VAT Return Dates 2026: UK Deadline Guide for Small Businesses

VAT return dates 2026 explained for UK small businesses, with quarterly deadlines, payment dates, penalties, and examples.

VAT Return Dates 2026: UK Deadline Guide for Small Businesses

The VAT return dates 2026 problem is simple until the quarter closes, the bank feed is behind, one supplier bill has been coded twice, and the payment date is suddenly next Friday. For most UK small businesses filing quarterly VAT returns, the deadline is one month and seven days after the VAT period ends. That means the quarter ending 30 June 2026 is normally due by 7 August 2026.

That date covers the return and, in most standard quarterly cases, the VAT payment too. Filing the return without paying the VAT is only half the job. Paying the VAT without fixing the return is not much better. HMRC’s systems can charge late submission penalties, late payment penalties, and interest, and those are three different problems.

Quick summary: if your VAT quarter ends on 30 June 2026, plan for a 7 August 2026 filing and payment deadline. A 30 September 2026 quarter is usually due by 7 November 2026, and a 31 December 2026 quarter by 7 February 2027. Check your VAT online account because stagger periods, annual accounting, payments on account, and unusual periods can change the answer.

If you want the deadline handled without a last-week scramble, we can help through our VAT returns service, bookkeeping support, and contact page.

VAT return dates 2026: the standard quarterly deadlines

Most VAT-registered businesses file quarterly. GOV.UK’s VAT return guidance says returns are usually submitted every three months, and the deadline is normally one month and seven days after the end of the VAT period. GOV.UK’s payment guidance gives the same practical rule for paying the VAT bill.

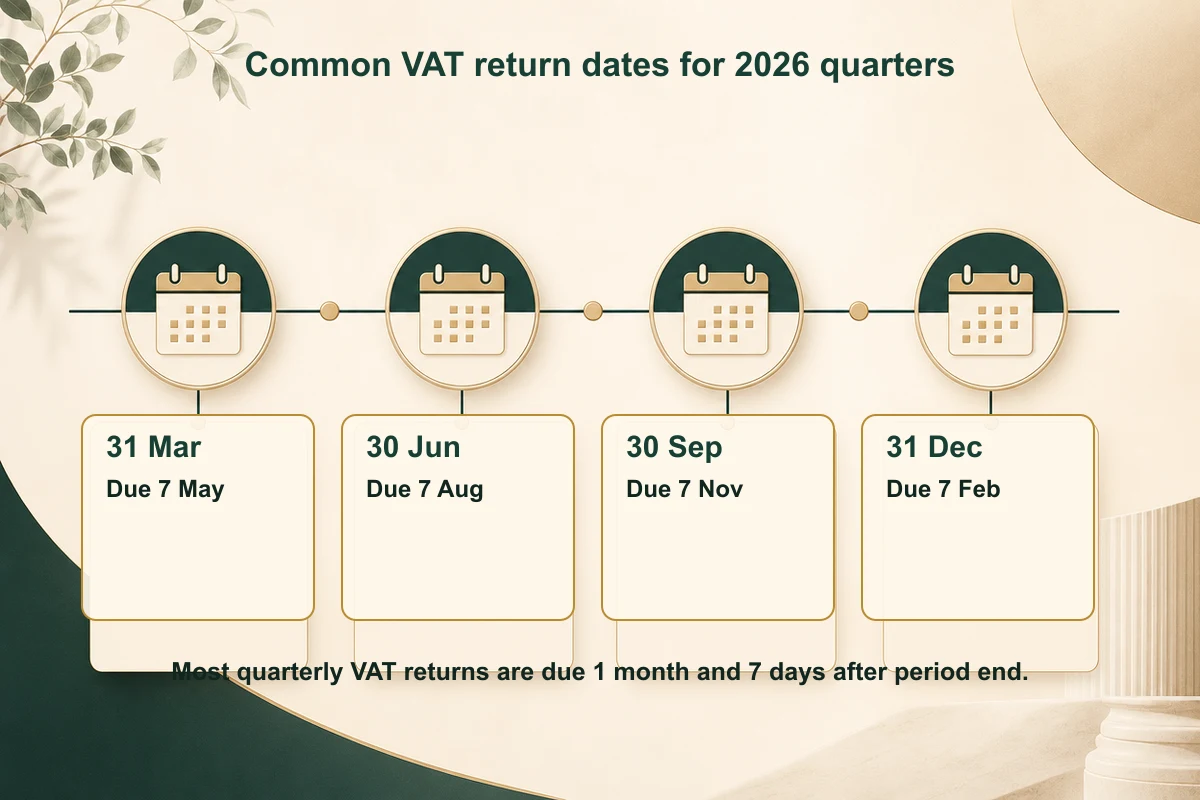

Here are the common calendar-quarter VAT return dates for 2026:

| VAT period ends | Usual return deadline | Usual payment deadline | Practical planning date |

|---|---|---|---|

| 31 March 2026 | 7 May 2026 | 7 May 2026 | Reconcile by late April |

| 30 June 2026 | 7 August 2026 | 7 August 2026 | Reconcile by late July |

| 30 September 2026 | 7 November 2026 | 7 November 2026 | Reconcile by late October |

| 31 December 2026 | 7 February 2027 | 7 February 2027 | Reconcile by late January |

That table is useful if your VAT quarters follow calendar quarters. Many businesses do, but not all. HMRC can put a business on different stagger periods, such as quarters ending in January, April, July, and October, or February, May, August, and November. Your VAT online account is the final source for your own dates.

Worth mentioning though: the deadline is not moved just because the seventh day lands near a weekend or holiday in the way many people expect. Payment method matters too. If you pay by Direct Debit, HMRC usually takes payment automatically after the return is received. If you pay by bank transfer, card, or another route, you need to allow enough time for HMRC to receive cleared funds.

Official references worth keeping open are GOV.UK’s VAT online account page, GOV.UK’s VAT payment page, and GOV.UK’s VAT penalties and interest collection.

Worked example 1: quarter ending 30 June 2026

Assume a VAT-registered design agency has a quarterly VAT period ending 30 June 2026. Its deadline is normally 7 August 2026.

By the time the return is filed, the agency needs to check:

- sales invoices dated in the VAT period

- customer credits and refunds

- purchase invoices and receipts

- bank transactions and card processor payouts

- reverse charge entries, if any

- imports, postponed VAT accounting, or overseas services

- VAT adjustments, bad debt relief, and previous corrections

Here is a simple set of figures:

| Item for the June 2026 quarter | Net amount | VAT |

|---|---|---|

| Standard-rated sales | £52,000 | £10,400 |

| Standard-rated purchases | £18,500 | £3,700 |

| VAT due before adjustments | £6,700 | |

| Previous small correction | £120 added | |

| VAT to pay | £6,820 |

The return and payment would normally be due by 7 August 2026. If the business waits until 6 August to reconcile the bank, there is almost no time left to investigate missing purchase invoices or coding errors. A better rhythm is to close the quarter by mid-July, review the return before the end of July, then file before the final week.

That is not just tidiness. It protects cash flow. A £6,820 payment that arrives as a surprise on 5 August is harder to absorb than the same payment forecast three weeks earlier.

What changes your VAT return date?

The one month and seven days rule is the normal pattern, not a promise that every VAT business has the same date.

Your deadline may differ if you use:

| Situation | What can change |

|---|---|

| Monthly VAT returns | Deadlines follow monthly periods, often used where the business regularly reclaims VAT |

| Annual Accounting Scheme | You usually make payments during the year and file one annual return |

| Payments on account | Larger VAT businesses may make interim payments with a balancing payment |

| Non-standard VAT periods | HMRC may set a shorter or longer first period, or a changed stagger |

| VAT group registration | The group representative member manages the group return date |

| Deregistration or final return | HMRC may issue a specific final period and deadline |

Annual accounting deserves special care. It can reduce the number of VAT returns, but it does not mean VAT is ignored all year. Businesses usually make advance payments and then file one annual return. The timing can be useful, but the cash-flow effect needs checking before you choose it.

Monthly VAT returns can be useful where a business often receives repayments, for example because it exports, makes zero-rated supplies, or has heavy input VAT. The trade-off is more frequent admin. If records are messy quarterly, monthly filing will not magically make them cleaner. It just gives you twelve chances a year to discover the mess.

If you’re unsure which cycle you are on, do not guess from last year’s diary. Log in to the VAT online account or ask your accountant to check the current obligation. We see deadline errors when a business changes period, changes agent, joins a scheme, or assumes every quarter works like the last one.

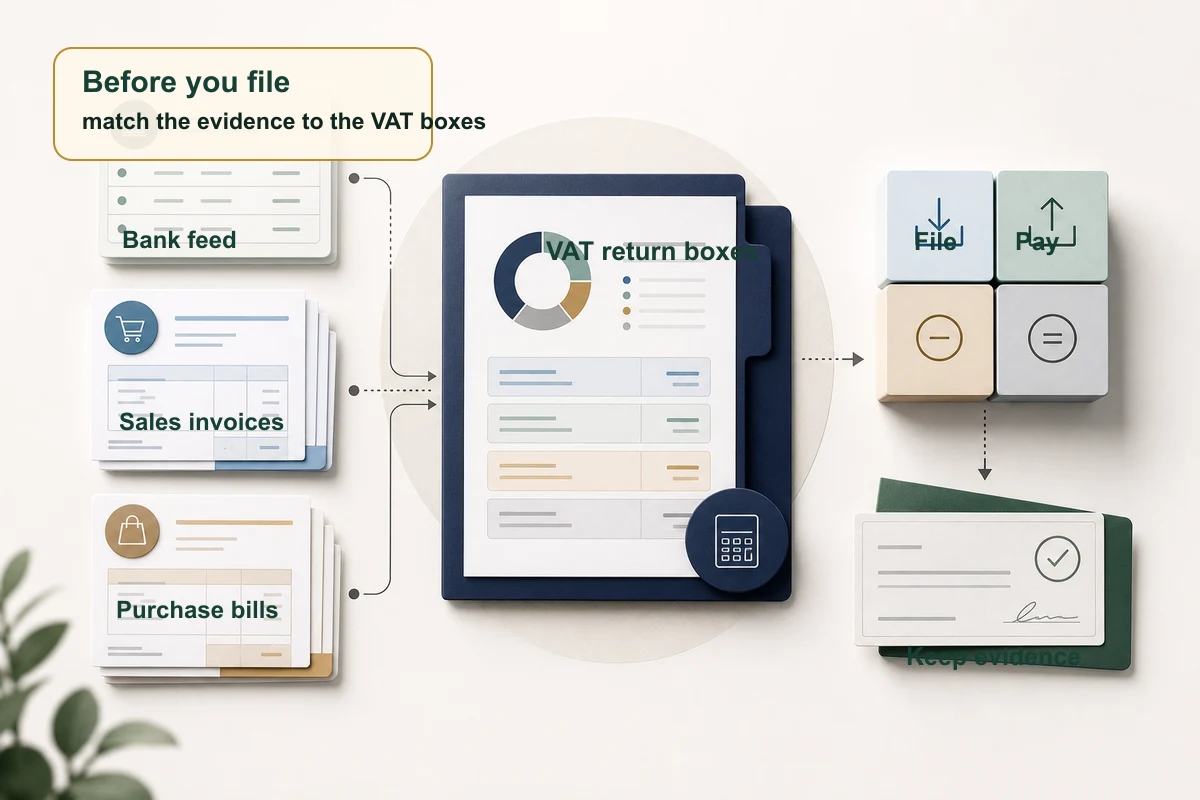

The records to get ready before filing

A VAT return is a summary, not a pile of invoices. The return is only as reliable as the records behind it.

For a standard small business VAT return, we would expect to review:

- sales invoices, till reports, platform statements, or payment processor reports

- credit notes and refunds

- purchase invoices and receipts with valid VAT evidence

- bank feed transactions and reconciliations

- import VAT statements, postponed VAT accounting statements, and customs records where relevant

- reverse charge entries for construction, overseas services, or other affected transactions

- VAT codes in the bookkeeping software

- previous VAT return balances and any outstanding corrections

Right, so what actually goes wrong? Usually it is not one dramatic error. It is five small ones. A card processor payout is posted as sales even though the invoices are already in the system. A supplier invoice is claimed without a VAT invoice. A mixed-rate receipt is put wholly to 20%. A credit note is missed. A director pays a business cost personally and forgets to send the receipt.

The VAT return deadline is the moment those small errors become urgent. Monthly bookkeeping makes the return easier because the evidence is already in place. Our bookkeeping service is designed around that: keep the records current, then the VAT return becomes a review exercise rather than a rescue job.

Worked example 2: one coding error can change the VAT bill

Assume a cafe has these draft VAT figures for the quarter ending 30 September 2026:

- output VAT on sales: £8,200

- input VAT on purchases: £3,100

- draft VAT payable: £5,100

During review, the owner spots that a new coffee machine was posted as a general expense without VAT. The invoice shows:

- net cost: £2,400

- VAT at 20%: £480

- gross cost: £2,880

If the cafe has a valid VAT invoice and the purchase is for taxable business use, that missing £480 input VAT can reduce the VAT payable:

| Draft position | Amount |

|---|---|

| Draft VAT payable | £5,100 |

| Missing input VAT claim | £480 |

| Corrected VAT payable | £4,620 |

That is why review matters. The goal is not to push the VAT bill down at any cost. The goal is to file the right return with the right evidence. Sometimes the review increases the bill because output VAT was missed. Sometimes it reduces the bill because input VAT was missed. Either way, the return is better.

Your specific situation may differ, especially if you use a VAT scheme such as the Flat Rate Scheme or Cash Accounting Scheme. We recently covered the VAT Cash Accounting Scheme because timing can change where payments, invoices, and claims sit on the return.

What happens if you submit a VAT return late?

HMRC’s late submission system uses penalty points. For a quarterly VAT business, the penalty threshold is usually four points. Once you reach that threshold, HMRC charges a £200 penalty. Later missed returns can create further £200 penalties while you remain at the threshold.

The threshold depends on how often you submit:

| Filing frequency | Penalty point threshold |

|---|---|

| Annual | 2 points |

| Quarterly | 4 points |

| Monthly | 5 points |

There are rules for removing points, but they are not instant. You usually need a period of compliance and all outstanding returns filed. In plain English: do not treat the first late point as harmless just because it is not yet a fine. It can sit there waiting for the next missed return.

Late submission penalties can apply even if the VAT return is nil or repayment. That catches people out. If your return says HMRC owes you money, it still needs filing on time.

What happens if you pay VAT late?

Late payment is a separate system. GOV.UK’s VAT late payment guidance says late payment interest is charged from the first day payment is overdue until it is paid in full. Late payment penalties can then apply if the VAT remains unpaid for long enough.

For VAT payments under the current rules:

| Payment position | Penalty effect |

|---|---|

| Up to 15 days overdue | No first or second late payment penalty, but interest can still apply |

| 16 to 30 days overdue | First late payment penalty at 3% of VAT outstanding at day 15 |

| 31 or more days overdue | First penalty includes 3% at day 15 plus 3% at day 30, then a second daily penalty at a 10% annual rate from day 31 |

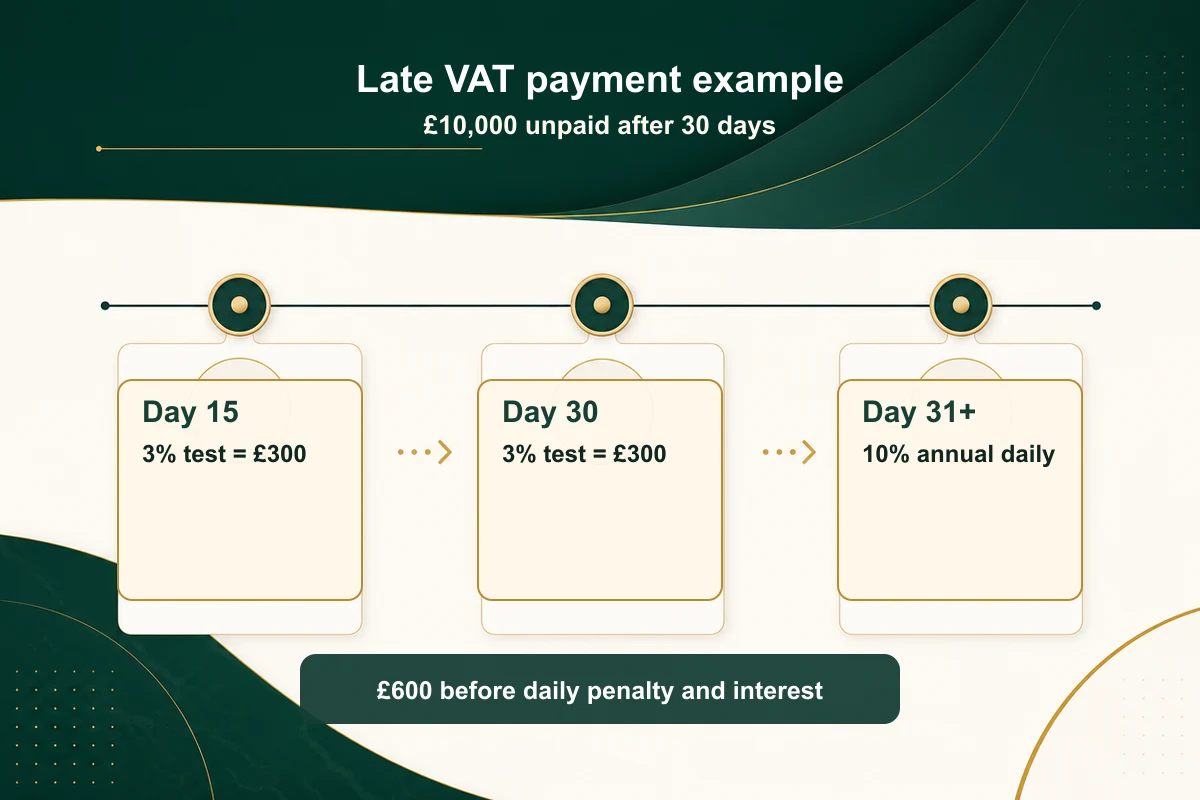

Worked example 3: £10,000 VAT paid after 30 days

Assume a business files its VAT return on time, but £10,000 of VAT is still unpaid after 30 days.

The first late payment penalty would be:

| Penalty stage | Calculation | Amount |

|---|---|---|

| Day 15 test | £10,000 × 3% | £300 |

| Day 30 test | £10,000 × 3% | £300 |

| First late payment penalty before daily penalty | £600 |

If the debt continues into day 31 and beyond, a second late payment penalty starts to build daily at a 10% annual rate on the outstanding balance. Late payment interest is separate.

This is where a Time to Pay arrangement can matter. HMRC says agreeing a payment plan may mean lower or no late payment penalties, depending on timing and whether you keep to the arrangement. If you know you cannot pay, speak to HMRC early rather than waiting for penalty letters.

How to avoid the 7 August rush

The best VAT return process starts before the quarter ends.

For a quarter ending 30 June 2026, a sensible timetable looks like this:

| Date | Job |

|---|---|

| 30 June | VAT quarter ends |

| 1 to 10 July | Import bank transactions, card payouts, sales invoices, and purchase bills |

| 11 to 20 July | Reconcile bank, check VAT codes, chase missing invoices |

| 21 to 31 July | Review return, check payment forecast, agree adjustments |

| 1 to 5 August | Submit return and schedule payment |

| 7 August | HMRC deadline |

That leaves room for real life. The supplier who sends invoices late. The director who paid for software on a personal card. The Stripe payout that combines sales, fees, and refunds. The customer credit note that sits in emails rather than the accounts system. VAT has a talent for finding the one missing document at the worst time.

If you use Xero, QuickBooks, FreeAgent, Sage, or another cloud system, the software should help, but do not skip review. Bank rules can post transactions quickly and still post them wrongly. Receipt capture can read a gross amount but miss the VAT treatment. A neat dashboard is not evidence by itself.

When to ask for help

You should get help before the deadline if any of these apply:

- your VAT quarters are not clear in the VAT online account

- bank reconciliations are more than a month behind

- you have imported goods, overseas services, or postponed VAT accounting

- you use the domestic reverse charge for construction

- sales include a mix of standard-rated, zero-rated, exempt, and outside-scope income

- you have received a VAT assessment, penalty, or interest notice

- you cannot pay the VAT by the deadline

- you are not sure whether old errors need adjusting on the next return or reporting separately

The last point matters. Small VAT errors can often be corrected on a later return if they meet HMRC’s conditions, but larger or more serious errors may need separate disclosure. Do not simply hide an old error inside the next box 1 or box 4 figure and hope for the best.

If you’d like us to review your VAT position before the next deadline, start with our VAT returns service or send the details through the contact page. We can check the VAT period, records, coding, payment forecast, and any scheme issues before the deadline becomes expensive.

VAT return dates 2026 FAQ

What is the next VAT return deadline after 30 June 2026?

For a standard quarterly VAT period ending 30 June 2026, the next VAT return deadline is usually 7 August 2026. The VAT payment is normally due by the same date. Check your VAT online account because your business may have a different stagger or scheme.

Are VAT returns due every three months?

Most VAT-registered small businesses submit VAT returns quarterly, but some submit monthly or annually. Monthly returns are common for repayment traders. Annual accounting reduces the number of returns but usually involves payments during the year.

Can I file a VAT return before the deadline?

Yes. You can file before the deadline once the VAT period has ended and the records are ready. Filing early can help cash-flow planning because you know the payment figure sooner. Do not file before checking bank reconciliations, VAT codes, and missing purchase invoices.

Does a nil VAT return still need filing?

Yes. If HMRC expects a VAT return, you need to submit it even if there is no VAT to pay or the return is nil. Late submission points can still apply to nil and repayment returns.

What if I cannot pay my VAT bill?

File the return on time if you can, then contact HMRC as early as possible about payment. A Time to Pay arrangement may reduce or prevent some late payment penalties, but interest can still apply. The worst option is silence: HMRC does not treat a missed payment better because the return was ignored too.

Can Golden Tree Consulting file my VAT return?

Yes, if we have the right authorisation, software access, and records. We can also clean up the bookkeeping before filing so the return is based on evidence rather than guesswork. For a tight deadline, send sales, purchase, bank, and VAT account records as early as possible.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

VAT Cash Accounting Scheme UK: 2026 Guide for Small Businesses

VAT Cash Accounting Scheme UK rules for 2026, with thresholds, cash-flow examples, eligibility checks, and record-keeping tips.

VAT Registration Threshold UK 2026: When Small Businesses Need to Register

VAT registration threshold UK rules for 2026, with turnover tests, dates, penalties, voluntary registration, and worked examples.

VAT Return Deadline 7 May 2026: UK Checklist for Quarter Ending 31 March

VAT return deadline 7 May 2026 explained for UK businesses, with a filing checklist, common mistakes, error rules, and payment timing tips.