ERS Return Deadline 6 July 2026: Share Scheme Guide for UK Employers

ERS return deadline 6 July 2026 explained, with EMI notifications, nil returns, penalties, share events, and employer checklist.

ERS Return Deadline 6 July 2026: Share Scheme Guide for UK Employers

The ERS return deadline 6 July 2026 matters if your company has issued shares, granted options, operated an EMI scheme, or registered an employee share arrangement with HMRC. It is easy to miss because it sits beside the better-known P11D deadline on the same date. HMRC will not care that benefits reporting took all the attention.

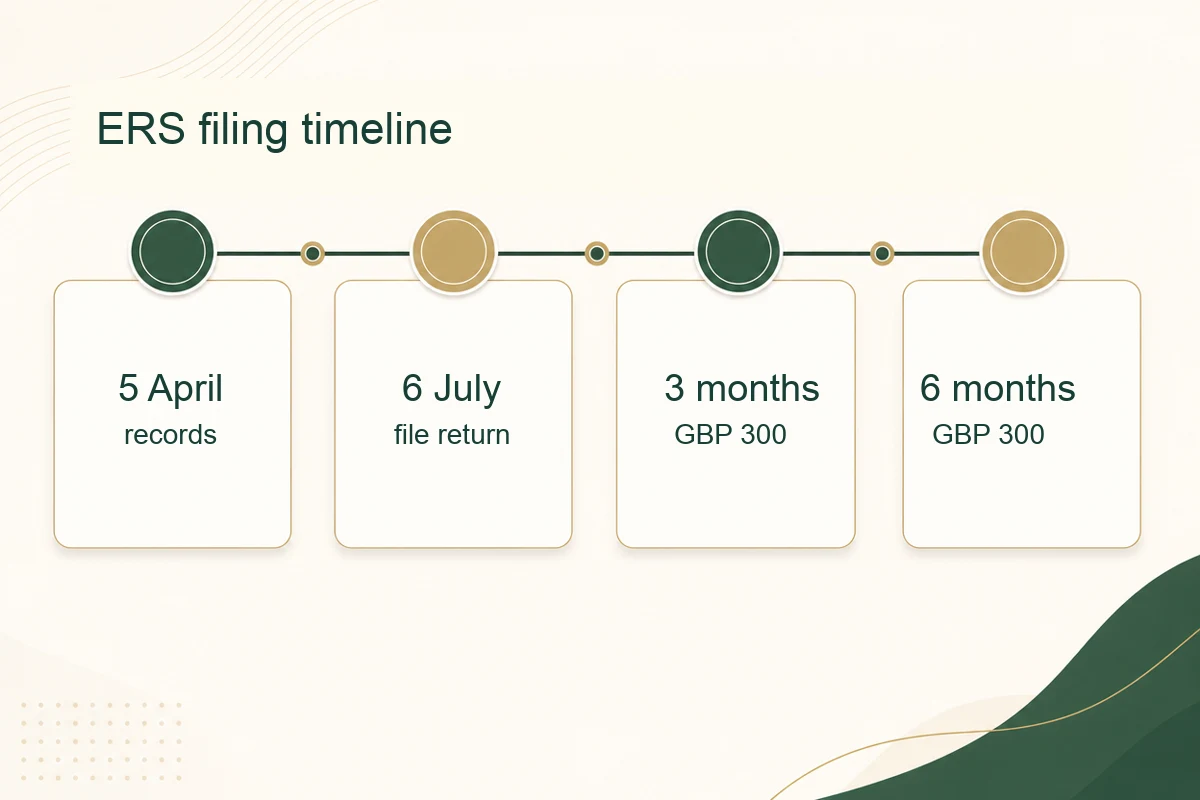

For the 2025/26 tax year, employers must submit an end of year Employment Related Securities, or ERS, return by 6 July 2026 for each registered scheme. If there is nothing to report, a nil return may still be needed. If you granted Enterprise Management Incentives, known as EMI, options during 2025/26, the EMI notification deadline is also 6 July 2026.

Quick summary: check every share issue, option grant, share purchase, director share transfer, EMI grant, and registered share scheme before 6 July 2026. File an ERS return or nil return for every scheme registered with HMRC. Late filing starts with an automatic £100 penalty, and a missed EMI notification can risk the tax advantages of the option.

If you want us to check the accounting records, payroll position, and HMRC filing route before the deadline, we can help through our annual accounts service, payroll services, bookkeeping support, or contact page.

ERS return deadline 6 July 2026: the dates employers need

HMRC’s April 2026 ERS bulletin confirms the main rule. For the 2025 to 2026 tax year, an end of year ERS return is due on or before 6 July 2026. The same bulletin says employers must submit a return or nil return for every scheme registered on the ERS online service.

That last point is where many smaller companies get caught. A scheme can stay live on HMRC’s system even after the exciting part is over. Maybe no options were granted this year. Maybe a founder share issue happened years ago. Maybe somebody registered a scheme and forgot to cease it. If it is still registered, check whether HMRC expects a filing.

| Task | Deadline for 2025/26 |

|---|---|

| Register a tax-advantaged share scheme set up in 2025/26 | 6 July 2026 |

| Register a non tax-advantaged ERS scheme after the first reportable event | 6 July 2026 |

| Submit ERS annual return or nil return | 6 July 2026 |

| Notify HMRC of EMI options granted in 2025/26 | 6 July 2026 |

| File P11D and P11D(b), if relevant | 6 July 2026 |

Official references worth keeping open while you check the position:

- HMRC Employment related securities bulletin 65

- Register your employment related securities scheme

- Submit an EMI notification

- ICAEW reminder on 6 July share scheme returns

The practical advice is boring but useful: do not wait until early July to ask who has the Government Gateway access. ERS filings often need payroll, company secretarial records, option documents, Companies House records, valuation paperwork, and your accountant’s input. Those are rarely all in the same folder.

What Employment Related Securities means in plain English

Employment Related Securities is HMRC’s phrase for shares, options, and other securities connected with employment. That can include arrangements for employees and directors. It does not only mean large quoted company share plans. Owner-managed companies can fall into the rules too.

The connection with employment is the key point. If a director, employee, or office holder gets shares or options because of their role in the company, the arrangement may be reportable. Sometimes there is a formal plan, such as EMI, CSOP, SAYE, or SIP. Sometimes there is no glossy plan document at all, just a small company issuing shares to a director, granting an option to a senior employee, or transferring shares as part of a deal.

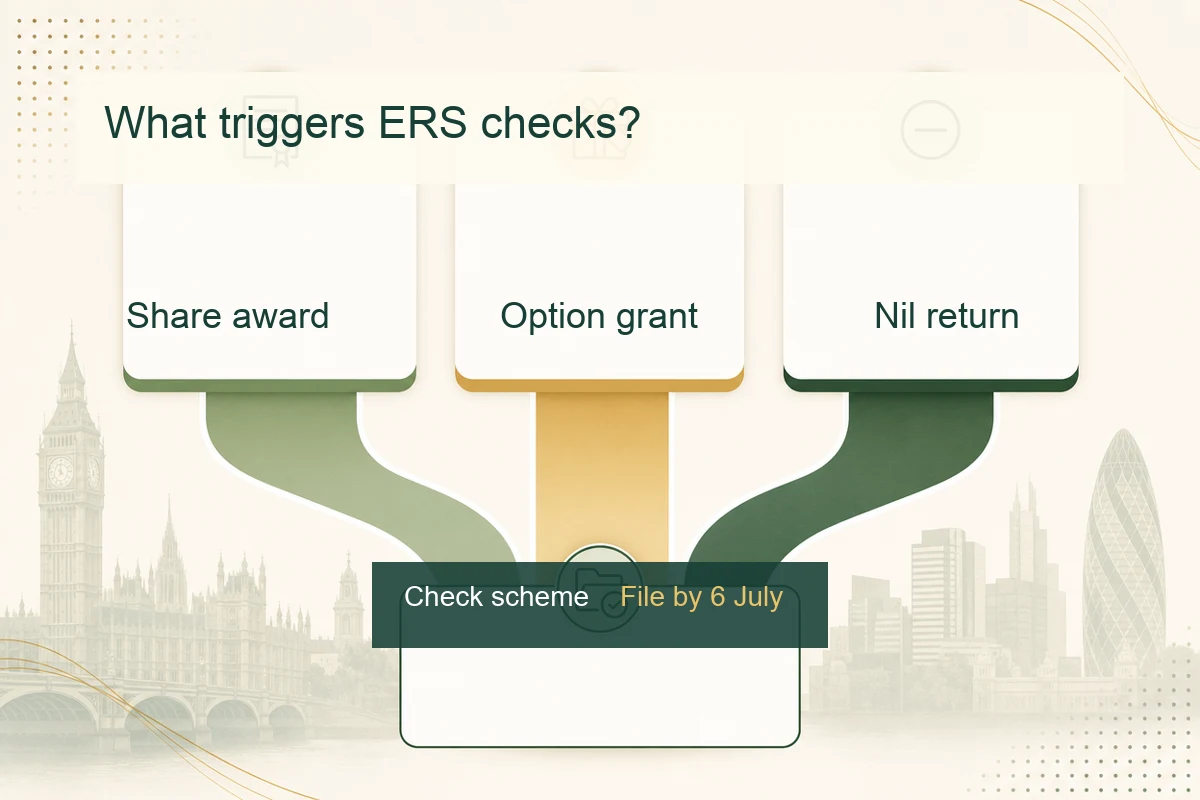

Common events to review include:

- granting share options

- exercising options

- issuing growth shares or ordinary shares to employees or directors

- transferring shares to or from an employee or director

- restricted shares, partly paid shares, and shares acquired below market value

- share awards linked to recruitment, retention, exit planning, or corporate transactions

- registered schemes with no activity, which may still need a nil return

This is one of those areas where a quick “we only issued a few shares” answer can be too casual. A small number of shares can still create a reporting duty. The value, restriction terms, who received the shares, what they paid, and why they received them all matter.

Worked example 1: director shares in a small company

Assume a company issues 100 ordinary shares to a new director on 1 September 2025. The director pays £100 in total, but the company’s adviser later estimates the unrestricted market value at £12,000.

The company now needs to ask several questions:

- were the shares acquired because of the director’s office or employment?

- were any restrictions attached to the shares?

- was the director asked to pay less than market value?

- does PAYE or National Insurance apply, or is the amount dealt with through Self Assessment?

- does the event need to be reported on an ERS return by 6 July 2026?

That does not mean every small share issue creates a payroll charge. It means the company should not treat the Companies House allotment as the end of the matter. Company law records and tax reporting are different jobs.

If the share issue is part of wider owner-manager planning, it may also affect dividend planning, director tax, and eventual disposal relief. Our salary vs dividends guide and Business Asset Disposal Relief guide cover nearby issues, but ERS reporting needs its own deadline check.

Which return template do you need?

HMRC expects the correct end of year return template for the scheme being operated. The main categories include EMI, CSOP, SAYE, SIP, and other non tax-advantaged arrangements. If the wrong template is used, or an old template is uploaded, the ERS online service can reject the submission.

Here is the simple split.

| Arrangement | Typical filing route |

|---|---|

| EMI options | EMI annual return, plus separate EMI notification for grants where needed |

| CSOP, SAYE, or SIP | Specific tax-advantaged scheme return |

| One-off employee or director share issue outside a tax-advantaged plan | Often reported through the “other” ERS return, if reportable |

| Registered scheme with no events in the tax year | Nil return |

| Scheme registered in error or no longer operating | Consider ceasing the scheme, but check whether a final return is still due |

HMRC’s bulletin says you must still submit an annual return for a ceased scheme for the tax year in which the final event date falls. So ceasing a scheme is not a magic delete button for the current year.

The admin sequence can feel back to front. In many cases you need to register the scheme first, wait for the ERS scheme reference, download the correct template, gather the share data, submit the file, and then save evidence because the online service will not keep a copy for you. HMRC says an ERS scheme reference is normally issued online within 7 days of registration, but that still leaves very little room if you begin in the final week.

EMI notifications: the separate 6 July trap

EMI is a tax-advantaged share option scheme for qualifying companies. It is popular with growth companies because it can let employees share in future value without the same tax cost that can arise from a normal share award. The filing side, though, has its own rules.

For EMI options granted before 6 April 2024, HMRC says notification was due within 92 days of the grant. For options granted on or after 6 April 2024, the deadline changed. The notification is due by 6 July following the end of the tax year in which the grant was made. For options granted during 2025/26, that means 6 July 2026.

That EMI notification is separate from the annual ERS return. If the company operates a live EMI scheme, it must also submit the end of year EMI return by 6 July 2026.

Worked example 2: EMI grant made in March 2026

Assume a software company grants EMI options to 8 employees on 20 March 2026. Each employee receives options over shares worth £25,000 at the date of grant, so the total option value is £200,000.

The company should check:

- the EMI scheme was registered

- the options meet the EMI conditions

- the option grant details are complete

- the EMI notification is submitted by 6 July 2026

- the annual EMI return is also filed by 6 July 2026

If the finance team files the annual return but forgets the separate EMI notification, the company may still have a serious problem. HMRC says missing notification deadlines can risk the tax benefits for the employer and employees. That is exactly the sort of mistake people make when they treat 6 July as one filing rather than a bundle of related filings.

There is a fresh 2026 wrinkle too. From 6 April 2026, the EMI limits increased for most eligible companies. HMRC guidance says the gross assets limit rose from £30 million to £120 million, the full-time employee limit rose from 250 to 500, and the company option limit rose from £3 million to £6 million. The maximum exercise period also increased from 10 years to 15 years for companies where the increased limits apply.

Those new limits may make EMI more useful for scale-up companies that previously sat outside the rules. They do not remove the reporting duties for options granted before the later removal of the EMI notification requirement takes effect for grants from 6 April 2027. For 2025/26 grants, file the notification.

Nil returns are not optional admin

Nil returns are the least glamorous part of ERS reporting, which is saying something. They also cause a surprising number of penalties.

If a scheme is registered on HMRC’s ERS online service and there is nothing to report for the year, HMRC can still expect a nil return. The company may feel there was no activity, but HMRC’s system sees a live registered scheme waiting for an annual filing.

Worked example 3: no share activity, still a filing

Assume a company registered an EMI scheme in 2023. It granted options that year, filed the return at the time, and then had no grants, exercises, lapses for consideration, or share events during 2025/26.

The directors might say, “nothing happened this year.” For ERS filing, that is not enough. If the EMI scheme is still live on HMRC’s system, the company should check whether a nil return is due by 6 July 2026.

Now add a second scheme. Suppose the company also registered an “other” ERS arrangement in 2024 for a one-off share award and never ceased it. That could mean two filings to check, not one:

| Registered item | 2025/26 activity | Likely action |

|---|---|---|

| EMI scheme | No events | Submit nil EMI return, if still live |

| Other ERS scheme | No events | Submit nil return or cease correctly, depending on facts |

That is why the first check should be “what schemes are registered?”, not “what do we remember doing?”

Penalties and why access matters

HMRC says an automatic £100 penalty is issued if the end of year ERS return, including a nil return where needed, is not submitted by 6 July 2026. Further automatic £300 penalties can apply if the return is still outstanding 3 months after the original deadline and again if it is still outstanding 6 months after that date.

The money is irritating, but the bigger issue is often the lost time. A late ERS return may need old option documents, valuation notes, board minutes, payroll records, Companies House filings, and employee data. When the person who set up the scheme has left, the job becomes harder than it needed to be.

Worked example 4: the cost of leaving the return outstanding

Assume a company misses the 6 July 2026 ERS deadline for one registered scheme and does not notice until January 2027.

The automatic penalties could look like this:

| Date | Penalty position |

|---|---|

| After 6 July 2026 | £100 automatic late filing penalty |

| 3 months after 6 July | Further £300 if still outstanding |

| 6 months after 6 July | Further £300 if still outstanding |

| Total before considering other consequences | £700 |

That example is for one return. If several registered schemes were missed, the problem can multiply. If an EMI notification was also missed, the question is not just “how much is the fine?” It becomes “have we damaged the tax treatment we promised employees?”

The quickest way to reduce risk is to confirm access now. Check the Government Gateway login, PAYE online access, ERS scheme references, agent authorisation, and who can submit. HMRC says agents can view and file returns for schemes that are already registered, but agents cannot register or end a scheme for you. That part still needs employer-side access.

What records to gather before filing

Start with a list, not the template. The template is only useful once you know what events happened.

For a small company, the records to gather may include:

- cap table at 6 April 2025 and 5 April 2026

- Companies House allotment and transfer filings

- board minutes approving share issues, transfers, or option grants

- option agreements and exercise notices

- EMI valuation agreement or valuation support

- payroll records for directors and employees

- employee start and leaving dates

- market value, unrestricted market value, and price paid

- restrictions attached to shares

- details of any overseas or internationally mobile employees

- confirmation of schemes registered on HMRC’s ERS online service

Some of those records sit with accountants. Some sit with lawyers. Some sit in a founder’s inbox under a subject line that seemed obvious three years ago. That is the real reason to begin before June ends.

There is also a record-keeping trap. HMRC says the online service will not let you access a copy of what you submitted once it has gone in. Save the completed return, any EMI notification attachment, screenshots where relevant, and the confirmation page. Future you will be grateful, which is not something tax admin often gets to hear.

A practical checklist before 6 July

Use this as a working list for the next few weeks.

| Check | Why it matters |

|---|---|

| List every registered ERS scheme | HMRC may expect one return per registered scheme |

| Confirm whether each scheme is still live | Closed or inactive schemes may still need a final or nil return |

| Review share and option events from 6 April 2025 to 5 April 2026 | The filing is based on the tax year, not your company year end |

| Check EMI grants separately | EMI notification and annual return are not the same filing |

| Download the newest template | Old templates can be rejected |

| Confirm Government Gateway access | Access problems are painful in deadline week |

| Save copies before and after submission | HMRC’s online service will not keep the return available for you |

| Link the filing to accounts and payroll review | Share awards can affect tax, NIC, accounts, and disclosures |

If the company has also provided employee benefits, remember that 6 July 2026 is the P11D and P11D(b) deadline as well. Our P11D deadline guide covers that side. Treat ERS and P11D as separate workstreams with the same date, not one combined filing.

When to get advice

You should get advice before filing if any of these apply:

- shares were issued below market value

- directors or employees received growth shares

- restrictions attach to the shares

- options were amended, surrendered, released, exercised, or rolled over

- an EMI valuation was not agreed before the grant

- the company has overseas employees or internationally mobile staff

- the scheme was registered late

- an old registered scheme may need to be ceased

- the company is preparing for sale, investment, or liquidation

None of those points automatically means something has gone wrong. They mean the filing may need more thought than a simple nil return.

This is also a good moment to align the tax filing with your accounts. Share-based payments, payroll reporting, director transactions, and cap table changes can all feed into year-end accounts, Corporation Tax, and investor due diligence. If your records are split between payroll software, Companies House, and old legal documents, the ERS deadline is a useful prompt to tidy the evidence while the year is still fresh.

FAQ

What is the ERS return deadline for 2025/26?

The deadline is 6 July 2026. HMRC says employers must submit an end of year ERS return or nil return for every scheme registered on the ERS online service.

Do I need to file if nothing happened this year?

Possibly, yes. If the scheme is registered with HMRC and there are no reportable events, a nil return may still be needed. Check the ERS online service rather than relying on memory.

Is the EMI notification the same as the EMI annual return?

No. The EMI notification tells HMRC about a grant of EMI options. The EMI annual return reports the year-end position for the scheme. For EMI options granted during 2025/26, the notification deadline is 6 July 2026, and the annual return for a live EMI scheme is also due by that date.

What happens if the ERS return is late?

HMRC applies an automatic £100 penalty for a late ERS return or nil return. Further £300 penalties can apply if the return remains outstanding after 3 months and again after 6 months.

Can my accountant file the ERS return?

An agent can file ERS returns for schemes that are already registered, provided the online authorisation is in place. HMRC says agents cannot register or end a scheme, so the employer still needs to deal with that access and setup.

Does every share issue to a director need an ERS return?

Not always, but do not assume it is outside the rules. Shares or options acquired by reason of employment can fall within ERS. Director share issues, growth shares, nil-paid shares, and discounted shares all deserve a proper check.

Pull the registered scheme list this week, then match it to the cap table and option records for 6 April 2025 to 5 April 2026. If the list does not agree, fix that before touching the template. If you want us to review the records and prepare the filing position, send us the details while there is still time to ask sensible questions.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

P46 Car Form Deadline 2026/27: Company Car Reporting Guide

P46 Car form deadline 2026/27 explained for employers, with quarterly dates, payroll rules, company car tax examples, and checks.

PAYE Settlement Agreement Deadline 5 July 2026: Employer Guide

PAYE Settlement Agreement deadline guide for 2026, with PSA dates, eligible benefits, tax gross-up examples, and employer checklist.

P11D Deadline 6 July 2026: UK Employer Guide to Benefits and Expenses

P11D deadline 6 July 2026 explained for UK employers, with what to report, Class 1A NIC examples, penalties, and a checklist.