VAT Registration Threshold UK 2026: When Small Businesses Need to Register

VAT registration threshold UK rules for 2026, with turnover tests, dates, penalties, voluntary registration, and worked examples.

VAT Registration Threshold UK 2026: When Small Businesses Need to Register

The VAT registration threshold UK businesses need to watch in 2026 is GBP 90,000 of VAT-taxable turnover. That figure sounds simple until you try to apply it in a growing business with deposits, one-off contracts, exempt sales, overseas customers, and monthly bookkeeping that is not quite up to date. The real risk is not usually ignorance of VAT. It is missing the exact month when your rolling 12-month turnover tips over the line.

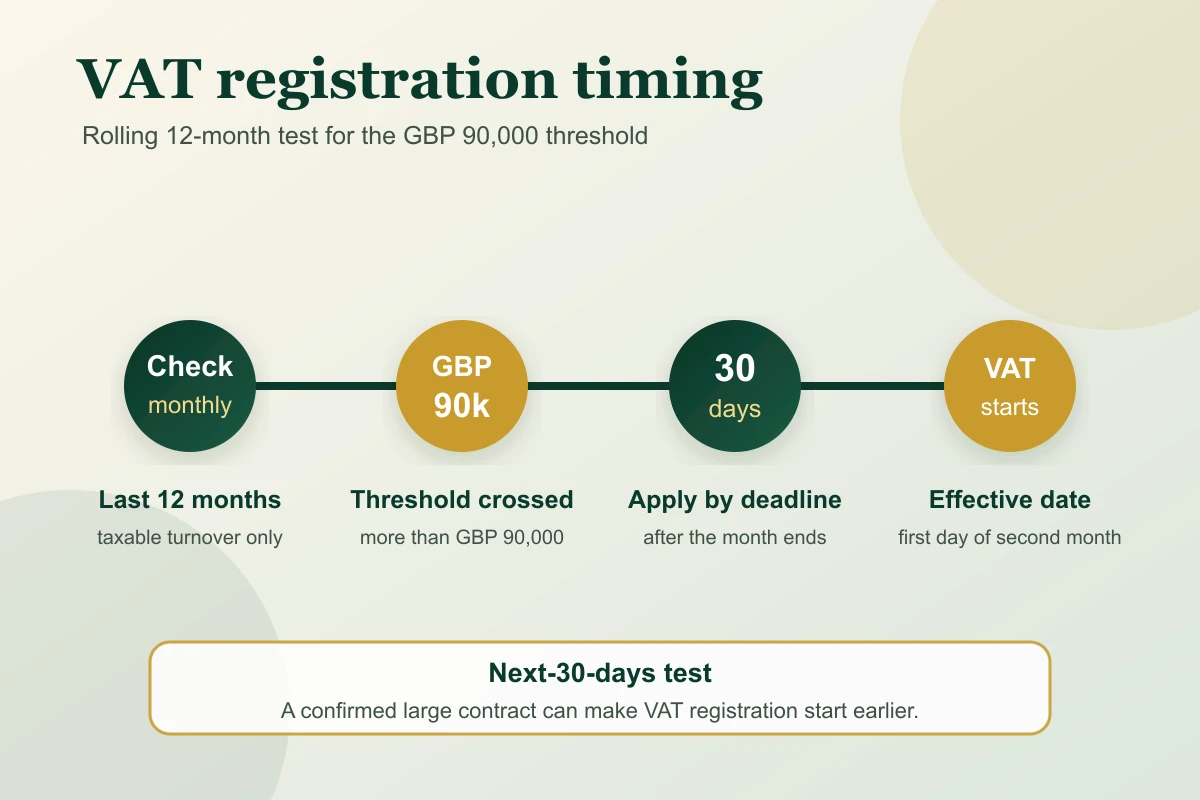

Right, so here is the practical version. You do not check the threshold once at your year end. You check it every month, looking back over the previous 12 months, and you also need to think ahead if you expect the next 30 days alone to push you over GBP 90,000.

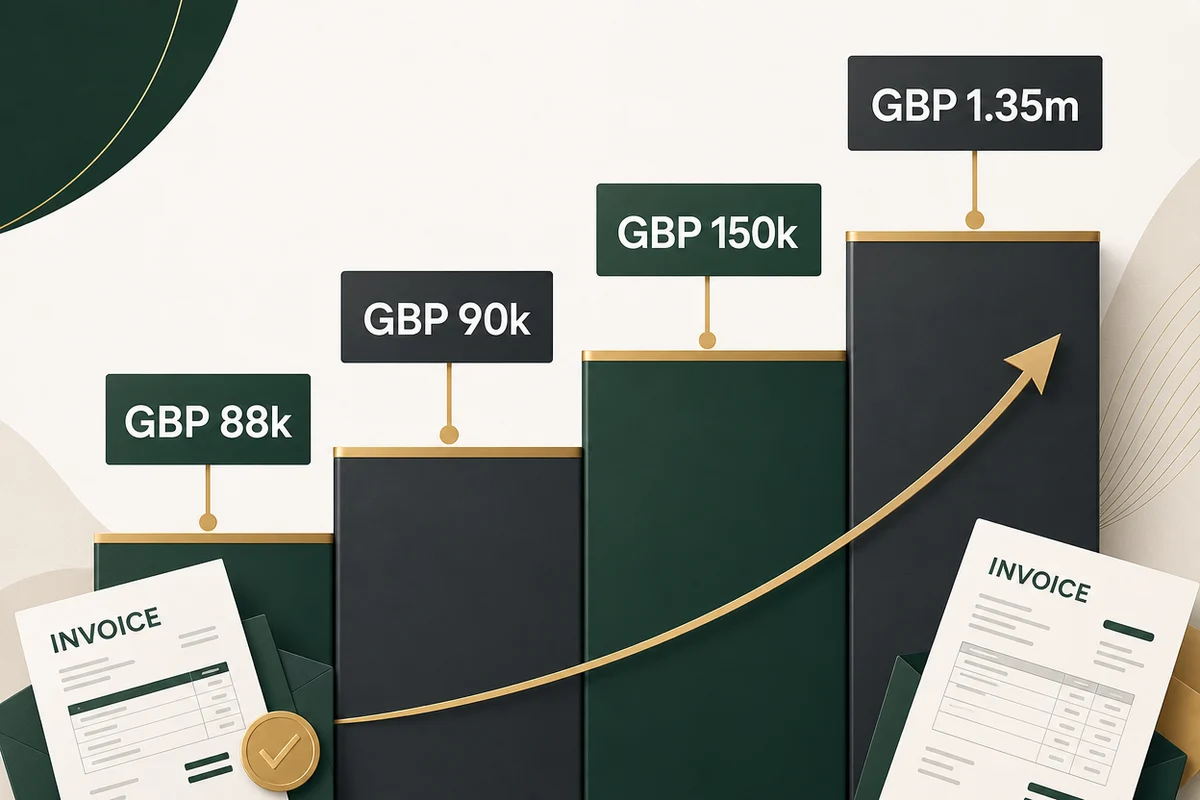

Quick summary: register for VAT if your VAT-taxable turnover goes over GBP 90,000 in the last 12 months, or if you expect it to go over GBP 90,000 in the next 30 days. The optional deregistration threshold is GBP 88,000. Once registered, new VAT businesses are normally brought into Making Tax Digital for VAT automatically.

If your sales are getting close to the threshold, we can help you review the numbers through our VAT registration service, VAT returns service, and bookkeeping support.

VAT registration threshold UK rules for 2026

GOV.UK currently lists the VAT registration threshold as more than GBP 90,000 of taxable turnover. It also lists the optional deregistration threshold as less than GBP 88,000 of taxable turnover.

Those two numbers matter, but they are not the whole story.

| Rule | Current figure | What it means in practice |

|---|---|---|

| VAT registration threshold | More than GBP 90,000 | You must register if VAT-taxable turnover goes over this level |

| Forward-looking test | More than GBP 90,000 expected in the next 30 days | A large contract can trigger registration before you have actually been paid |

| Optional deregistration threshold | Less than GBP 88,000 | You may be able to cancel VAT registration if taxable turnover falls below this level |

| Flat Rate Scheme join threshold | GBP 150,000 or less | Scheme may be available, subject to conditions |

| Cash Accounting Scheme join threshold | GBP 1.35 million or less | Useful where customers pay slowly |

| Annual Accounting Scheme join threshold | GBP 1.35 million or less | Fewer VAT returns, but regular payments still apply |

Official references:

The thing is, the threshold uses taxable turnover, not profit and not bank balance. A business with GBP 95,000 of taxable sales and GBP 85,000 of costs may still need to register. A business with GBP 110,000 of total income may not need to register if enough of that income is genuinely exempt or outside the scope of UK VAT.

That distinction is where many mistakes start.

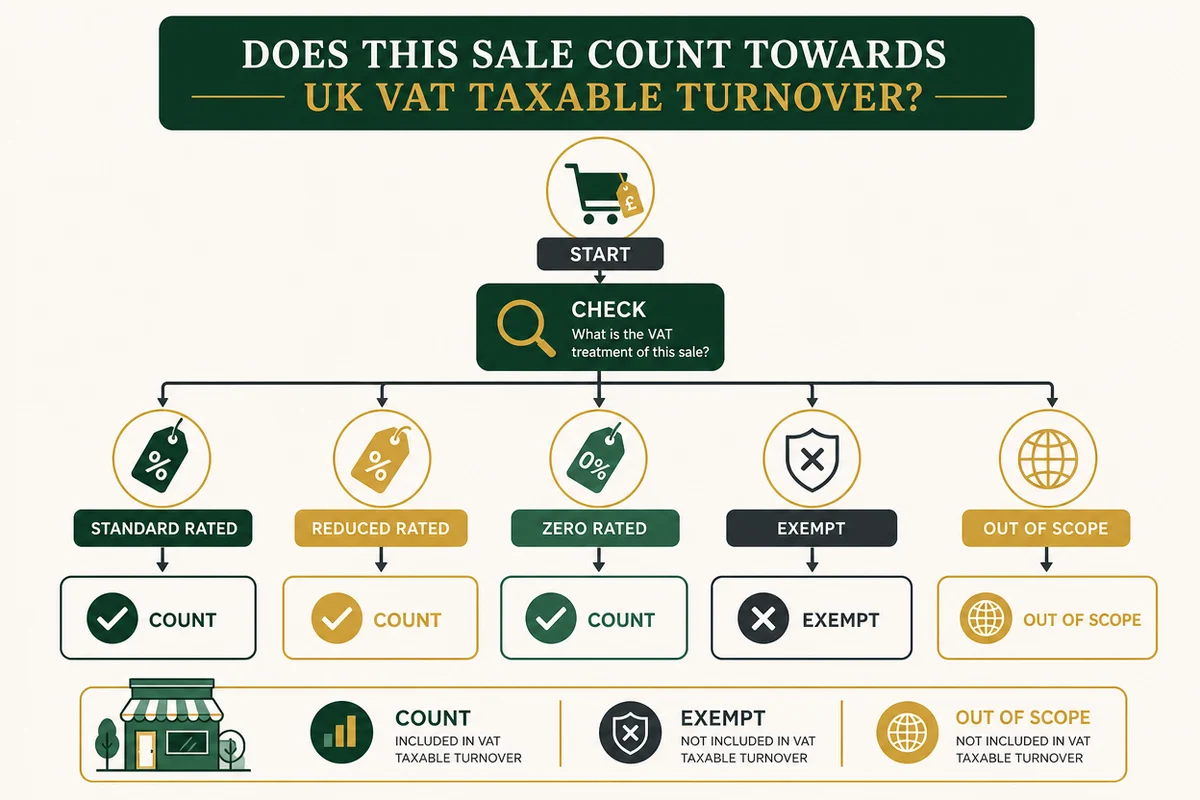

What counts as VAT-taxable turnover?

Taxable turnover is the value of sales that are not exempt and not outside the scope of VAT. GOV.UK says it includes standard-rated, reduced-rated, and zero-rated supplies. It can also include goods hired or loaned to customers, certain gifts or barter transactions, and reverse charge items in specific situations.

Plain English version: if your sales would be subject to VAT at 20%, 5%, or 0%, they usually count towards the threshold.

Here are common categories.

| Type of sale | Does it usually count towards the GBP 90,000 threshold? | Example |

|---|---|---|

| Standard-rated sales | Yes | Most consultancy, trades, retail goods, and professional services |

| Reduced-rated sales | Yes | Certain energy-saving materials or hospitality-related cases |

| Zero-rated sales | Yes | Some food, books, children’s clothing, and exports |

| Exempt sales | No | Many insurance, finance, education, and health services |

| Outside the scope | No, if correctly outside scope | Some overseas services, depending on place of supply rules |

Zero-rated is the category that catches people. A zero-rated sale can still be taxable turnover, even though the VAT rate is 0%. That means a business selling only zero-rated goods can still cross the registration threshold. In some cases, exemption from registration may be possible, but you need to ask HMRC for permission rather than assume.

Your specific supply mix can change the answer. If you sell digital services overseas, construction services under the domestic reverse charge, or mixed packages with exempt and taxable elements, get advice before treating any income as excluded.

The rolling 12-month test: the one most businesses miss

The backward-looking VAT test is not based on your accounting year, tax year, or company year end. It is a rolling 12-month test.

At the end of each month, add up your VAT-taxable turnover for the previous 12 months. If the total is more than GBP 90,000, you have crossed the threshold.

Once that happens, GOV.UK says you have to register within 30 days of the end of the month when you went over the threshold. Your effective date of registration is usually the first day of the second month after you went over.

Worked example 1: crossing the threshold in July

Assume a small design studio checks its taxable turnover on 31 July 2026.

The previous 12 months look like this:

| Month | VAT-taxable sales |

|---|---|

| August 2025 | GBP 6,200 |

| September 2025 | GBP 6,600 |

| October 2025 | GBP 7,000 |

| November 2025 | GBP 7,400 |

| December 2025 | GBP 5,900 |

| January 2026 | GBP 6,800 |

| February 2026 | GBP 7,100 |

| March 2026 | GBP 7,800 |

| April 2026 | GBP 8,200 |

| May 2026 | GBP 8,500 |

| June 2026 | GBP 9,000 |

| July 2026 | GBP 10,100 |

| Total | GBP 90,600 |

The studio has gone over GBP 90,000 in July.

Practical result:

- threshold crossed: 31 July 2026

- registration application due: 30 August 2026

- effective date of registration: 1 September 2026

From 1 September, the studio needs to charge VAT on taxable sales, keep VAT records, and prepare for VAT returns.

If the studio only checks turnover during annual accounts preparation in April 2027, it could be months late. That can mean paying VAT out of its own pocket on sales where no VAT was charged to customers.

The next-30-days test: large contracts can trigger VAT early

The forward-looking test is different. You must register if you realise that your taxable turnover will go over GBP 90,000 in the next 30 days alone.

This is not a vague forecast for the year. It is a short, specific 30-day test.

Worked example 2: one contract changes the VAT date

Assume a marketing consultant is not VAT registered. Their rolling 12-month taxable turnover is only GBP 62,000, so the backward-looking test has not been triggered.

On 1 June 2026, they sign a confirmed project worth GBP 96,000 for work to be delivered and invoiced in June.

The forward-looking test now matters:

- expected taxable turnover in the next 30 days: GBP 96,000

- threshold: GBP 90,000

- application deadline: 30 June 2026

- effective date of registration: 1 June 2026

That effective date can surprise people. Under the forward-looking rule, the VAT registration date is the date you realised you would cross the threshold, not a later month-end date.

For a large contract, that can affect the quote, contract wording, invoice, and cash flow immediately. If you sign a GBP 96,000 contract and later discover it should have been plus VAT, you may not be able to go back and recover the VAT from the customer.

What happens if you register late?

Late VAT registration is expensive because HMRC can require you to account for VAT from the date you should have been registered.

In plain terms, if you should have started charging VAT on 1 September but only register in December, HMRC can still ask for VAT on taxable sales made from 1 September onwards. If your customers will not pay extra VAT after the event, the money may come from your margin.

Worked example 3: late registration cash impact

Assume a retailer should have been VAT registered from 1 September 2026 but notices the problem on 1 December 2026.

Between September and November, it made taxable sales of GBP 36,000 to consumers. The prices were treated as VAT-inclusive because consumers were charged final shelf prices.

Using the standard 20% VAT fraction:

- VAT-inclusive sales: GBP 36,000

- VAT fraction at 20%: 1/6

- VAT due inside those sales: GBP 6,000

- net sales after VAT: GBP 30,000

If the retailer cannot charge customers more after the event, that GBP 6,000 comes out of cash already received. Input VAT on business purchases may reduce the net amount due, but the cash shock can still be serious.

HMRC also says you might need to pay a penalty depending on how much you owe and how late the registration is. The exact penalty position depends on the facts, so this is one of those areas where we would not recommend guessing.

Voluntary VAT registration: when it can make sense

You can choose to register voluntarily if taxable turnover is below GBP 90,000. That can be sensible in some situations.

Voluntary registration may help if:

- your customers are mostly VAT-registered businesses that can reclaim VAT

- you have significant VAT on start-up costs or equipment purchases

- you want a cleaner VAT record before you cross the threshold

- you plan to grow quickly and want pricing set up correctly from the start

It can be unhelpful if:

- your customers are mainly consumers who cannot reclaim VAT

- your margins are tight and competitors are not VAT registered

- admin time would outweigh the input VAT you reclaim

- your pricing does not leave room for VAT

Worked example 4: consumer pricing after VAT registration

Assume a tradesperson currently charges consumers GBP 1,000 for a job and is not VAT registered.

After VAT registration, there are two basic pricing choices.

| Option | Customer price | VAT due | Net retained before costs |

|---|---|---|---|

| Add VAT on top | GBP 1,200 | GBP 200 | GBP 1,000 |

| Keep price at GBP 1,000 | GBP 1,000 | GBP 166.67 | GBP 833.33 |

Neither answer is automatically right.

If your customers are VAT-registered businesses, adding VAT on top may be fairly painless because they can usually reclaim it. If your customers are private individuals, a 20% headline price rise may reduce demand. Keeping prices the same protects the customer price but cuts your net revenue.

The decision needs pricing, margin, customer type, and competitor checks. It is not just a tax form.

VAT schemes to consider after registration

Once registered, the default position is standard VAT accounting. You charge VAT on sales, reclaim VAT on purchases, and submit VAT returns, usually quarterly.

Some schemes may reduce admin or improve cash flow.

Cash Accounting Scheme

Under cash accounting, you usually account for VAT based on payments received and paid, rather than invoice dates. That can help if customers pay slowly because you are not funding VAT before cash arrives.

Current GOV.UK threshold figures show the scheme can be joined if taxable turnover is GBP 1.35 million or less, with a leaving threshold of more than GBP 1.6 million.

Flat Rate Scheme

The Flat Rate Scheme can simplify VAT calculations for some smaller businesses. You charge VAT to customers as normal, then pay HMRC a fixed percentage of VAT-inclusive turnover based on your business type.

The join threshold is currently GBP 150,000 or less, with a leaving threshold of more than GBP 230,000.

Be careful here. The Flat Rate Scheme is not automatically cheaper. Limited cost trader rules and sector percentages can change the result, and some businesses lose out because they cannot reclaim input VAT in the normal way.

Annual Accounting Scheme

Annual accounting usually means one VAT return each year with regular payments during the year. The join threshold is currently GBP 1.35 million or less, with a leaving threshold of more than GBP 1.6 million.

It can reduce filing frequency, but it does not remove the need for accurate records.

Making Tax Digital for VAT after registration

All VAT-registered businesses should now keep VAT records and submit VAT returns using compatible software unless exempt. GOV.UK’s Making Tax Digital for VAT collection says HMRC signs up new VAT-registered businesses automatically unless they are already exempt or have applied for exemption.

That means VAT registration is also a software and bookkeeping question.

Before you register, check:

- your bookkeeping software is compatible with Making Tax Digital for VAT

- sales invoices show VAT correctly from the right date

- purchase records separate VAT from net cost

- bank feeds and receipts are reconciled regularly

- you know which VAT return period HMRC has assigned

- someone owns the VAT payment calendar

If you still use spreadsheets, you may be able to use bridging software, but the digital link rules need care. A spreadsheet that only exists as a rough summary after the quarter ends is not a reliable VAT system.

Useful HMRC source: Making Tax Digital for VAT

Month-by-month VAT monitoring checklist

You do not need a complicated system to stay ahead of the threshold. You need a regular one.

Run this check at month end:

- Pull sales for the last 12 complete months.

- Remove genuinely exempt and outside-scope income.

- Keep zero-rated taxable income in the total.

- Add the 12-month VAT-taxable turnover figure.

- Compare it with GBP 90,000.

- Check signed contracts and expected sales for the next 30 days.

- Record the check in your bookkeeping notes.

- If turnover is above GBP 75,000, review monthly rather than waiting for accounts work.

A simple threshold tracker can sit next to your management accounts. If you are already using cloud bookkeeping, the report should take minutes once categories are set up properly.

For businesses hovering near the threshold, we often suggest an early pricing review. Waiting until the registration letter arrives means you may be changing prices, invoice templates, software settings, and customer terms all at once.

Common VAT registration mistakes

Checking annual turnover instead of rolling turnover

A company year end of 31 March does not protect you if you crossed the threshold in November. The rolling 12-month test keeps moving.

Excluding zero-rated sales

Zero-rated does not mean ignored. It can still count towards VAT-taxable turnover.

Waiting until payment is received

Turnover is not always the same as cash received. In many cases, invoice timing and supply rules matter, so do not rely only on bank deposits.

Forgetting the next-30-days test

One large contract can make registration immediate. That is particularly important for consultants, agencies, construction businesses, and project-based freelancers.

Assuming HMRC will tell you

HMRC may send prompts or letters in some cases, but responsibility sits with the business. A tax return showing turnover above GBP 90,000 is not a substitute for a VAT registration check.

Using old threshold figures

Some websites, templates, and service pages still mention GBP 85,000. Current GOV.UK guidance shows GBP 90,000. If your internal checklist still uses GBP 85,000, update it now so staff do not work from old figures.

What to do if you are close to GBP 90,000 now

If your rolling taxable turnover is already above GBP 75,000, treat VAT as a current planning issue rather than a future admin task.

Start with these actions:

- calculate your rolling 12-month taxable turnover today

- separate taxable, exempt, zero-rated, and outside-scope income

- check signed contracts for the next 30 days

- decide whether customer prices would be VAT-inclusive or plus VAT

- choose VAT-compatible bookkeeping software

- plan first VAT return dates and cash reserves

- speak to your accountant before submitting the application if supplies are mixed

For many businesses, the hardest part is pricing. The tax form is not the painful bit. The painful bit is finding out too late that your customer contracts do not let you add VAT on top.

If you want us to check your turnover position before you apply, use our contact page and send a short note saying you need a VAT threshold review. Bring your last 12 months of sales figures, sales categories, and any confirmed large contracts for the next month.

VAT registration FAQs

What is the VAT registration threshold in the UK for 2026?

The current VAT registration threshold is more than GBP 90,000 of VAT-taxable turnover. The optional deregistration threshold is less than GBP 88,000. Check GOV.UK before acting, because thresholds can change.

Is the VAT threshold based on profit or turnover?

It is based on VAT-taxable turnover, not profit. Costs do not reduce the threshold calculation. A business with thin margins can still need to register if taxable sales go over GBP 90,000.

Do zero-rated sales count towards VAT registration?

Yes, zero-rated sales usually count because they are taxable supplies, even though the VAT rate is 0%. Exempt and outside-scope income is different and may be excluded if correctly classified.

When do I have to register after crossing the threshold?

If your taxable turnover for the last 12 months goes over GBP 90,000, you usually have to register within 30 days of the end of the month when you crossed the threshold. Your effective date is normally the first day of the second month after crossing.

Can I register for VAT before reaching GBP 90,000?

Yes. Voluntary VAT registration can make sense if your customers are VAT-registered businesses or you have input VAT to reclaim. It can hurt pricing if your customers are consumers who cannot reclaim VAT.

Do I need Making Tax Digital software after VAT registration?

Usually, yes. GOV.UK says new VAT-registered businesses are signed up to Making Tax Digital for VAT automatically unless they are exempt or have applied for exemption. You should keep digital VAT records and submit VAT returns using compatible software.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

VAT Return Dates 2026: UK Deadline Guide for Small Businesses

VAT return dates 2026 explained for UK small businesses, with quarterly deadlines, payment dates, penalties, and examples.

VAT Cash Accounting Scheme UK: 2026 Guide for Small Businesses

VAT Cash Accounting Scheme UK rules for 2026, with thresholds, cash-flow examples, eligibility checks, and record-keeping tips.

VAT Return Deadline 7 May 2026: UK Checklist for Quarter Ending 31 March

VAT return deadline 7 May 2026 explained for UK businesses, with a filing checklist, common mistakes, error rules, and payment timing tips.