VAT Cash Accounting Scheme UK: 2026 Guide for Small Businesses

VAT Cash Accounting Scheme UK rules for 2026, with thresholds, cash-flow examples, eligibility checks, and record-keeping tips.

VAT Cash Accounting Scheme UK: 2026 Guide for Small Businesses

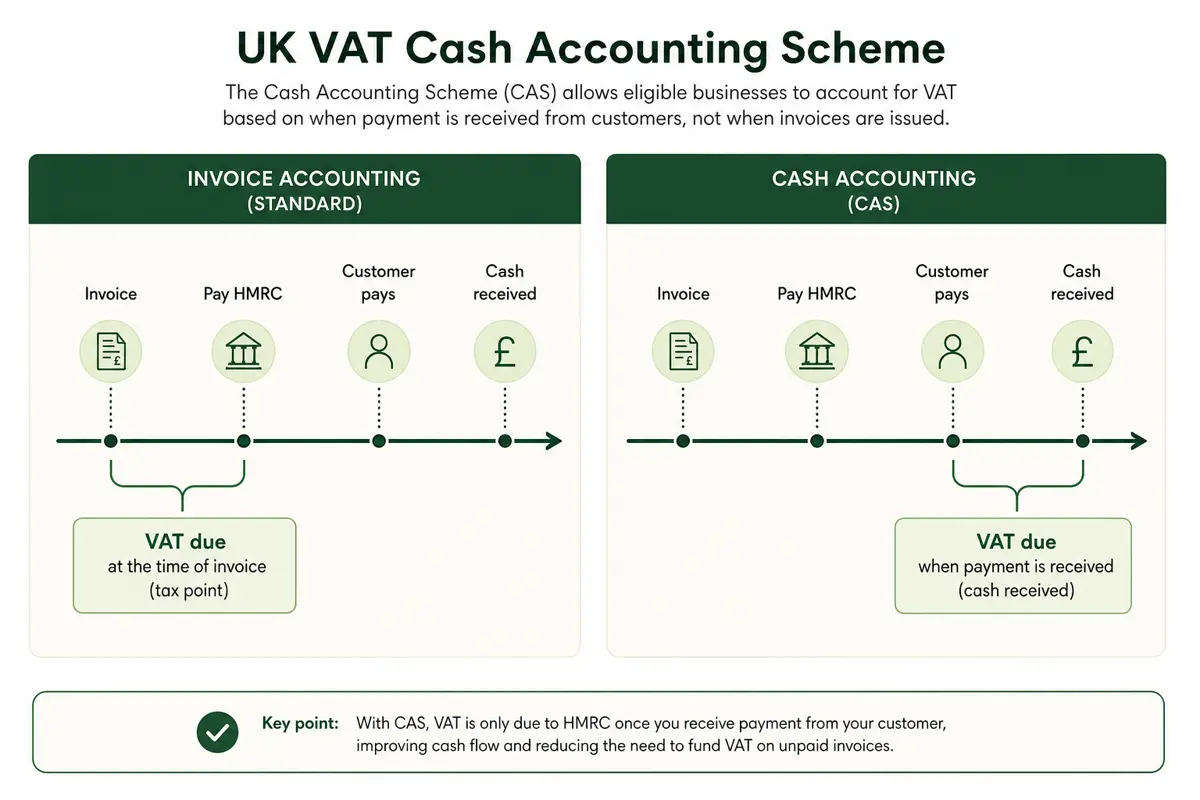

The VAT Cash Accounting Scheme UK businesses can use in 2026 is a simple idea with a big cash-flow effect. Instead of paying VAT to HMRC because you raised an invoice, you usually pay the VAT when your customer pays you. For a small business with slow-paying customers, that timing difference can stop a VAT bill landing before the money has arrived.

There is a trade-off. You normally reclaim VAT on purchases when you pay your supplier, not when the supplier invoices you. So cash accounting can help when customers pay late, but it may be less attractive if you buy stock or equipment on credit and want to reclaim input VAT quickly.

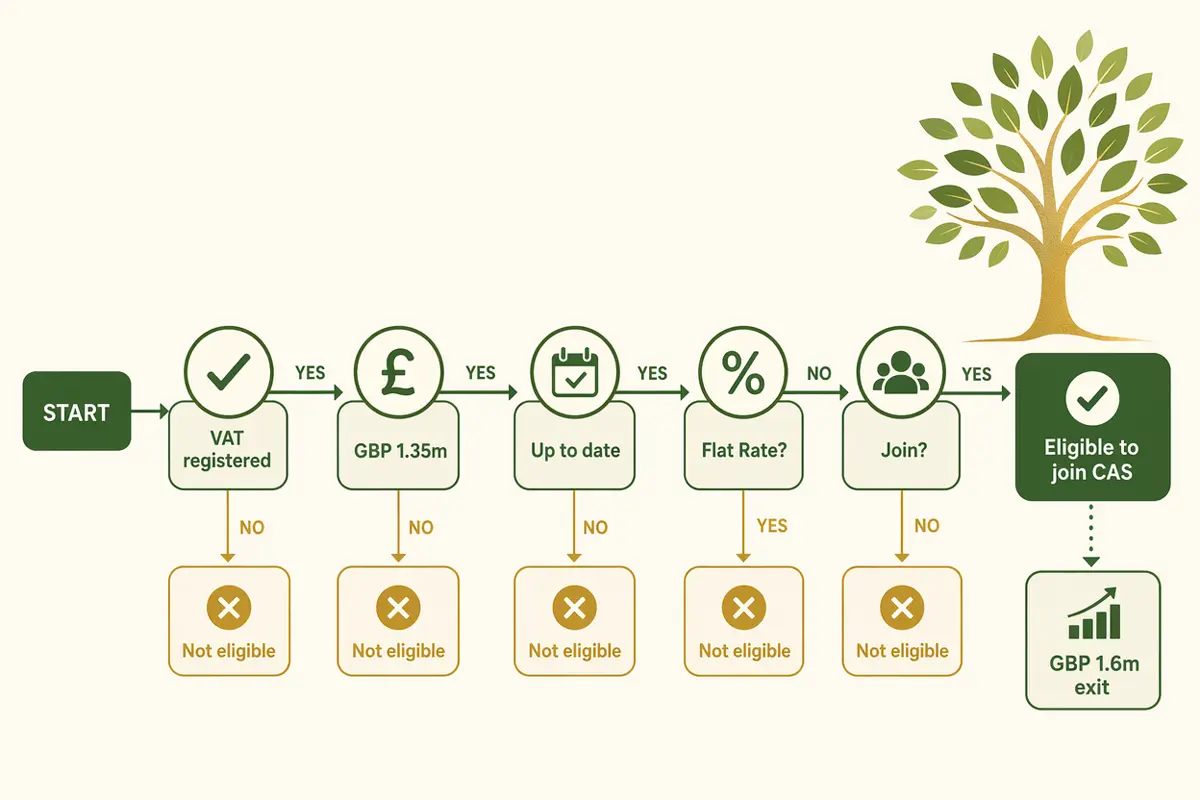

Quick summary: you can usually join the VAT Cash Accounting Scheme if your business is VAT registered and your estimated VAT taxable turnover is £1.35 million or less in the next 12 months. You must normally leave if VAT taxable turnover goes over £1.6 million. You do not need to tell HMRC when you join, but you must start from the beginning of a VAT accounting period and keep clear payment records.

If VAT returns are already taking too long, we can help you tighten the process through our VAT returns service, bookkeeping support, and VAT registration advice.

VAT Cash Accounting Scheme UK rules in plain English

Under normal VAT accounting, your VAT return follows invoices. If you invoice a customer in June and the invoice falls into the June quarter, the output VAT usually goes on that VAT return, even if the customer pays in August.

Under cash accounting VAT, the timing follows payment. You account for output VAT when customers pay you. You reclaim input VAT when you pay suppliers. GOV.UK describes the scheme in exactly those practical terms: VAT on sales is paid when customers pay you, and VAT on purchases is reclaimed when you have paid your supplier.

That makes the scheme especially relevant for:

- consultants, agencies, trades, and subcontractors with 30-day or 60-day payment terms

- businesses selling mainly to other VAT-registered businesses

- service businesses with low stock levels

- firms where customer payment dates are more unpredictable than supplier payment dates

- seasonal businesses that want VAT returns to follow actual cash received

It is less useful where customers pay immediately, where you regularly buy stock on credit, or where you already use a scheme that does not fit alongside cash accounting.

Official references worth keeping open are GOV.UK’s VAT Cash Accounting Scheme guide, the eligibility page, and GOV.UK’s VAT thresholds page.

The 2026 thresholds and eligibility checks

The current VAT cash accounting threshold is £1.35 million of estimated VAT taxable turnover for the next 12 months. VAT taxable turnover means sales that are not VAT exempt. It is not profit, and it is not your bank balance.

GOV.UK also lists a leaving threshold of more than £1.6 million. If your VAT taxable turnover goes above that level, you normally have to leave the scheme.

| Rule | Current figure | Practical meaning |

|---|---|---|

| VAT registration threshold | More than £90,000 | You must register for VAT if taxable turnover crosses the normal registration test |

| Cash Accounting Scheme join threshold | £1.35 million or less | You can usually join if estimated VAT taxable turnover for the next 12 months is within this level |

| Cash Accounting Scheme leave threshold | More than £1.6 million | You must normally leave once VAT taxable turnover exceeds this level |

| Annual Accounting Scheme join threshold | £1.35 million or less | Often considered alongside cash accounting for smaller VAT businesses |

| Flat Rate Scheme join threshold | £150,000 or less | Cannot be used with the normal Cash Accounting Scheme, because the Flat Rate Scheme has its own cash-based method |

You can usually use cash accounting if:

- your business is VAT registered

- your estimated VAT taxable turnover is £1.35 million or less in the next 12 months

- your VAT returns and VAT payments are up to date

- you have not committed a VAT offence in the last 12 months

- HMRC has not withdrawn or refused your use of the scheme

You cannot use the normal scheme if you use the VAT Flat Rate Scheme. You also cannot use cash accounting for certain transactions, including invoices with payment terms of six months or more, VAT invoices raised in advance, hire purchase or lease purchase transactions, and some Northern Ireland or customs warehouse movements.

This is one of those areas where a quick eligibility check is worth doing before changing your software settings. If your sales mix includes imports, finance agreements, deposits, or long payment terms, the answer can be less tidy than the headline rule suggests.

Invoice accounting versus cash accounting: why the timing matters

The best way to understand the scheme is to follow one invoice through a VAT quarter.

Assume a marketing agency raises an invoice for £12,000 plus VAT on 20 June 2026. The VAT is £2,400, so the total invoice is £14,400. The customer has 60-day payment terms and pays on 19 August 2026.

Under normal invoice accounting, the output VAT belongs to the VAT period that includes the June invoice. The agency may need to include £2,400 of output VAT on the return before the customer pays.

Under cash accounting, the VAT usually follows the August customer payment. The £2,400 is accounted for in the VAT period when the payment is received.

Worked example 1: the cash-flow difference on slow payment

Take a VAT quarter ending 30 June 2026.

| Detail | Normal VAT accounting | Cash accounting VAT |

|---|---|---|

| Sales invoice raised in June | £12,000 plus £2,400 VAT | £12,000 plus £2,400 VAT |

| Customer pays | 19 August 2026 | 19 August 2026 |

| VAT return includes output VAT in June quarter? | Yes | No, because cash has not arrived |

| VAT due before customer pays? | £2,400 may be due | Usually £0 for that invoice until payment |

That does not reduce the VAT. It changes the timing. HMRC still gets the VAT when the customer pays, but the business is not funding VAT from its own cash while waiting for the debtor.

For a business with one slow invoice, the effect may be modest. For a firm with £60,000 of unpaid VATable sales sitting in trade debtors at quarter end, the cash-flow swing can be much larger. At 20% VAT, the VAT inside £72,000 of gross unpaid invoices is £12,000. Paying that before the cash arrives can hurt.

The purchase side: input VAT waits too

Cash accounting is not only about sales. It also changes when you reclaim VAT on purchases.

Under normal VAT accounting, you may be able to reclaim input VAT based on the supplier invoice, subject to the usual rules and evidence. Under cash accounting, you normally reclaim the VAT when you pay the supplier.

That matters if you buy stock, tools, equipment, or software on supplier credit.

Worked example 2: delayed input VAT reclaim

Assume a VAT-registered retailer receives a stock invoice on 25 June 2026:

- stock cost: £9,000

- VAT at 20%: £1,800

- total supplier invoice: £10,800

- supplier payment date: 10 August 2026

Under normal accounting, the £1,800 input VAT may fall into the June quarter if the invoice and records are valid.

Under cash accounting, the retailer normally waits until the August payment before reclaiming that input VAT.

That is why cash accounting often suits service firms better than stock-heavy businesses. A consultant with few supplier invoices may benefit from waiting to pay output VAT. A retailer with regular stock purchases may dislike waiting to reclaim input VAT.

The right answer depends on the pattern of both sides of the ledger. If customers pay late and suppliers are paid quickly, the scheme can be helpful. If customers pay immediately and suppliers give generous credit, it may make cash flow worse.

How to join the VAT Cash Accounting Scheme

You do not need to apply to HMRC or send a separate notification to join the scheme. If you are eligible, you start using it at the beginning of a VAT accounting period.

That sounds refreshingly simple by HMRC standards. Still, the bookkeeping setup needs care.

Before switching, check:

- the business is eligible on turnover and VAT compliance

- the change starts from the first day of a VAT quarter, not halfway through

- your bookkeeping software is set to cash accounting for VAT from the correct date

- unpaid old invoices are kept separate so they are not missed or counted twice

- purchase invoices and sales invoices can be matched to payment dates

- bank feeds, payment processors, and card receipts are posting cleanly

- your accountant or bookkeeper knows the change has happened

HMRC’s tertiary legislation says you cannot apply the Cash Accounting Scheme retrospectively. It also says your records must clearly cross-refer payments received to sales invoices, payments made to purchase invoices, and payments to evidence such as bank statements, cheque stubs, or paying-in slips.

That record link is the whole system. A VAT return under cash accounting is only as reliable as the payment matching underneath it.

What to watch in your bookkeeping software

Most cloud bookkeeping systems can run VAT returns on cash accounting, but the setting is not the same as a magic clean-up button.

Check these points before relying on the first return:

| Software area | What to check | Why it matters |

|---|---|---|

| VAT scheme setting | Cash accounting selected from the right VAT period | A mid-period change can create messy reports |

| Payment matching | Customer receipts matched to the correct sales invoices | Unmatched cash can leave VAT in the wrong period |

| Supplier payments | Payments matched to purchase invoices | Input VAT should not be reclaimed before payment |

| Part payments | System accounts for only the paid proportion | A 50% payment should not trigger 100% of the VAT |

| Deposits and advance invoices | Treated under the correct tax point rules | Cash accounting does not fix every timing rule |

| Payment processors | Gross receipts, fees, and VAT are split correctly | Card and platform payouts can hide the true payment date |

Part payments deserve special attention. If a customer pays half an invoice, the VAT usually follows the paid part. For example, if a customer pays £6,000 against a £12,000 plus VAT invoice, you do not simply ignore the payment until the whole invoice is settled. Your system needs to account for the VAT on the part paid.

Mixed-rate invoices are another area to treat carefully. If one invoice includes standard-rated and zero-rated items, a payment may need to be split across the different VAT rates. Software can help, but only if the invoice was coded properly in the first place.

Cash accounting, MTD for VAT, and digital records

The VAT Cash Accounting Scheme does not remove Making Tax Digital for VAT requirements. If your business is within MTD for VAT, you still need digital VAT records and compatible software to submit VAT returns.

The difference is the basis of the VAT return calculation. Instead of the VAT report pulling mainly from invoice dates, it relies on payment dates and matched transactions. That makes bank reconciliation more important, not less.

GOV.UK’s VAT record guidance says VAT records must usually be kept for at least six years. It also says a business using cash accounting has a payment-received tax point. In practice, that means you need to preserve:

- sales invoices

- purchase invoices

- bank records

- card processor records

- payment matching evidence

- VAT return workings

- notes explaining adjustments, bad debts, and unusual transactions

If your records are behind, switching scheme may hide the problem for a quarter, then create a bigger one. We would usually tidy the bank feed, debtor list, creditor list, and VAT codes before relying on cash accounting.

Bad debts: do you still need bad debt relief?

Bad debt relief is less central when you use cash accounting because you normally have not paid output VAT on a customer invoice until the customer pays. That is one of the scheme’s main attractions.

Under normal VAT accounting, a customer can fail to pay after you have already accounted for the VAT. GOV.UK says bad debt relief may be available when a debt is older than six months, and claims must usually be made within four years and six months of the payment due date or date of supply, whichever is later.

Cash accounting can reduce that bad debt pain, but it does not remove all messy cases. Watch for:

- invoices that were already accounted for before you joined the scheme

- deposits or advance invoices outside the normal cash accounting treatment

- part payments followed by a write-off

- factoring or debt sale arrangements

- customers paying through agents or platforms

If a debtor position is already messy, sort that before changing scheme. Otherwise you may not know which invoices have already had VAT paid and which are waiting for cash.

When the scheme is a good fit

The VAT Cash Accounting Scheme often works well where the business has a simple sales cycle and a clear payment trail.

Good-fit signs include:

- customers regularly pay 30 to 90 days after invoice

- most customers are businesses, not consumers

- sales invoices are larger and less frequent

- supplier bills are paid promptly

- the business has low stock and low finance agreement activity

- bookkeeping software is already reconciled monthly

- the owner wants VAT returns to reflect real cash received

Worked example 3: agency with late-paying customers

Assume a design agency has these figures at quarter end:

| Item at quarter end | Amount excluding VAT | VAT at 20% |

|---|---|---|

| Paid customer invoices | £45,000 | £9,000 |

| Unpaid customer invoices | £35,000 | £7,000 |

| Paid supplier invoices | £12,000 | £2,400 |

| Unpaid supplier invoices | £4,000 | £800 |

Under normal invoice accounting, the sales VAT could be £16,000 and the purchase VAT could be £3,200, giving a net VAT bill of £12,800.

Under cash accounting, the sales VAT on paid invoices is £9,000 and the purchase VAT on paid supplier invoices is £2,400, giving a net VAT bill of £6,600 for that period.

The unpaid invoices are not ignored forever. Their VAT moves into later periods when money changes hands. Still, the immediate cash-flow difference is £6,200. For a small agency, that can cover payroll, rent, or supplier payments in a tight month.

Your specific numbers may differ, especially if you have mixed VAT rates, exempt income, imports, or large supplier bills. Treat examples as a planning guide, not personal tax advice.

When cash accounting can cause problems

The scheme is not automatically better because it sounds more cash-friendly.

It can be awkward where:

- you receive payment before raising invoices

- customers pay immediately by card or direct debit

- you buy stock on credit and want to reclaim VAT before paying suppliers

- you use finance agreements, hire purchase, lease purchase, or conditional sale arrangements

- you have invoice payment terms of six months or more

- you use the Flat Rate Scheme

- you have poor payment matching in the bookkeeping system

- turnover is close to the £1.6 million leaving threshold

Retailers are a good example. A shop may receive customer payment immediately, so cash accounting does not delay much sales VAT. If suppliers give 60-day credit, input VAT may be delayed instead. That can make the return worse, not better.

Businesses with many card, marketplace, and platform payments also need care. A payout from a platform may combine several customer receipts, fees, refunds, and adjustments. The VAT calculation should follow the underlying transactions properly, not just the net amount landing in the bank.

Leaving the scheme

You can leave the scheme voluntarily, but GOV.UK says you should leave at the end of a VAT accounting period. You must leave if you are no longer eligible.

When you stop using cash accounting, you do not simply forget unpaid old invoices. GOV.UK says you must report and pay any outstanding VAT, whether your customers have paid you or not. It also says you can usually report and pay that outstanding VAT over six months, unless your VAT taxable turnover exceeded £1.35 million in the last three months, in which case you must report and pay straight away.

That exit calculation is often where businesses need help. You need a list of:

- unpaid sales invoices where output VAT has not yet been accounted for

- unpaid purchase invoices where input VAT has not yet been reclaimed

- part-paid invoices

- old disputed balances

- deposits and advance invoices

- debtors already written off

Do this before the final return on the scheme. Trying to reconstruct it later from old bank data is possible, but nobody enjoys that particular afternoon.

A practical checklist before switching

Before you move to cash accounting VAT, run this short review.

| Question | Why it matters |

|---|---|

| Are you VAT registered and within the £1.35 million join threshold? | Eligibility comes first |

| Are VAT returns and payments up to date? | HMRC excludes businesses that are not up to date |

| Do customers pay later than supplier bills? | This is where the cash-flow benefit usually appears |

| Do you use the Flat Rate Scheme? | The normal scheme cannot be used with it |

| Do invoices have payment terms under six months? | Long payment terms may be excluded |

| Can software match payments to invoices reliably? | Payment matching drives the VAT return |

| Have unpaid old invoices been listed before the switch? | This helps prevent double counting or missed VAT |

| Does your accountant agree with the date and settings? | A second check is cheaper than fixing a bad VAT return |

If the answer is unclear, do not change the setting five minutes before filing. Take one VAT quarter, compare invoice accounting with cash accounting, and look at the actual cash-flow effect.

For businesses with slow-paying customers, the scheme can be genuinely useful. For businesses with weak bookkeeping, it can just move the confusion from invoices to bank payments.

If you want us to check whether cash accounting fits your VAT position, send us a note with your last VAT return, current debtor list, current creditor list, and bookkeeping software name. We can usually tell quite quickly whether the scheme is worth testing or whether another VAT process would be cleaner.

FAQ: VAT Cash Accounting Scheme UK

What is the VAT Cash Accounting Scheme?

The VAT Cash Accounting Scheme lets eligible VAT-registered businesses account for VAT based on payments rather than invoice dates. You usually pay output VAT when customers pay you and reclaim input VAT when you pay suppliers.

What is the VAT cash accounting threshold in 2026?

The current join threshold is estimated VAT taxable turnover of £1.35 million or less in the next 12 months. You must normally leave if VAT taxable turnover goes over £1.6 million.

Do I need to tell HMRC before using cash accounting VAT?

No, GOV.UK says you do not have to tell HMRC when you join. You must be eligible and start from the beginning of a VAT accounting period.

Can I use cash accounting with the Flat Rate Scheme?

No. GOV.UK says you cannot use the normal Cash Accounting Scheme if you use the VAT Flat Rate Scheme. The Flat Rate Scheme has its own cash-based turnover method.

Does cash accounting mean I pay less VAT?

No. It changes timing, not the VAT rate or the final amount due. It may improve cash flow because you are not usually paying VAT on customer invoices before the customer has paid you.

Is cash accounting good for every small business?

No. It often suits service businesses with late-paying customers. It can be worse for businesses that receive customer payment quickly but pay suppliers later, because input VAT recovery may be delayed.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

VAT Return Dates 2026: UK Deadline Guide for Small Businesses

VAT return dates 2026 explained for UK small businesses, with quarterly deadlines, payment dates, penalties, and examples.

VAT Registration Threshold UK 2026: When Small Businesses Need to Register

VAT registration threshold UK rules for 2026, with turnover tests, dates, penalties, voluntary registration, and worked examples.

VAT Registration Threshold UK: When to Register, Deadlines, and Worked Examples for 2026

VAT registration threshold UK rules for 2026 explained with deadlines, worked examples, voluntary registration pros and cons, and common mistakes to avoid.