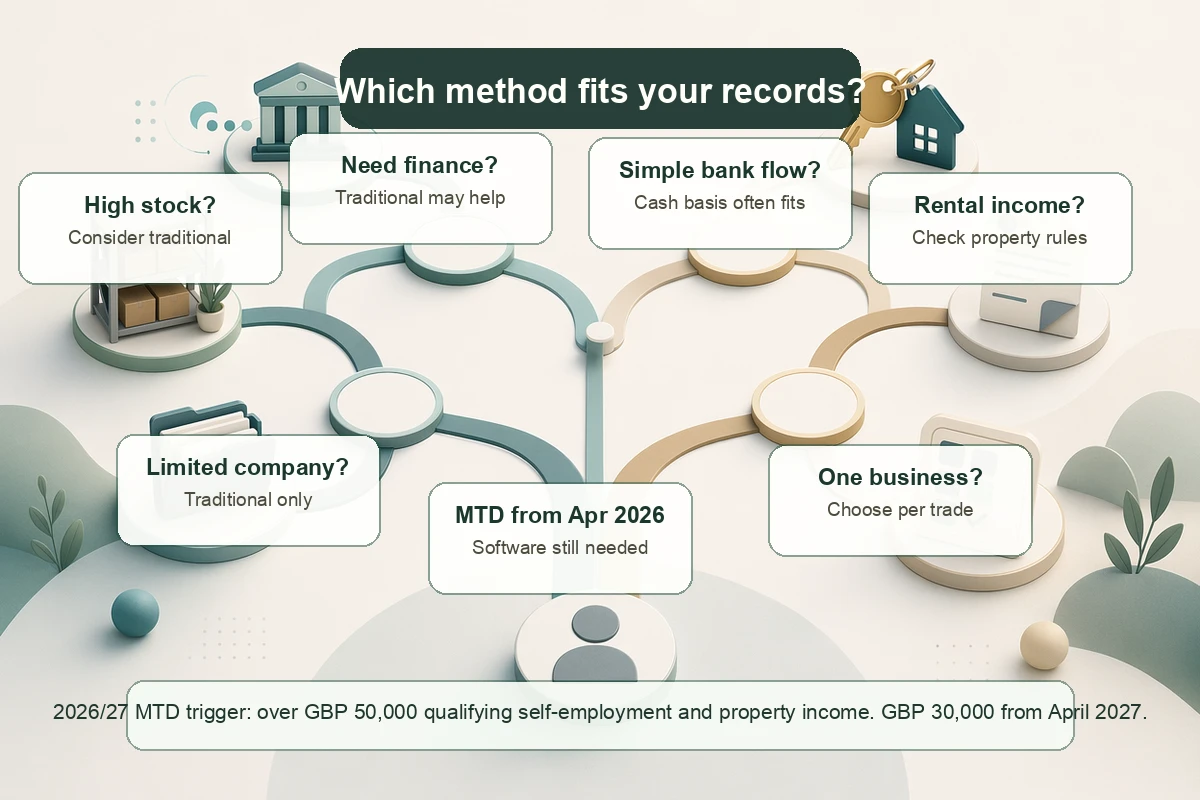

Quick summary: for 2026/27, most sole traders and partnerships without corporate partners can use cash basis as the normal route. Limited companies, limited liability partnerships, and partnerships with corporate partners cannot use it. Traditional accounting can still be better where you have high stock, unpaid customer invoices, grant or loan applications, complex finance, or accounts that need to show what the business has earned rather than what has landed in the bank.

If your records are already drifting between invoices, bank payments, VAT, and Self Assessment, start with the bookkeeping rather than the tax return. Our bookkeeping service, self assessment support, and self-employment tax help can help you choose the right method and keep it consistent.

Traditional accounting vs cash basis: the core difference

Cash basis records income when you receive money and expenses when you pay them. If a client pays you on 10 April 2026 for an invoice raised on 25 March 2026, cash basis normally puts that income into the 2026/27 tax year because the cash arrived after 5 April.

Traditional accounting, sometimes called accruals accounting, records income when it is earned and expenses when they relate to the period, even if money moves later. The same March invoice would usually sit in the year to 5 April 2026 because the work was billed before the year end.

GOV.UK says cash basis accounting is the standard method for sole traders and partnerships without corporate partners. It also says you can choose traditional accounting instead, particularly where the business is more complex or needs finance.

That matters because the method affects more than a box on the SA103 self-employment pages. It affects when income is taxed, when expenses are relieved, how you treat stock, how you explain your numbers to a lender, and how easy your bookkeeping is under Making Tax Digital for Income Tax.

| Question | Cash basis | Traditional accounting |

|---|---|---|

| When is income counted? | When money is received | When the invoice or earning period belongs |

| When are expenses counted? | When the bill is paid | When the cost belongs to the period |

| Does it track unpaid invoices? | Not for taxable profit until paid | Yes, as debtors |

| Does it track unpaid supplier bills? | Not for taxable profit until paid | Yes, as creditors |

| Can limited companies use it? | No | Yes, traditional accounts are expected |

| Is it simpler for a small sole trader? | Often yes | Sometimes, but more records are needed |

Right, so cash basis is easier for many small businesses because the bank feed does more of the heavy lifting. Easier does not always mean better. If your bank account does not tell the full story, traditional accounting may give a truer picture.

Who can use cash basis in 2026/27?

You can usually use cash basis if you are a sole trader or a partnership without corporate partners. If you run more than one business, GOV.UK says you can choose cash basis or traditional accounting for each business.

You cannot use cash basis if the business is a limited company, a limited liability partnership, or a partnership with one or more corporate partners. Some specialist businesses are also excluded, including Lloyd’s underwriters, some farming businesses with certain elections, mineral extraction trades, and businesses that have claimed certain allowances.

Before 6 April 2024, there were turnover limits for using cash basis. GOV.UK’s current guidance says those older limits applied before the 2024/25 tax year. Since 6 April 2024, cash basis has become the default method for many self-employed businesses, which is why older articles and old spreadsheet templates can be misleading.

For a straightforward consultant, designer, tradesperson, tutor, online seller, or freelance professional, cash basis may be perfectly sensible. The warning sign is when the bank account no longer tells the whole story.

Watch for these points:

- you carry meaningful stock at the year end

- customers owe you large unpaid invoices

- you owe suppliers for work already done

- you need accounts for a mortgage, loan, grant, or investor

- you have hire purchase, finance leases, or other asset finance

- you are close to Making Tax Digital for Income Tax thresholds

- you may incorporate soon and need cleaner opening figures

That last one is easy to miss. A sole trader using cash basis can be fine for tax, then hit extra work when moving into a limited company because the company accounts need a fuller opening position.

Worked example 1: same invoices, different taxable profit

Assume a freelance designer has these figures for the 2026/27 tax year:

- invoices raised during the year: £60,000

- cash received from customers by 5 April 2027: £48,000

- unpaid customer invoices at 5 April 2027: £12,000

- bills paid by 5 April 2027: £18,000

- further supplier bills relating to the year but unpaid at 5 April: £4,000

Under cash basis, the taxable profit is based on money received and paid:

| Cash basis item | Amount |

|---|---|

| Cash received | £48,000 |

| Less bills actually paid | £18,000 |

| Taxable profit | £30,000 |

Under traditional accounting, the profit follows the invoices and costs for the year:

| Traditional accounting item | Amount |

|---|---|

| Invoices raised | £60,000 |

| Less costs for the year, including unpaid supplier bills | £22,000 |

| Taxable profit | £38,000 |

The difference is £8,000 of taxable profit. That is not a permanent tax saving under cash basis. The unpaid customer invoices will usually be taxed when the customer pays. The unpaid supplier bills will usually be relieved when paid. Cash basis has shifted the timing.

For a business owner, timing still matters. If the unpaid invoices are large and customers pay slowly, cash basis can stop you paying tax on money you have not received. That is a very real cash-flow benefit.

When cash basis works well

Cash basis is often a good fit where income and costs are simple, payment dates are easy to trace, and stock is low.

Good-fit examples include:

- a consultant paid soon after sending invoices

- a tutor paid by bank transfer before or after each lesson

- a tradesperson with modest materials and clear customer payments

- a freelancer with low overheads and few unpaid bills

- a small landlord with rent paid monthly and simple property costs

- a service business using one business bank account and monthly reconciliation

GOV.UK’s page on recording income and expenses under cash basis says you only record income actually received and only count expenses you have actually paid. It also says payments can include cash, card, cheque, payment in kind, or another method.

That sounds tidy, and it can be. The catch is consistency. You cannot treat one payment as received when it hits the bank, then use the date the customer pressed “send” for another because it feels more convenient. Pick a method and keep it steady.

Cash basis can also reduce year-end admin. Instead of listing every unpaid invoice and every outstanding supplier bill, you start from money movement. For micro-businesses with regular bank reconciliation, that can make Self Assessment less painful.

There is a VAT wrinkle though. VAT-registered businesses can record income and expenses including or excluding VAT, but they need to treat income and expenses consistently. VAT returns have their own rules, and the VAT Cash Accounting Scheme is a separate topic. Our VAT Cash Accounting Scheme guide explains that distinction.

When traditional accounting is the better choice

Traditional accounting is usually better when the business needs a fuller financial picture. Banks, mortgage lenders, grant bodies, and buyers may want to see sales earned, costs incurred, debtors, creditors, stock, and profit margins. A bank statement alone may not satisfy them.

Traditional accounting may suit you if:

- stock levels are material

- customers pay well after invoices are raised

- supplier bills arrive before or after the year they relate to

- you need accounts for a mortgage or business loan

- you want monthly management accounts that show true trading performance

- the business has deposits, prepayments, or deferred income

- you are preparing to sell, incorporate, or bring in a partner

Here is the thing. Cash basis can make a profitable business look poor in one year and strong in the next just because payment dates moved. Traditional accounting smooths that by matching income and costs to the period they belong to.

Worked example 2: stock can change the answer

Assume a small online seller buys £35,000 of goods during 2026/27 and still has £14,000 of stock unsold at 5 April 2027.

Under a simple cash basis view, the business may have paid £35,000 to suppliers. That does not mean all £35,000 has really been used to earn the year’s sales. Some of the goods are still sitting on shelves or in boxes.

Under traditional accounting, the unsold stock is normally held back from the cost of sales calculation. A simplified version looks like this:

| Stock example | Amount |

|---|---|

| Goods bought | £35,000 |

| Closing stock still held | £14,000 |

| Cost matched against current year sales | £21,000 |

That gives a cleaner trading margin. If the seller applies for finance, the lender can see stock, sales, and gross profit more clearly. If the seller only shows bank payments, the numbers may look weaker than the trading position really is.

For a low-stock service business, that difference may not matter. For a shop, food business, or online seller, it can matter a lot.

Making Tax Digital does not remove the choice

Making Tax Digital for Income Tax has made this question more urgent. HMRC says MTD for Income Tax applies from 6 April 2026 to sole traders and landlords with qualifying income from self-employment and property over £50,000. It requires compatible software to create and store digital records, send quarterly updates, submit the tax return, and pay tax due by 31 January after the tax year.

MTD does not mean traditional accounting disappears. It also does not mean cash basis is automatic for every record in every situation. Your software needs to know which method you are using, and your year-end adjustments still need judgement.

For the first MTD year, the practical issue is not only filing. It is whether your records are clean enough by quarter. A sole trader who used to sort receipts once a year now needs a working record process during the year. If the method is wrong, the software can submit tidy-looking numbers that are still poor numbers.

The most common MTD cash basis traps are:

- personal and business spending mixed in one bank account

- sales platforms paying net of fees with no clear fee split

- card processors batching several days of takings into one payout

- supplier bills paid personally and forgotten

- asset purchases posted as ordinary costs without review

- VAT records and income tax records using inconsistent treatment

If you are near the MTD threshold, do not wait until January to decide. The method affects how the whole year is recorded.

Worked example 3: loan application versus tax timing

Assume a self-employed electrician wants a van loan in autumn 2026. The business has:

- invoices raised in the six months to 30 September: £52,000

- cash received by 30 September: £41,000

- unpaid customer invoices: £11,000

- supplier bills unpaid but relating to the same period: £3,500

- tools and equipment bought outright: £6,000

Cash basis may show a lower taxable profit because it ignores the unpaid customer invoices until paid. That can be helpful for tax timing, but the lender may want to know whether the business is actually earning enough to repay the loan.

A traditional accounting pack can show:

| Finance view | Amount |

|---|---|

| Sales earned | £52,000 |

| Debtors outstanding | £11,000 |

| Supplier creditors | £3,500 |

| Equipment spend shown separately | £6,000 |

That does not automatically make traditional accounting better for tax. It does mean the business may need traditional-style management information even if the tax return uses cash basis.

Right, so the answer may be “cash basis for Self Assessment, but fuller reports for decision-making”. That is completely reasonable. Tax reporting and management reporting do not always have to be identical, but you need to know which set of numbers you are looking at.

Switching method: what to check before you change

Switching between cash basis and traditional accounting can create adjustment work. GOV.UK warns that you might have to make adjustments if you switch to traditional accounting. The main risk is counting income or expenses twice, or missing them altogether.

Before changing method, check:

- Which tax year the change starts in.

- What unpaid customer invoices existed at the start and end of the year.

- What unpaid supplier bills existed at the start and end of the year.

- Whether stock, work in progress, deposits, or prepayments need review.

- Whether equipment purchases have been treated correctly.

- Whether your software settings match the tax return basis.

- Whether VAT reporting uses a separate scheme or setting.

Avoid switching because one year happens to produce a nicer tax bill. HMRC expects a method that reflects your business and is applied properly. If the facts change, fine. If the only reason is “I like this year’s answer”, that is a weak position.

What about landlords?

Landlords are pulled into the conversation because MTD for Income Tax covers qualifying property income as well as self-employment income. The accounting basis for property can have its own details, so landlords should be careful about copying sole trader guidance without checking the property pages of the tax return.

The broad point still holds. Rent received, repairs paid, mortgage interest records, agent statements, service charges, deposits, and year-end timing all need clear records. If you own more than one property, your records should also show which income and cost relates to which property.

For landlords close to the MTD threshold, the priority is a digital record process that captures rent and property costs during the year. Waiting until January with twelve months of agent statements is not going to feel clever.

Common mistakes we see with cash basis and traditional accounting

Treating cash basis as “bank statement equals tax return”

A bank statement is a starting point, not the whole tax return. It will not explain private payments, mixed-use costs, capital items, loan transfers, refunds, VAT, or money moved between accounts. You still need bookkeeping judgement.

Forgetting unpaid invoices under traditional accounting

Traditional accounting needs debtors. If you invoice a customer before 5 April and they pay after the year end, the invoice may still belong in the earlier tax year. Missing debtors can understate profit.

Claiming supplier bills in the wrong year

Under cash basis, unpaid bills usually wait until paid. Under traditional accounting, the cost may belong to the year the goods or services were received. Mixing those two treatments creates messy tax returns.

Ignoring stock

Stock is one of the quickest ways for simple cash records to become misleading. If you buy heavily in March but sell the goods in May, the cash movement and the trading performance do not line up.

Assuming MTD software decides for you

Software records what it is told. It will not always know whether a cost is private, whether a customer deposit is income, whether a loan receipt is not sales, or whether a capital item needs separate treatment.

Which method should you choose?

For many small sole traders with simple records, cash basis is a sensible default. It follows real money, reduces the pain of unpaid invoices, and often makes Self Assessment easier.

Traditional accounting deserves a proper look if your business is growing, stock-heavy, finance-dependent, or timing-sensitive. It is also often the better management tool if you want to understand monthly profit rather than just cash movement.

A practical decision process is:

- List your unpaid customer invoices at the year end.

- List supplier bills that relate to the year but were unpaid at 5 April.

- Check stock, work in progress, deposits, and prepayments.

- Ask whether a lender, landlord, buyer, or grant body may need fuller accounts.

- Check whether your software can report clearly on the basis you choose.

- Decide before the year-end tax work starts, not after the draft tax bill appears.

If the difference is small, simplicity may win. If the difference changes lending, tax payments, or business decisions, get the numbers modelled properly. We can review your current records through our bookkeeping support or help prepare the tax return through our Self Assessment service.

FAQ: traditional accounting vs cash basis

Is cash basis now the default for sole traders?

Yes, for most sole traders and partnerships without corporate partners, cash basis is now the standard way to work out taxable profit. You can still choose traditional accounting if it suits the business better.

Can a limited company use cash basis?

No. GOV.UK says limited companies, limited liability partnerships, and partnerships with corporate partners cannot use cash basis. Limited companies normally need traditional company accounts.

Does cash basis reduce my tax bill?

Cash basis can reduce a tax bill in one year if customers have not paid by 5 April, but it is usually a timing difference. The income is normally taxed when the cash is received.

Is cash basis the same as VAT cash accounting?

No. Cash basis for Income Tax and the VAT Cash Accounting Scheme are separate rules. A VAT-registered business needs to check both the Income Tax basis and the VAT scheme used for returns.

Do I need accounting software for cash basis?

Not always for older non-MTD cases, but MTD for Income Tax requires compatible software once you are within the rules. Even outside MTD, software can make bank reconciliation and receipt capture much easier.

Should landlords use cash basis or traditional accounting?

Landlords need to check the property income rules and their own facts. Simple rent and repair records may be easy to track on a cash basis, but finance costs, agent statements, deposits, property improvements, and multiple properties can need closer review.

Pick the method before the records harden for the year. A quick July review is far easier than rebuilding twelve months of bank payments, invoices, stock, and unpaid bills in January.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

Cash Basis Accounting for Sole Traders 2026: Rules, Examples, and When to Use Traditional Accounting

Cash basis accounting for sole traders in 2026, with current HMRC rules, worked examples, MTD points, and when traditional accounting is better.

MTD Penalties 2026: What Happens If You Miss a Quarterly Update?

MTD penalties in 2026 explained, including the first-year soft landing, penalty points, late payment charges, and examples.

MTD Compatible Software for Sole Traders: 2026 Setup Guide

MTD compatible software for sole traders explained: what HMRC expects, how to choose tools, and what to test before quarterly updates.