VAT Return Deadline 7 May 2026: UK Checklist for Quarter Ending 31 March

VAT return deadline 7 May 2026 explained for UK businesses, with a filing checklist, common mistakes, error rules, and payment timing tips.

VAT Return Deadline 7 May 2026: UK Checklist for Quarter Ending 31 March

The VAT return deadline for many UK businesses with a quarter ending 31 March 2026 falls on 7 May 2026. That sounds generous until you remember what usually sits inside that return: late purchase invoices, March sales still waiting to be reconciled, direct debit timing, and the small matter of making sure the numbers in your software match the records in your bank. Plenty of VAT problems are not technical tax disputes. They are bookkeeping delays wearing a tax deadline badge.

April can be awkward for exactly that reason. You are often closing one quarter, dealing with the new tax year, and trying not to let routine admin drift into early May.

Quick summary: if your VAT quarter ended on 31 March 2026, both the return and any payment are usually due by 7 May 2026. You must still file a return even if there is no VAT to pay. If you pay by Direct Debit, HMRC says you should set it up at least 3 working days before you submit your return. If you spot an old error, you may be able to correct it on a later return if it is within HMRC’s adjustment limits. If the position is messier than that, deal with it before deadline week, not during it.

If you want us to sense-check the figures before you file, we can help through our VAT returns service, bookkeeping service, and contact page.

VAT return deadline UK: the date that matters and who it applies to

HMRC’s general rule is straightforward. A VAT return is usually due 1 calendar month and 7 days after the end of the accounting period. For a business in the standard March quarter, that takes you from 31 March 2026 to 7 May 2026.

That date is not universal for every VAT-registered business. Some businesses are on different stagger groups. Some use annual accounting. Some have special arrangements. Still, a large number of small businesses land in the March, June, September, December cycle, so 7 May 2026 is a live deadline for many owners right now.

Two points are easy to miss:

- you must submit a VAT return even if you owe nothing or are due a repayment

- the payment must clear HMRC by the deadline as well, not just leave your account after it

If you pay by Direct Debit, HMRC says to set it up at least 3 working days before you submit the return. Leave it later than that and the payment may not be collected in time, which is a miserable way to create a penalty risk from an otherwise ordinary quarter.

Use this short table if your VAT period ended on 31 March:

| Item | Date or rule | What to do |

|---|---|---|

| Quarter end | 31 March 2026 | Finish posting March sales and purchase records |

| VAT return deadline | 7 May 2026 | Submit through MTD-compatible software |

| VAT payment deadline | 7 May 2026 | Make sure funds clear HMRC by that date |

| Direct Debit setup timing | At least 3 working days before submission | Check the mandate is active before filing |

| Nil return rule | Still required | File even if every box is zero |

Useful HMRC and GOV.UK references:

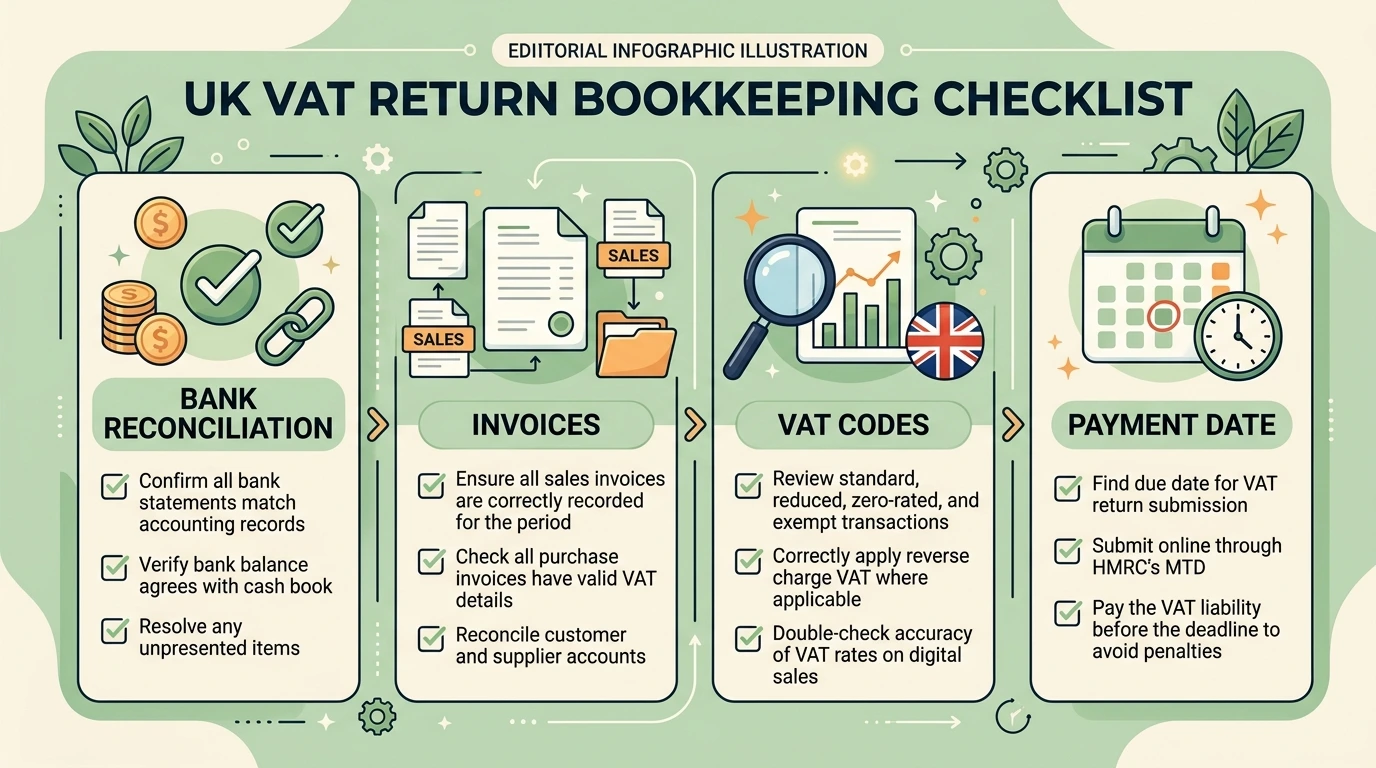

What to check before you press submit

The cleanest VAT returns are usually the ones that were prepared all quarter, not the ones that were heroically rescued on 6 May. Right, so let us focus on the checks that actually catch mistakes.

Start with the accounting records. Your software should show the same quarter you think you are filing. That sounds obvious, but it is common to see April invoices posted into March, March supplier bills left outside the quarter, or bank feed items still sitting uncoded while someone assumes the VAT report is somehow final anyway.

Work through this checklist before you touch the submit button:

- reconcile the main business bank account and any credit card used for business spending

- review sales invoices dated 1 January 2026 to 31 March 2026 and make sure credit notes are posted in the right period

- review purchase invoices and receipts, especially anything uploaded late in April

- check the VAT rates used on unusual transactions, such as zero-rated goods, exempt income, reverse charge items, or mixed supplies

- confirm import VAT, if relevant, has been handled using the correct records rather than guesswork

- look at the exception report in your software for uncategorised or suspense items

- check whether any private or non-business spending has been coded into reclaimable VAT by mistake

- make sure the return is being submitted through compatible software, because most VAT-registered businesses must now use Making Tax Digital software or bridging software

Bookkeeping quality matters more than people like to admit. If the records are late, the VAT return is late in spirit even if you manage to click submit on time.

Worked example 1: a quarter that looks fine until the late purchase invoices land

Assume a design studio has these March-quarter figures in the software on 28 April 2026:

- output VAT on sales: £5,640

- input VAT on purchases: £2,180

- VAT due to HMRC: £3,460

That owner feels fairly relaxed and expects to pay around £3,460 on 7 May.

Then three valid March purchase invoices are found in an email folder on 30 April 2026:

- software subscription annual renewal, VAT £96

- subcontract design support, VAT £420

- hardware purchase, VAT £180

Extra input VAT available:

- £96 + £420 + £180 = £696

Correct VAT due:

- £3,460 - £696 = £2,764

That is a difference of £696 from one quarter’s filing position. For a small business, that is not background noise. It is the difference between a routine payment and an avoidable overpayment.

Anyway, the lesson is simple. A VAT return is only as good as the records sitting underneath it.

Common VAT return mistakes that still catch small businesses

Some VAT errors are genuinely technical. Most are much duller than that.

Reclaiming VAT without the right evidence

You generally need valid VAT evidence before reclaiming input tax. Card statements and order confirmations are not always enough on their own. If a supplier has not issued a proper VAT invoice, stop and get the paperwork sorted before you reclaim.

The problem here is not just compliance. Weak evidence makes later reviews much harder, especially if the claim sits in a mixed quarter with lots of small digital purchases.

Filing the wrong quarter because the books were not closed properly

March quarter returns often go wrong when April bookkeeping starts too early. A few April sales get back-dated, a March supplier bill arrives late, or someone edits the period after the draft return has been reviewed. Small timing slips stack up fast.

One good habit is to lock the quarter internally before final review. You do not need a grand finance policy. You just need one agreed cut-off point so nobody is posting random corrections while the VAT boxes are being checked.

Forgetting that a nil return is still a return

HMRC still expects a submission even if there is no VAT to pay or reclaim for the period. This catches dormant or low-activity businesses surprisingly often. Quiet quarter, busy week, deadline missed, pointless penalty risk.

Leaving Direct Debit too late

Owners often think payment is solved because Direct Debit exists in theory. HMRC is much less sentimental. If the mandate is not set up early enough, or has gone inactive, the payment may not be collected in time.

Treating VAT like a year-end job

VAT is a quarterly deadline, but the data should be kept live. If you only clean up the books once every three months, every quarter feels like a rescue project. That is usually where coding mistakes, duplicate expenses, and missed sales adjustments creep in.

If that sounds familiar, our bookkeeping service and VAT returns service are often the fastest way to get the process back under control.

Worked example 2: how a Direct Debit timing slip turns into a payment problem

Assume a retailer completes the quarter and the final VAT bill comes to £3,240.

They submit the return on 7 May 2026 and assume HMRC will take the money by Direct Debit because it worked last year.

The problem is that the Direct Debit instruction was not active, and no alternative payment was made on time.

From the owner’s point of view, the filing job felt finished on 7 May. From HMRC’s point of view:

- the return was submitted

- the payment did not clear by the deadline

- the business now has a late payment issue on £3,240

That is the kind of mistake that feels unfair when it happens, but it is also avoidable. Check the payment method before filing day, not after it.

How to submit VAT return UK filings without deadline week chaos

The mechanics are not glamorous, but they are reliable if you follow them in order.

1. Confirm the exact quarter in your software

Make sure the return you are reviewing really covers 1 January 2026 to 31 March 2026 if you are aiming at the 7 May deadline. Do not assume the software has picked the right period just because the headings look familiar.

2. Review the VAT detail, not just the headline boxes

Look at the transactions behind the figures. Box 1 to Box 9 totals can look neat while the detail is wrong. Spot checks help. So do exception reports. So does asking the slightly annoying question: “Would I be happy defending this line if HMRC asked next month?“

3. Submit through compatible software

HMRC says VAT returns must generally be filed using Making Tax Digital-compatible software or bridging software. If you still rely on spreadsheets, that can work, but only if the submission route itself is compliant.

We covered the wider digital record issue in our Making Tax Digital for Income Tax checklist. VAT has been in the digital-filing world for a while now, so this should not be a last-minute surprise.

4. Sort payment before, not after, submission

If you pay by Direct Debit, check the mandate is live and leave enough time. If you pay another way, make sure the money reaches HMRC by the deadline. For a lot of small businesses, the filing job and the cash-flow job are treated as separate tasks. They should sit on the same checklist.

5. Keep proof that the return was received

HMRC’s online services let you check the return has been received. Save the confirmation or at least note when it was filed. It takes seconds and saves arguments later.

If you spot an error after filing, do not guess the fix

Errors happen. The important part is dealing with them properly.

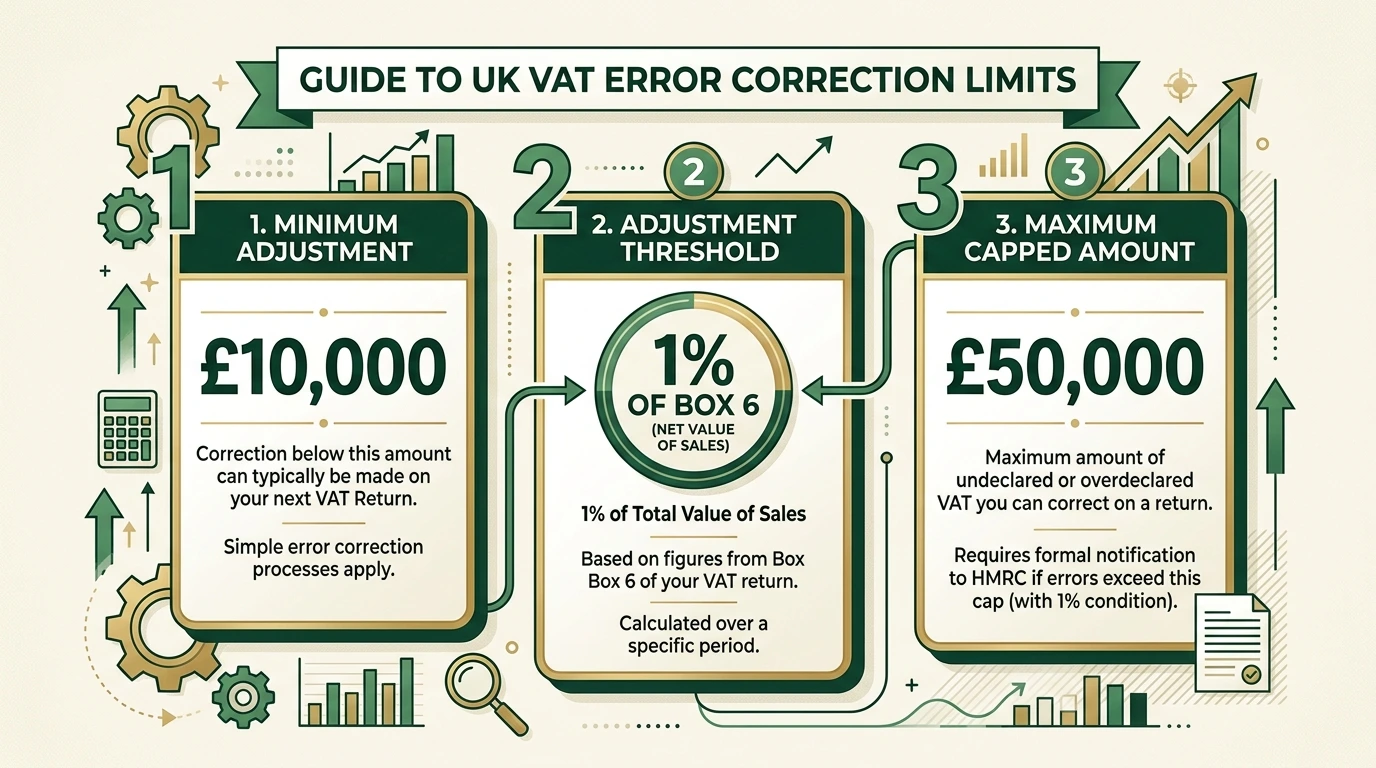

HMRC’s current error-correction rules say you may adjust a later VAT return if the net value of the errors does not exceed the greater of:

- £10,000, or

- 1% of the Box 6 figure on the return for the period in which the error was discovered, subject to an upper limit of £50,000

If the net error is above that limit, a separate notification is normally required. Deliberate inaccuracies cannot simply be tidied up on a later return because HMRC treats those differently.

That is one of those areas where the rules get a bit fiddly. The net value test matters. The period of discovery matters. The paperwork trail matters. If the numbers are not tiny, do not improvise.

Worked example 3: can a £12,000 old error go on the next return?

Assume a wholesaler discovers in May 2026 that a net VAT error from an earlier period was £12,000 underdeclared.

Now assume the Box 6 figure on the current return for the period of discovery is £1,600,000.

Calculate 1% of Box 6:

- £1,600,000 x 1% = £16,000

The relevant adjustment limit is the greater of:

- £10,000

- £16,000

So the limit here is £16,000.

Because the net error of £12,000 is below £16,000, the business may be able to adjust it on the VAT return for the period of discovery, assuming the error was genuinely discovered later and is not deliberate.

Change the facts slightly and the answer changes fast. If Box 6 for the discovery period were only £500,000, then 1% would be £5,000, so the greater figure would be £10,000. In that version, a £12,000 net error would sit above the adjustment limit and would usually need separate notification to HMRC.

Useful references:

- Correct errors in your VAT return

- HMRC VAT error correction manual: return adjustment net errors

- HMRC VAT error correction manual: monetary limits

What to do if you cannot pay the VAT bill on time

Filing and paying are linked, but they are not the same problem. A business can have the records ready and still hit a cash-flow squeeze.

If you know the payment will be difficult, do not wait for silence to turn into a debt problem. HMRC has guidance on setting up a payment plan, and it is far better to deal with that early than to miss the date and hope the issue sorts itself out.

Worked example 4: why early visibility matters

Assume your March-quarter VAT bill is likely to be about £4,800.

Cash available on 30 April 2026 is £3,100.

Expected shortfall:

- £4,800 - £3,100 = £1,700

If you spot that on 30 April, you still have time to:

- check whether the bill is accurate

- chase any outstanding customer payments

- move money from reserves if that is sensible

- speak to HMRC or your adviser before the deadline passes

If you discover it on the evening of 7 May 2026, the options are worse and the stress is higher. Tax admin is often won or lost a week earlier than people think.

FAQ: VAT return deadline UK

What is the VAT return deadline if my quarter ended on 31 March 2026?

For many quarterly VAT businesses, the return and payment deadline is 7 May 2026.

Do I still need to file if there is no VAT to pay?

Yes. HMRC still expects a VAT return, even if the period is nil.

Can I submit a VAT return using a spreadsheet?

You can use a spreadsheet only if the submission route is still compliant with Making Tax Digital, usually through bridging software or compatible filing software.

How late can I set up a Direct Debit for VAT?

HMRC says you should set it up at least 3 working days before you submit your VAT return.

What if I find an old VAT error after filing?

Small net errors may be adjusted on a later return if they fall within HMRC’s limits. Larger errors usually need separate notification. If you are unsure, get advice before amending anything.

Is this article personal tax advice?

No. It is general guidance for UK businesses. Your position may differ if you use a special VAT scheme, have mixed supplies, complex imports, partial exemption, or unusual timing issues.

Your next step before 7 May 2026

Open the VAT quarter in your software today, not next week. Reconcile the bank, review the purchase evidence, confirm the payment method, and make sure the quarter really is ready. If any part of that sounds less tidy than you would like, get in touch. A calm review in mid-April is much cheaper than a rushed repair job on 6 May.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

VAT Return Dates 2026: UK Deadline Guide for Small Businesses

VAT return dates 2026 explained for UK small businesses, with quarterly deadlines, payment dates, penalties, and examples.

VAT Registration Threshold UK 2026: When Small Businesses Need to Register

VAT registration threshold UK rules for 2026, with turnover tests, dates, penalties, voluntary registration, and worked examples.

VAT Cash Accounting Scheme UK: 2026 Guide for Small Businesses

VAT Cash Accounting Scheme UK rules for 2026, with thresholds, cash-flow examples, eligibility checks, and record-keeping tips.