How to Run Payroll for One Employee UK: 2026/27 First Employer Guide

How to run payroll for one employee UK in 2026/27, with PAYE registration, FPS deadlines, employer NI, pensions, and costs.

How to Run Payroll for One Employee UK: 2026/27 First Employer Guide

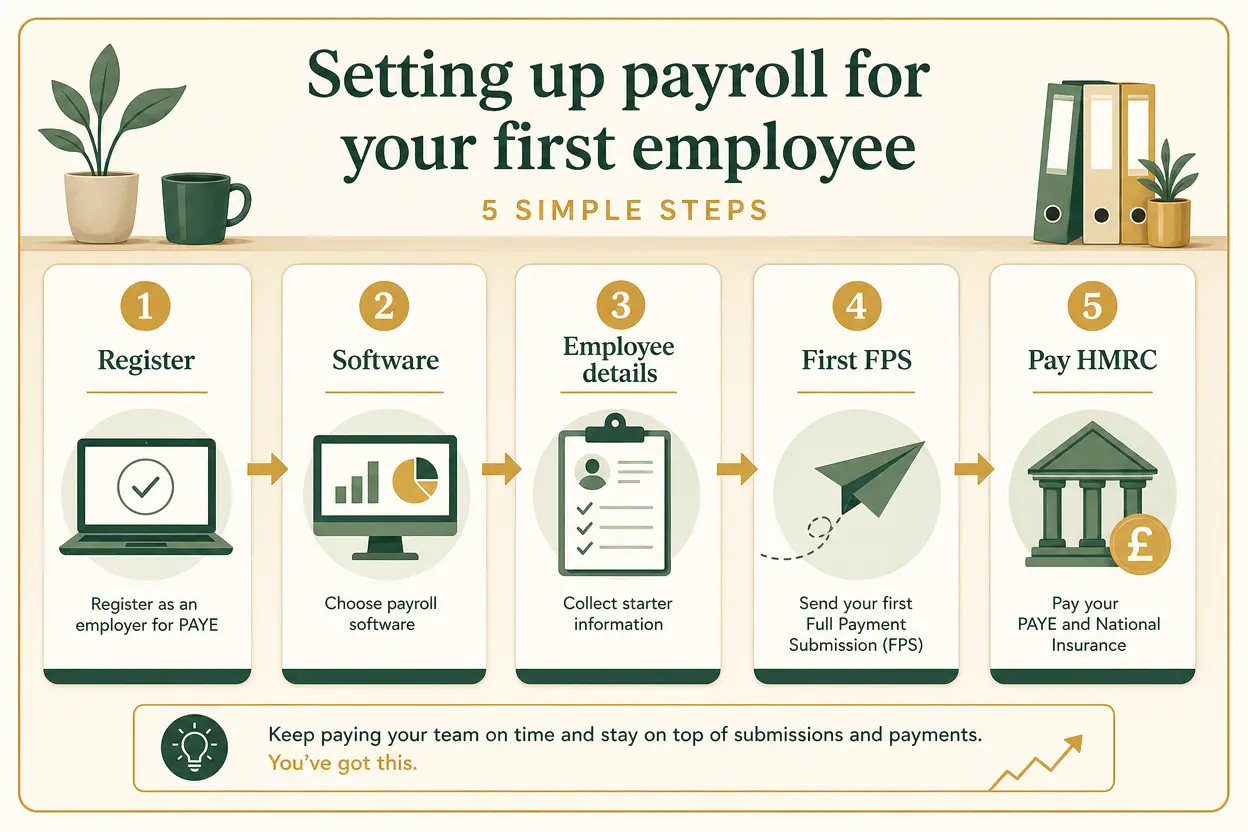

How to run payroll for one employee UK is a more practical question than most first-time employers expect. You are not just paying someone from the business bank account. You may need to register with HMRC, choose payroll software, collect starter details, send a Full Payment Submission, pay PAYE and National Insurance by the right date, and check workplace pension duties.

That sounds like a lot for one member of staff. It is a lot if you leave it until payday morning.

Quick summary: for 2026/27, you normally need to register as an employer before the first payday, send an FPS on or before each payday, pay HMRC by the 22nd of the next tax month if paying electronically, and budget for employer National Insurance at 15% above £417 per month for a standard adult employee. Auto-enrolment pension duties can apply even with one employee.

If you want the payroll set up properly from the first payslip, our payroll services, bookkeeping support, and contact page are the quickest places to start.

How to run payroll for one employee UK in plain English

Payroll is the system that turns gross pay into net pay and reports the position to HMRC. Gross pay is the pay before deductions. Net pay is what the employee receives after deductions such as PAYE Income Tax, employee National Insurance, pension contributions, student loan deductions, and anything else that applies.

For a one-person payroll, the process is usually:

- Check the person is genuinely an employee, not a self-employed contractor.

- Register as an employer with HMRC if you need a PAYE scheme.

- Choose payroll software that can send real time information reports.

- Collect starter information, including the employee’s P45 or starter checklist.

- Run the payslip and send the FPS on or before payday.

- Pay HMRC on time.

- Assess workplace pension duties and keep records.

The official HMRC pages are worth keeping nearby:

- Register as an employer

- Running payroll and reporting to HMRC

- Pay employers’ PAYE

- Rates and thresholds for employers 2026 to 2027

- The Pensions Regulator earnings thresholds

The mistake we see is treating payroll as an afterthought because there is only one employee. HMRC does not run a softer rulebook because your payroll is small. A one-person payroll can still produce late filing penalties, incorrect tax codes, missing pension records, and awkward year-end corrections.

Do you need to register as an employer?

HMRC says you normally need to register as an employer when you start employing staff. You must also register if you are only employing yourself, for example as the only director of a limited company.

You need to register before the first payday so HMRC can send your employer PAYE reference and Accounts Office reference. HMRC also says you cannot register more than 2 months before you start paying people.

The timing matters. If you pay someone before the references arrive, HMRC says you should still run payroll, store the FPS, and then send a late FPS once you can. That is not ideal, but it is better than doing nothing and trying to patch the payroll months later.

Some very small payments may not require a PAYE scheme, depending on the employee’s pay level and whether they have another job, pension, expenses or benefits. Do not guess that point. If the worker earns enough to trigger PAYE reporting, or if their circumstances require reporting, you need a proper scheme.

What information do you need before the first payslip?

Before you run the first payroll, collect the details your software will need. At minimum, that usually means:

- full name

- address

- date of birth

- National Insurance number, if available

- start date

- gross pay and pay frequency

- tax code source, usually a P45 or starter checklist

- student loan or postgraduate loan position

- pension assessment details

- bank details for payment

If the employee gives you a P45, use it. If they do not, ask them to complete HMRC’s starter checklist. The starter declaration helps decide which tax code basis to use. A wrong starter declaration can mean too much or too little PAYE in the first few months, which is not the warm welcome anyone wants from a new job.

Right to work checks, contracts, Employers’ Liability insurance, holiday entitlement, statutory sick pay duties, and HR records sit around payroll rather than inside it. They still matter. Payroll is not the whole employment process, but it is where many of the numbers become visible.

The 2026/27 payroll rates and thresholds to know

For most small employers, the current year figures are the anchor points. GOV.UK says the following rates and thresholds apply from 6 April 2026 to 5 April 2027, unless stated otherwise.

| Item | 2026/27 figure | Why it matters |

|---|---|---|

| Standard personal allowance | £12,570 a year | Main PAYE tax-free allowance for many employees |

| Monthly PAYE threshold | £1,048 | Standard monthly equivalent of the personal allowance |

| Employee National Insurance primary threshold | £1,048 per month | Employee NI usually starts above this level |

| Employer National Insurance secondary threshold | £417 per month | Employer NI usually starts above this level |

| Standard employer NI rate, category A | 15% | The employer cost above the secondary threshold |

| National Living Wage, age 21 and over | £12.71 per hour from 1 April 2026 | Minimum hourly pay for most workers aged 21+ |

| Employment Allowance | £10,500 | Can reduce eligible employers’ annual employer NI bill |

Scotland has different income tax bands for Scottish taxpayers. Payroll software should handle that through the tax code, but the employer still needs accurate starter information and correct payroll setup.

The Employment Allowance is useful, but do not assume it always applies. There are eligibility rules, and some companies with only one paid director and no other employees cannot claim. We covered the wider 2026/27 changes in our employer National Insurance and payroll changes guide.

Worked example 1: what one employee really costs each month

Assume you employ one adult employee in England on £2,000 gross pay per month in 2026/27. For simplicity, assume tax code 1257L, National Insurance category A, no student loan, no salary sacrifice, and minimum employer pension contributions on qualifying earnings.

Employer National Insurance is calculated above the monthly secondary threshold:

- monthly gross pay: £2,000

- employer NI threshold: £417

- pay above the threshold: £2,000 - £417 = £1,583

- employer NI at 15%: £1,583 x 15% = £237.45

For a basic workplace pension example, qualifying earnings are broadly the slice between £520 and £4,189 per month. At £2,000 gross pay:

- qualifying earnings: £2,000 - £520 = £1,480

- employer pension at 3%: £1,480 x 3% = £44.40

So the employer’s approximate monthly cost is:

| Cost | Amount |

|---|---|

| Gross salary | £2,000.00 |

| Employer NI | £237.45 |

| Employer pension contribution | £44.40 |

| Approximate total employer cost | £2,281.85 |

That figure does not include payroll software, accountancy fees, holiday cover, sick pay risk, training, equipment, insurance, or any other staff cost. It is just the monthly payroll cost. The specific result may differ if the worker is under 21, an apprentice, on a different NI category, or in a salary sacrifice arrangement.

Sending the FPS on or before payday

The FPS, or Full Payment Submission, tells HMRC what you have paid the employee and what deductions you have made. HMRC says you should send it on or before payday, even if you pay HMRC quarterly instead of monthly.

That one sentence is the heart of real time information payroll. The report is tied to the employee payment, not to the later date when you settle the PAYE bill.

Your software will normally ask for:

- the employee’s gross pay

- PAYE tax deducted

- employee National Insurance

- employer National Insurance

- pension details

- student loan or postgraduate loan deductions, if relevant

- the payment date

- starter or leaver information where needed

Use the normal payday as the payment date even if you pay early because of a bank holiday. HMRC’s guidance says not to report too early, because later changes can mean sending corrections.

If you make a mistake in an FPS, fix it promptly. A small payroll is often easier to correct than a large one, but the correction route still depends on timing and the type of error.

Paying HMRC after the payroll run

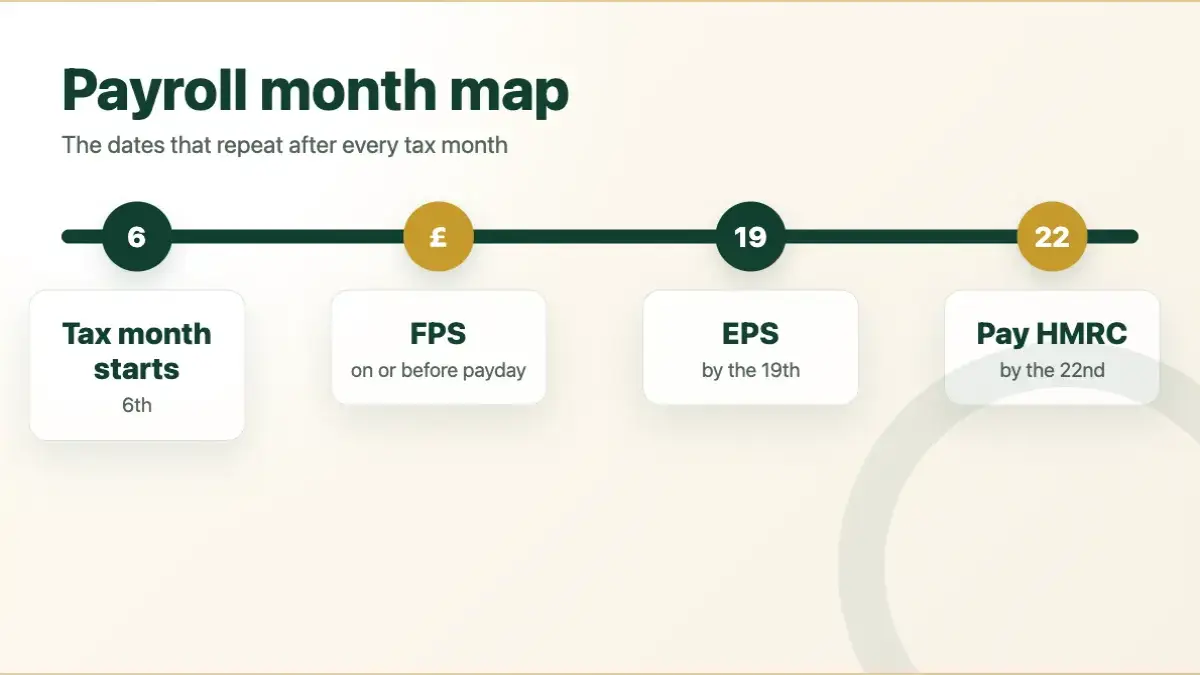

After you send the FPS, HMRC’s online account should show the amount due. HMRC says you can view the PAYE and NI owed from the 10th of the next tax month, claim reductions such as statutory pay by sending an EPS by the 19th, and pay the balance by the 22nd if paying electronically. If paying by post, the cheque must reach HMRC by the 19th.

The UK tax month runs from the 6th of one month to the 5th of the next. That is why a payday on 31 May 2026 falls in the tax month ending 5 June 2026, with electronic payment due by 22 June 2026.

Worked example 2: May payroll and the June PAYE payment date

Assume your first employee is paid on 31 May 2026.

You should:

- run payroll before the employee is paid

- send the FPS on or before 31 May 2026

- check the PAYE account from 10 June 2026

- send any EPS claim by 19 June 2026, if needed

- pay HMRC electronically by 22 June 2026

If you pay by direct debit, bank transfer, or another electronic route, allow time for the payment to reach HMRC. A payment made at 11pm on the due date can be a surprisingly expensive way to learn about bank processing times.

Workplace pension duties for one employee

Auto-enrolment can apply even if you only employ one person. The Pensions Regulator says the annual earnings trigger for automatic enrolment in 2026/27 is £10,000, with a monthly equivalent of £833. The lower level of qualifying earnings is £6,240 a year, or £520 per month, and the upper level is £50,270 a year, or £4,189 per month.

In plain English, if your employee is aged between 22 and State Pension age and earns above the trigger, you will usually need to put them into a workplace pension and contribute. If they earn less, they may still have rights to join or opt in, depending on their age and earnings.

This is one of those areas where “they said they don’t want a pension” does not remove the employer duties. You still need to assess them, issue the right communications, process any opt-out properly, and keep records.

Worked example 3: pension contribution on £2,000 per month

Using the same £2,000 monthly gross pay:

- lower qualifying earnings level: £520 per month

- qualifying earnings: £2,000 - £520 = £1,480

- employer minimum at 3%: £44.40

- employee minimum at 5%: £74.00, before any tax relief method differences

That is why the payslip is not just “salary minus tax”. Pension setup affects both the employee’s take-home pay and the employer’s cost.

What happens if you file payroll late?

HMRC can charge penalties if your FPS is late, if you do not send the expected number of FPS reports, or if you fail to send an EPS when you did not pay anyone in a tax month.

For a small employer with 1 to 9 employees, the monthly late filing penalty is £100. HMRC’s guidance also says there are cases where a penalty is not charged, such as a first failure in a tax year or a new employer sending their first FPS within 30 days of paying an employee. Do not rely on that as a process. Treat it as a backstop if something genuinely goes wrong.

Late payment is separate. GOV.UK says you may have to pay interest and penalties if your PAYE payment is late. That means two different problems can happen in the same month:

- the FPS was late

- the PAYE and National Insurance payment was late

Neither is helped by hoping HMRC will not notice. Payroll is reported in real time. It is rather good at making late admin visible.

Common first employee payroll mistakes

The first mistake is paying a neat round amount and planning to “sort the tax later”. PAYE does not work like that. If you pay an employee, run the payroll first.

The second mistake is registering too late. You cannot register more than 2 months before you start paying staff, but you also should not wait until payday. HMRC letters and online access can take time.

The third mistake is using the wrong tax code because nobody asked for a P45 or starter checklist. The employee may blame HMRC, the software, or the accountant. The actual problem is often missing starter information.

The fourth mistake is ignoring pension duties because the team is tiny. One employee is still an employee.

The fifth mistake is forgetting year-end tasks. Payroll does not end when the monthly payslip is issued. You may need P60s by 31 May, P11Ds by 6 July if benefits are reported that way, and clean records for accounts and tax returns. Keep our P60 deadline guide and PAYE year-end checklist nearby once the payroll is live.

A practical first payroll checklist

Use this before the first payday, not after it:

| Task | Done? |

|---|---|

| Confirm the worker’s employment status | |

| Agree gross pay, hours, pay frequency, and payday | |

| Check National Minimum Wage compliance | |

| Register as an employer with HMRC, where needed | |

| Choose payroll software or appoint payroll support | |

| Collect P45 or starter checklist information | |

| Assess workplace pension duties | |

| Run the first payslip before paying the employee | |

| Send the FPS on or before payday | |

| Save payroll reports and payslips | |

| Pay HMRC by the 22nd electronically, or 19th by post |

For many small businesses, the best point to ask for help is before the first payday. Once the employee has been paid incorrectly, the work shifts from setup to correction. Our payroll services can handle the registration, software workflow, monthly payroll, payslips, RTI submissions, pension processing, and employer reminders.

FAQ: how to run payroll for one employee UK

Do I need payroll if I only have one employee?

Yes, if the employee’s pay or circumstances mean you need to operate PAYE. One employee can still require an employer PAYE scheme, FPS reports, payroll records, payslips, and pension assessment.

When do I need to register as an employer?

HMRC says you must register before the first payday, and you cannot register more than 2 months before you start paying people.

When is the FPS due?

The FPS is due on or before the employee’s payday. That is separate from the later deadline for paying PAYE and National Insurance to HMRC.

When do I pay PAYE and National Insurance to HMRC?

If you pay monthly and electronically, HMRC says the deadline is the 22nd of the next tax month. If paying by cheque through the post, it must reach HMRC by the 19th.

Does auto-enrolment apply to one employee?

It can. For 2026/27, the annual automatic enrolment earnings trigger is £10,000, with a monthly equivalent of £833. Age and earnings both matter, and workers who are not automatically enrolled may still have pension rights.

How much does a £2,000 monthly employee cost in 2026/27?

Using a standard adult employee example, employer NI is about £237.45 and a 3% qualifying earnings pension contribution is about £44.40, making the approximate monthly payroll cost £2,281.85 before other employment costs.

Can I do payroll myself?

Yes, if you use suitable payroll software and understand the filing dates, pension duties, and record keeping. Many owners start themselves and then outsource once the monthly cycle becomes a distraction from paid work.

The best next step

Before you agree the start date, write down the first payday, the gross pay, the HMRC registration date, the FPS date, the pension assessment date, and the HMRC payment date. That single payroll calendar prevents most first-month mistakes. If any of those dates are already close, get the setup reviewed before money leaves the bank.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

How to Run Payroll for the First Time in the UK: New Employer Checklist for 2026

Learn how to run payroll for the first time in the UK, from HMRC registration and pensions to PAYE deadlines, costs, and first payday checks.

1257L M1 Tax Code Explained: Emergency Tax Guide for 2026/27

1257L M1 tax code explained for 2026/27, with emergency tax calculations, refund examples, and practical steps to correct your code.

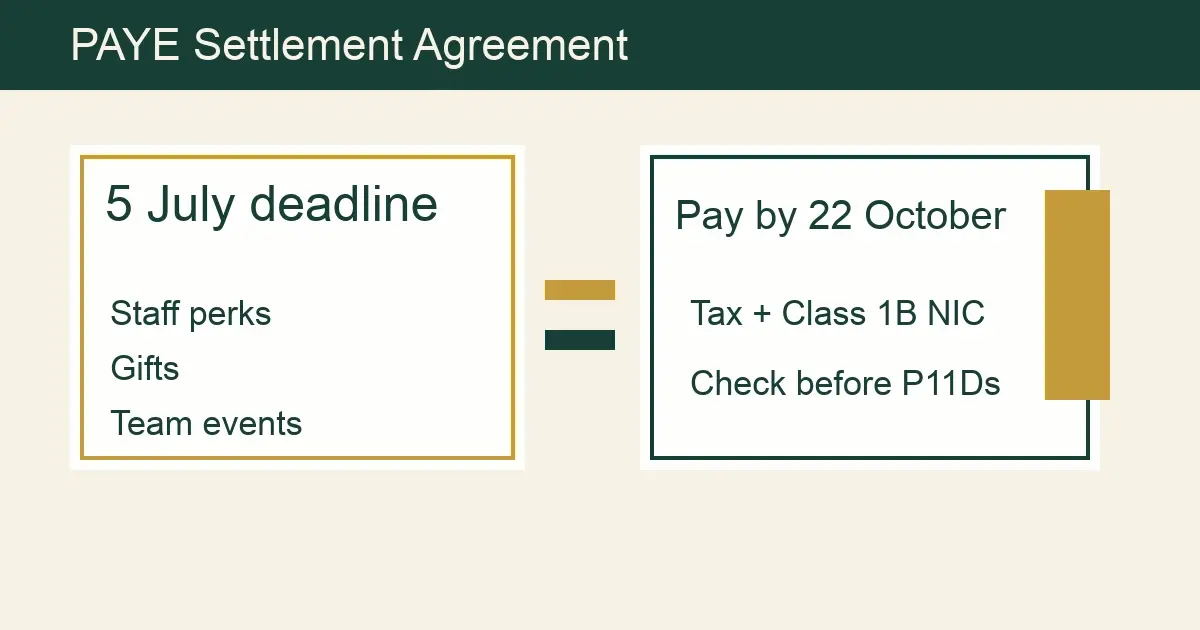

PAYE Settlement Agreement Deadline 5 July 2026: Employer Guide

PAYE Settlement Agreement deadline guide for 2026, with PSA dates, eligible benefits, tax gross-up examples, and employer checklist.