CIS Tax Return for Subcontractors: 2026 Guide to Deductions and Refunds

CIS tax return guide for subcontractors, covering 20% and 30% deductions, refunds, records, deadlines, and worked examples.

CIS Tax Return for Subcontractors: 2026 Guide to Deductions and Refunds

A CIS tax return is where many construction subcontractors find out whether the deductions taken by contractors were enough, too much, or not enough. If you work under the Construction Industry Scheme, the 20% or 30% held back from your labour payments is not the final tax calculation. It is a payment on account towards your Self Assessment bill.

That distinction matters. A subcontractor can have tax deducted every month and still need to file a return by 31 January 2027 for the 2025/26 tax year. You may be due a refund, but you may also owe extra tax, Class 4 National Insurance, student loan repayments, or a payment on account for the following year.

Quick summary: CIS deductions are advance tax payments, not a complete tax return. Registered subcontractors usually have 20% deducted from labour payments. Unregistered or unmatched subcontractors can face 30% deductions. Gross payment status means 0% is deducted, but the tax still has to be dealt with through the return. Keep every monthly deduction statement, because those figures support your refund or final bill.

If your CIS records are messy, we can help through our Self Assessment service, bookkeeping support, or a practical review via our contact page.

CIS tax return rules in plain English

The Construction Industry Scheme applies when contractors pay subcontractors for construction work. Under the scheme, the contractor may deduct money from the labour part of your payment and send it to HMRC. GOV.UK explains the subcontractor side in its guide to what you must do as a CIS subcontractor.

For a sole trader subcontractor, the annual tax position is usually settled through Self Assessment. Your return brings together:

- gross CIS income before deductions

- allowable business expenses

- CIS deductions already taken by contractors

- other self-employed income

- employment income, if you also have a PAYE job

- rental income, dividends, savings income, or other taxable income

- income tax, Class 4 National Insurance, and any payments on account

One common mistake is treating the banked amount as income. If a contractor pays you £800 after deducting £200 CIS tax from a £1,000 labour payment, the Self Assessment income figure starts from £1,000, not £800. The £200 is then entered as CIS tax already deducted.

Another mistake is assuming that a refund is automatic. CIS deductions can be high compared with your final tax bill, especially if your expenses are large. But if your profit is strong, or you have other untaxed income, the deductions might not cover the full bill.

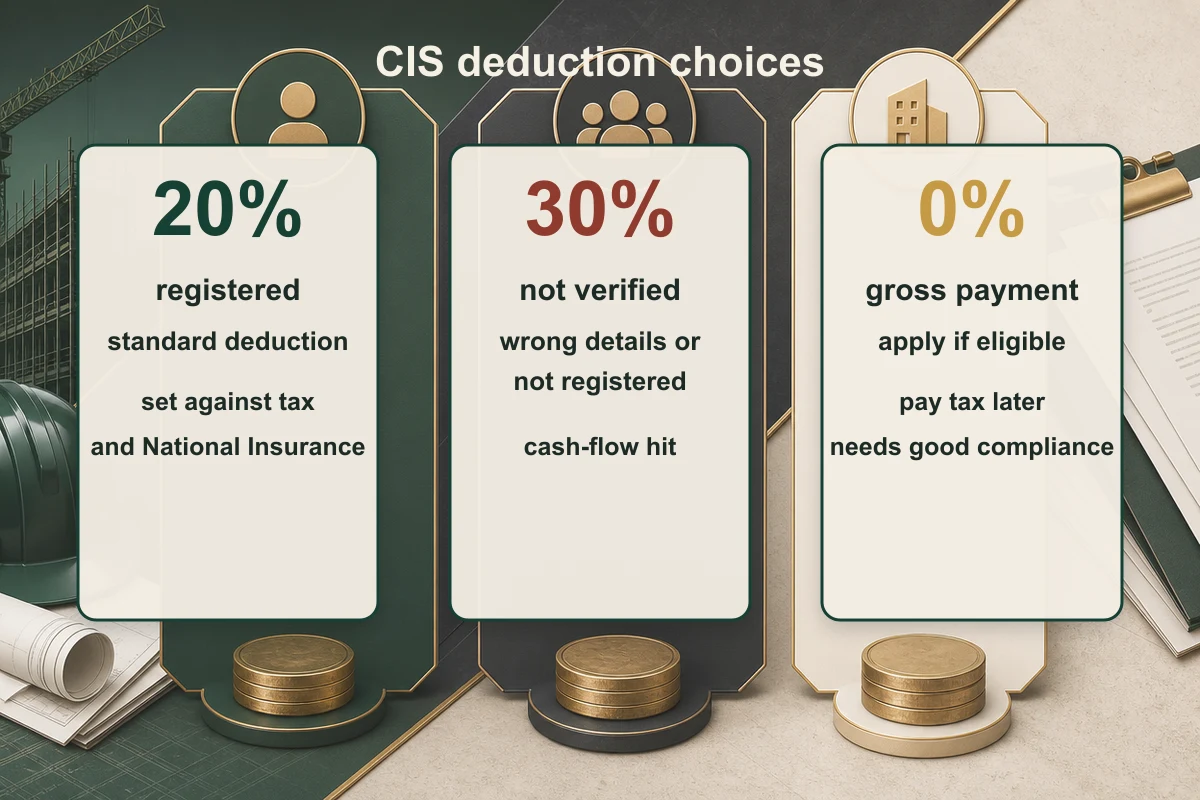

The 20%, 30%, and gross payment rates

HMRC uses contractor verification to decide which deduction rate applies. A contractor should verify you before paying you under CIS. If your details match HMRC’s records and you are registered as a subcontractor, the standard deduction is usually 20%. If you are not registered, or the contractor cannot match your details, the deduction can be 30%.

Gross payment status works differently. If HMRC approves gross payment status, contractors pay you without CIS deductions. That can help cash flow, but it also means you need stronger discipline, because the tax is not being held back month by month.

| CIS treatment | What the contractor usually does | What it means for your tax return |

|---|---|---|

| 20% registered deduction | Deducts 20% from labour, excluding VAT and most materials | You enter the gross income and claim the deduction already taken |

| 30% unregistered or unmatched deduction | Deducts 30% from labour | You may be over-deducted, but you need the statements to prove it |

| 0% gross payment status | Pays without deduction | You still declare the income and pay tax through the return |

The deduction is normally taken from labour. Materials are usually excluded from the CIS deduction calculation if they are genuine materials charged to the contractor. VAT is also not part of the CIS deduction if you are VAT registered and the invoice is handled correctly.

Right, so the practical point is simple: your invoice needs to split labour, materials, and VAT clearly. A vague invoice makes it easier for the wrong amount to be deducted and harder to fix later.

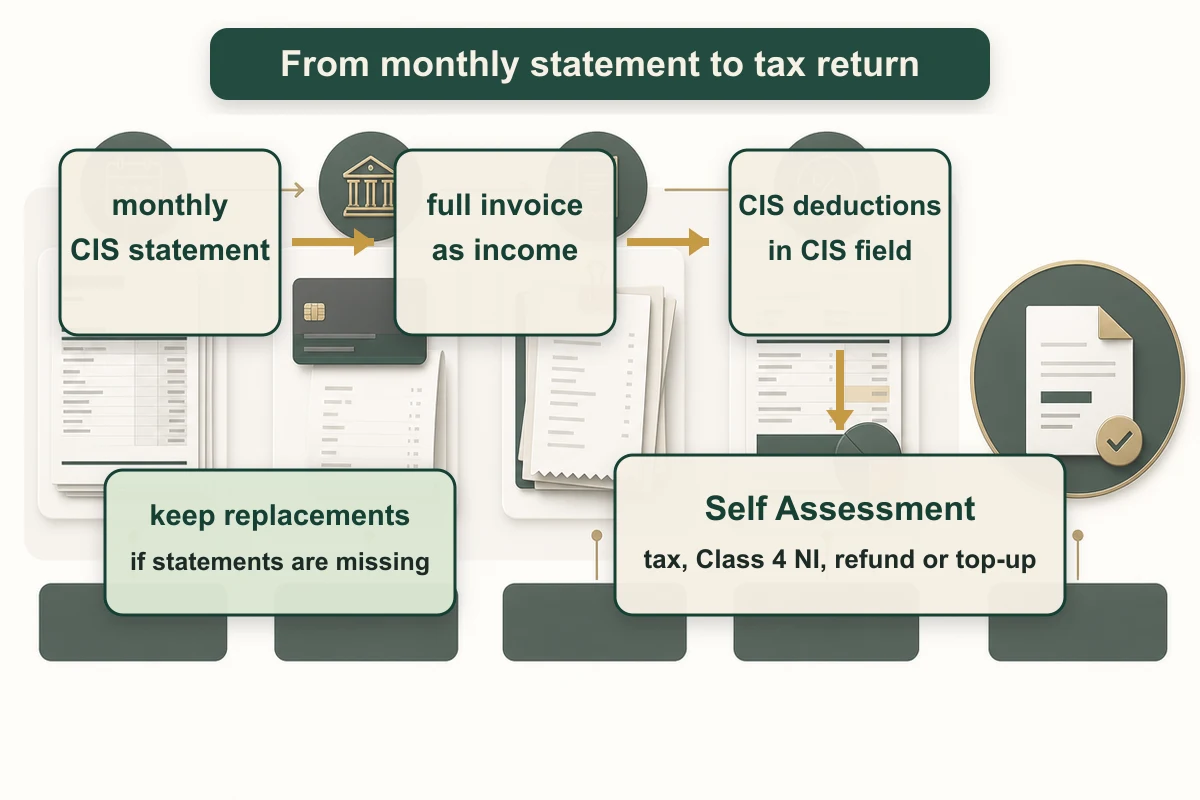

What records you need before filing

Monthly CIS deduction statements are the key documents. Contractors must give you a payment and deduction statement when they make CIS deductions. The statement should show the gross payment, cost of materials if relevant, amount deducted, and the tax month.

Keep those statements even if the money arrives in your bank account and the contractor seems organised. HMRC can ask for evidence, and a missing statement can delay a refund.

Before you file, pull together:

- all CIS monthly deduction statements for the tax year

- sales invoices issued to contractors

- bank statements showing payments received

- receipts and bills for tools, equipment, insurance, phone, fuel, van costs, accountancy, and other business expenses

- mileage records if you claim mileage rather than actual vehicle costs

- VAT returns if you are VAT registered

- payroll records if you employ anyone

- details of other income, including PAYE, property, dividends, and interest

If a contractor has not given you a statement, ask for a replacement before filing. Do not guess the deduction from the bank payment unless there is genuinely no better evidence. Guesswork is where CIS refunds start to go sideways.

Our bookkeeping service can help keep the monthly records tidy, while our Self Assessment service can deal with the annual return and CIS deduction claim.

Worked example: when CIS creates a refund

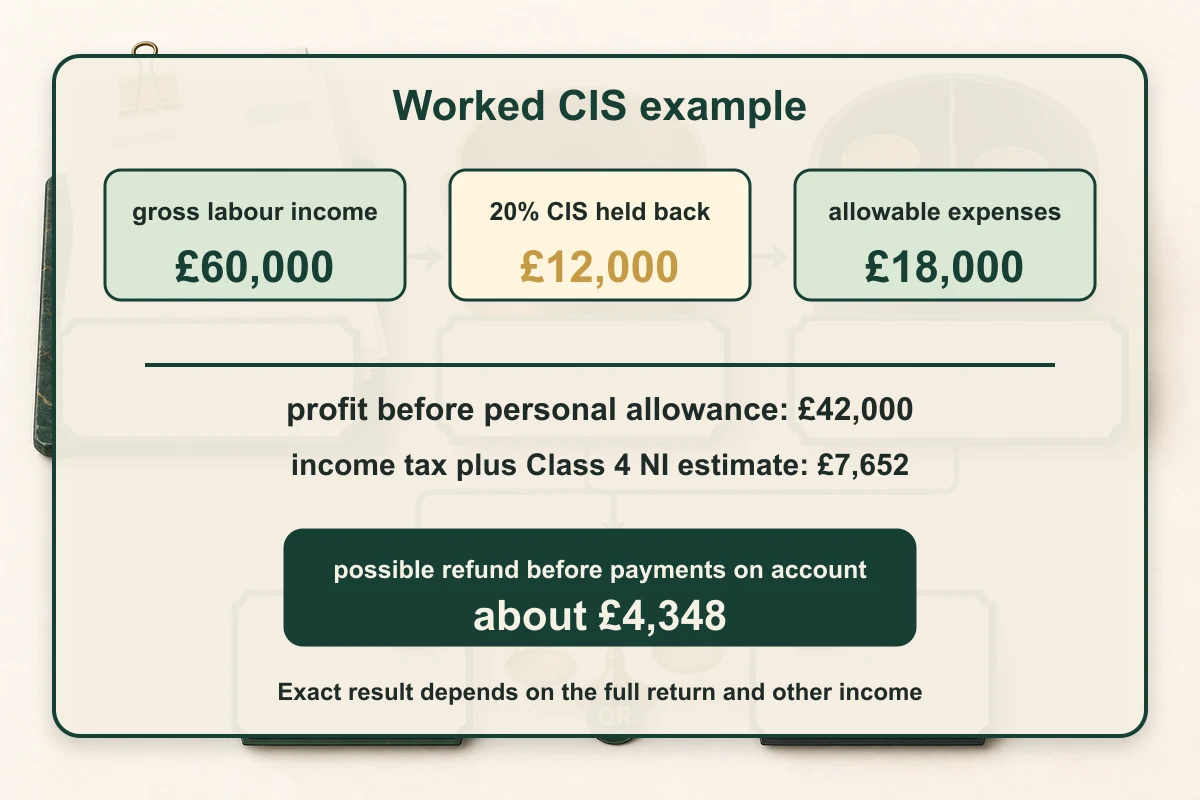

Assume Dan is a registered sole trader subcontractor. In the 2025/26 tax year, his contractor statements show:

| Item | Amount |

|---|---|

| Gross labour income before CIS | £60,000 |

| CIS tax deducted at 20% | £12,000 |

| Allowable business expenses | £18,000 |

| Profit before personal allowance | £42,000 |

Dan’s profit is £42,000. Using the standard Personal Allowance of £12,570, his taxable income is £29,430 if he has no other income and the allowance is fully available.

At the 2026/27 basic rate of 20%, income tax on £29,430 is £5,886. Class 4 National Insurance for many self-employed people is 6% on profits between £12,570 and £50,270, so that adds about £1,766. Together, that is roughly £7,652 before considering any other income, student loan, payments on account, or adjustments. You can check the current GOV.UK pages for income tax rates and allowances and National Insurance rates if you want to compare the figures.

Dan has already had £12,000 deducted under CIS. On those simplified numbers, he might be due about £4,348 back before any payments on account are considered.

That example is deliberately neat. Real returns often have van finance, mixed-use costs, private fuel, VAT, PAYE income, pension contributions, or payments on account. Your specific position may differ, so treat the calculation as a map rather than advice for your own figures.

Worked example: when CIS does not cover the bill

Now assume Priya has gross CIS labour income of £85,000, CIS deductions of £17,000, and allowable expenses of £14,000. Her profit is £71,000.

If Priya has the full Personal Allowance, taxable income starts at £58,430. The first £37,700 falls in the basic rate band at 20%, giving £7,540 of income tax. The remaining £20,730 falls into higher rate tax at 40%, giving £8,292. Income tax is about £15,832.

Class 4 National Insurance adds roughly £2,677:

| Band | Calculation | Amount |

|---|---|---|

| Main Class 4 band | £37,700 at 6% | £2,262 |

| Upper Class 4 band | £20,730 at 2% | £415 |

| Rounded estimate | £2,677 |

That makes the income tax and Class 4 estimate around £18,509. CIS deductions of £17,000 would not fully cover it. Priya may also face payments on account for the next tax year. The return is still worth doing early, because knowing the shortfall in October is much better than discovering it on 30 January.

How to enter CIS deductions on the tax return

Most sole trader CIS subcontractors complete the self-employment pages of the Self Assessment return. The return asks for business income and expenses, then has a separate place for CIS deductions taken from subcontractor payments.

The order matters:

| Step | What to do |

|---|---|

| 1 | Add up gross CIS income before deductions |

| 2 | Include other self-employed sales, if any |

| 3 | Claim allowable expenses with evidence |

| 4 | Enter CIS deductions from contractor statements |

| 5 | Check the final tax, National Insurance, and payment on account result |

If you only enter the money received after deductions, your income will be too low and your CIS tax claim may not match the contractor records. If you enter the gross income but forget the deductions, your tax bill will look too high.

GOV.UK’s Self Assessment deadlines page confirms the normal online deadline is 31 January after the end of the tax year. For the 2025/26 tax year, that means 31 January 2027. Paper returns are usually due earlier, on 31 October.

Allowable expenses for CIS subcontractors

Expenses are where subcontractors often lose money. Not because the rules are impossible, but because the evidence is weak by the time the return is prepared.

Common allowable expenses can include:

- tools and equipment used for the trade

- replacement protective clothing and safety boots

- public liability insurance

- accountancy and bookkeeping fees

- van costs, fuel, repairs, insurance, and parking for business journeys

- mobile phone costs, where the business part is reasonable

- training that updates existing trade skills

- subcontracted labour, if you pay others and handle the CIS rules properly

- materials bought for jobs, where they are not reimbursed separately

Some costs need care. Normal everyday clothing is not usually allowable just because you wear it to work. Fines are not usually allowable. Travel from home to a regular site can be tricky if the site has become a normal workplace. Van costs need a consistent method and decent records.

Worked example: tools and private use

Assume you buy a tool set for £1,500 and use it entirely for your subcontracting work. If it qualifies as a business expense or capital allowance claim, the business claim may be £1,500.

Now change the facts. You buy a laptop for £1,200 and use it 70% for quotes, invoices, site photos, and bookkeeping, with 30% private use. A reasonable business claim might be £840. That is £1,200 multiplied by 70%.

The point is not that every item needs a perfect scientific split. The point is that your claim should be reasonable, evidenced, and consistent.

CIS, VAT, and materials

CIS and VAT are separate systems, but they often meet on the same invoice. If you are VAT registered, VAT returns must be handled correctly alongside CIS. The CIS deduction should not be taken from VAT. It is usually applied to the labour element after excluding VAT and genuine materials.

For example:

| Invoice line | Amount |

|---|---|

| Labour | £2,000 |

| Materials | £500 |

| VAT at 20% | £500 |

| Total invoice | £3,000 |

If the contractor deducts CIS at 20% from the labour only, the deduction is £400. The payment you receive would be £2,600, assuming no other adjustments. Your VAT return still needs to deal with the £500 output VAT, and your Self Assessment return still starts from the gross income figures.

If your VAT records and CIS records do not agree, fix the issue before filing. Our VAT returns service can sit alongside CIS bookkeeping where both systems are in play.

Limited companies under CIS

CIS is not only for sole traders. A limited company subcontractor can also suffer CIS deductions. The difference is how those deductions are relieved.

For a limited company, CIS deductions are usually set against PAYE, National Insurance, and other payroll liabilities through the company’s payroll process. If deductions exceed what the company owes, the company may claim a repayment from HMRC after the tax year.

Directors sometimes mix this up with their personal Self Assessment return. Company CIS deductions belong to the company. They are not personal tax deducted from the director’s own income. If you trade through a company, the bookkeeping needs to separate:

- company sales and CIS deductions

- director salary

- dividends

- reimbursed expenses

- Corporation Tax

- PAYE and employer filings

If your construction business has moved from sole trader to limited company, this is worth checking carefully. We cover company accounts and tax returns through our company accounts service.

How to avoid delays and wrong refunds

The fastest CIS tax return is usually the one where the monthly statements already agree to the bookkeeping. The slowest is the one where the accountant has bank receipts, partial invoices, missing contractor names, and no deduction statements.

Build a simple monthly routine:

| Monthly check | Why it matters |

|---|---|

| Save every contractor statement | Supports the CIS deduction claim |

| Match each statement to bank receipts | Spots missing payments or wrong deductions |

| Keep labour and materials split | Prevents deductions being calculated on the wrong amount |

| Photograph receipts before they fade | Tool and fuel receipts often disappear by January |

| Reconcile VAT, if registered | Stops VAT and CIS figures fighting each other |

| Check contractor details | Helps trace statements later if there is a dispute |

If a contractor deducts 30% and you expected 20%, deal with it quickly. It might mean your CIS registration details are wrong, your Unique Taxpayer Reference has been entered incorrectly, or the contractor has not verified you properly. Waiting until the tax return is due may still get the over-deduction back eventually, but it is poor cash-flow management.

Deadlines, penalties, and payments on account

For the 2025/26 tax year, the main online Self Assessment deadline is 31 January 2027. That is also the normal deadline for paying the balancing payment for 2025/26 and the first payment on account for 2026/27 if payments on account apply.

Payments on account can surprise CIS subcontractors. If your final Self Assessment bill is more than £1,000 and less than 80% of your tax was collected outside Self Assessment, HMRC may ask for advance payments towards the next year’s bill. CIS deductions count as tax deducted at source, but the final position depends on the whole return.

Say your final Self Assessment liability after CIS deductions is £2,400. HMRC may ask for:

| Date | Possible payment |

|---|---|

| 31 January 2027 | £2,400 balancing payment plus £1,200 first payment on account |

| 31 July 2027 | £1,200 second payment on account |

That can feel unfair when contractors already deduct CIS each month. The reason is that HMRC is looking at the remaining Self Assessment bill after all credits and deductions. If your profit or expenses change, payments on account can sometimes be reduced, but reducing them too far can lead to interest if the final tax is higher than your estimate.

When to get help

A straightforward CIS return is not difficult if the records are clean. Problems start when several things happen at once: missing statements, mixed labour and materials, VAT registration, a van on finance, work through both a sole trade and a limited company, or income from more than one source.

Speak to an accountant before filing if:

- your contractor has deducted 30% and you do not know why

- you have no monthly statements for part of the year

- you are VAT registered and the CIS deduction has been taken from the wrong amount

- you moved from sole trader to limited company during the year

- you employed other subcontractors

- you think you are due a large refund but the figures do not feel right

- you cannot tell whether payments on account apply

We can prepare the return, check the CIS statements, and explain the likely refund or payment before the deadline. Start with our Self Assessment service or send the details through the contact page.

CIS tax return FAQs

Do CIS subcontractors still need to file a tax return?

Usually, yes. CIS deductions are advance tax payments. A sole trader subcontractor normally still files Self Assessment to report income, expenses, deductions, and any final tax or refund.

Is CIS deducted from materials?

Genuine materials are usually excluded from the CIS deduction calculation. The contractor normally deducts CIS from labour, not VAT or qualifying materials. Your invoices should split the figures clearly.

Why has my contractor deducted 30% CIS?

The 30% rate often applies when you are not registered for CIS or the contractor cannot verify your details with HMRC. Check your UTR, business name, National Insurance number, and registration position.

Can CIS deductions give me a tax refund?

Yes. If the tax deducted by contractors is more than your final income tax and National Insurance bill after expenses and allowances, you may be due a refund. Other income and payments on account can change the result.

What deadline applies to a CIS tax return?

For most online Self Assessment returns, the deadline is 31 January after the end of the tax year. For the 2025/26 tax year, the online filing and payment deadline is 31 January 2027.

Can a limited company claim back CIS deductions?

Yes, but the route is different. Company CIS deductions usually offset PAYE and National Insurance liabilities first. Any excess is normally handled through the company’s payroll and repayment process, not the director’s personal tax return.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

Self Assessment Tax Returns UK: What You Need to Know

Learn who needs to file a Self Assessment tax return in the UK, important deadlines to remember, and top tips for accurate tax reporting.

Cash Basis Accounting for Sole Traders 2026: Rules, Examples, and When to Use Traditional Accounting

Cash basis accounting for sole traders in 2026, with current HMRC rules, worked examples, MTD points, and when traditional accounting is better.

MTD Penalties 2026: What Happens If You Miss a Quarterly Update?

MTD penalties in 2026 explained, including the first-year soft landing, penalty points, late payment charges, and examples.