MTD Penalties 2026: What Happens If You Miss a Quarterly Update?

MTD penalties in 2026 explained, including the first-year soft landing, penalty points, late payment charges, and examples.

MTD Penalties 2026: What Happens If You Miss a Quarterly Update?

MTD penalties are one of the biggest worries for sole traders and landlords now that Making Tax Digital for Income Tax has started. The good news is that HMRC has built in a first-year soft landing for quarterly updates. The less comforting news is that the soft landing does not mean you can ignore the new filing rhythm, forget the final tax return, or pay Self Assessment tax late without a cost.

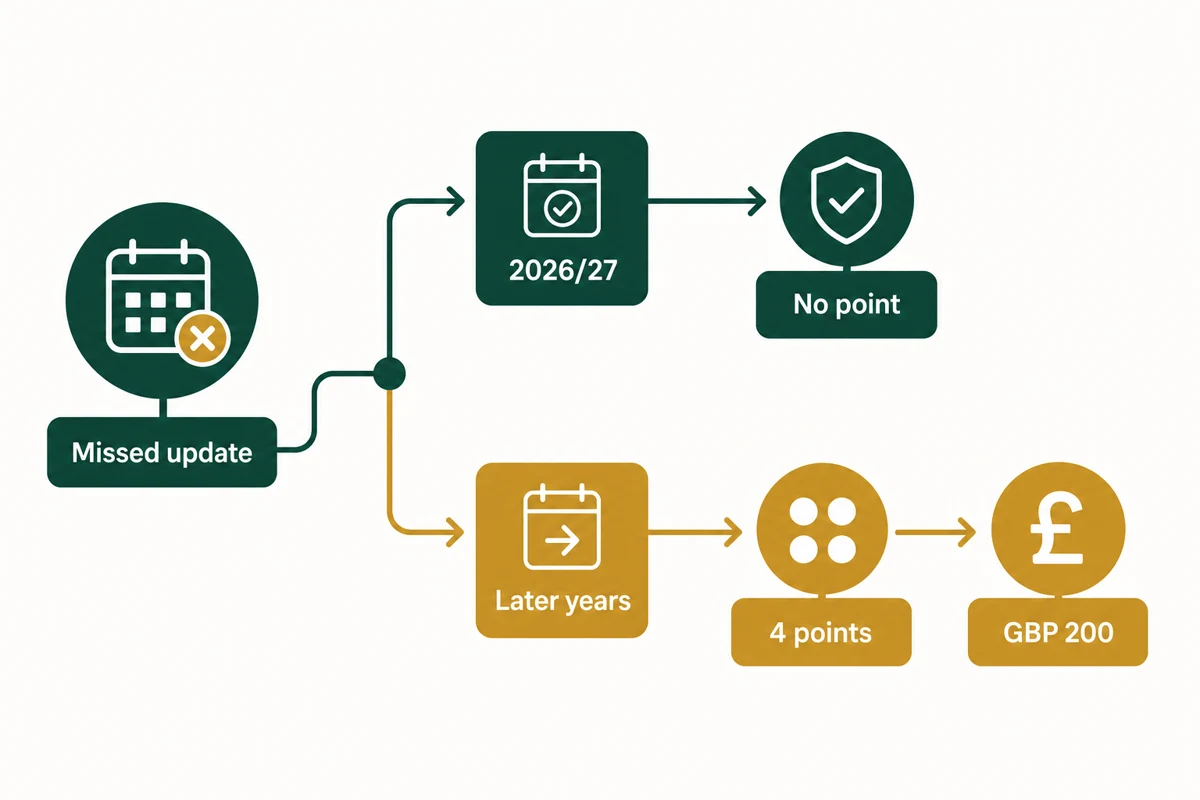

For the 2026/27 tax year, HMRC says there are no penalty points for late quarterly updates under Making Tax Digital for Income Tax. You still need to keep digital records, send the missing updates, and complete the final tax return by 31 January 2028. The quarterly updates are not optional. HMRC has simply decided not to issue penalty points for those quarterly update misses in the first year.

Quick summary: for 2026/27, missing an MTD quarterly update should not create a penalty point, but the update still has to be sent before the tax return can be filed. After 2026/27, each missed quarterly update or tax return deadline can create a penalty point. Reach 4 points and HMRC can charge £200, then another £200 for each later missed deadline while you are at the threshold.

If your records are already behind, fix the bookkeeping first. We can help through our Self Assessment service, bookkeeping support, or a practical review through our contact page.

MTD penalties 2026: the soft landing in plain English

HMRC’s current penalties for Making Tax Digital for Income Tax guidance says there are no penalties for missing a quarterly update deadline for the 2026 to 2027 tax year. Its quarterly update guidance says the same thing: HMRC will not apply penalty points for late quarterly updates during 2026/27.

That is helpful, but it is narrow.

The soft landing covers late quarterly updates for the first MTD year. It does not remove the duty to:

- keep digital records from the correct start date

- use compatible software

- send the quarterly updates before finalising the year

- submit the 2026/27 tax return by 31 January 2028

- pay Self Assessment tax by the normal payment dates

- deal with HMRC if you cannot pay on time

So the 2026/27 year is more like a training year for quarterly update penalties. It gives people space to get used to the process without immediate penalty points for those quarterly updates. It is not a free pass to leave everything until January 2028.

That distinction matters because the final tax return still has a filing deadline. HMRC says penalty points will still apply for late tax returns for the 2026/27 tax year. The final tax return is where your MTD records, other income, allowances, adjustments, claims, and final tax calculation are tied together.

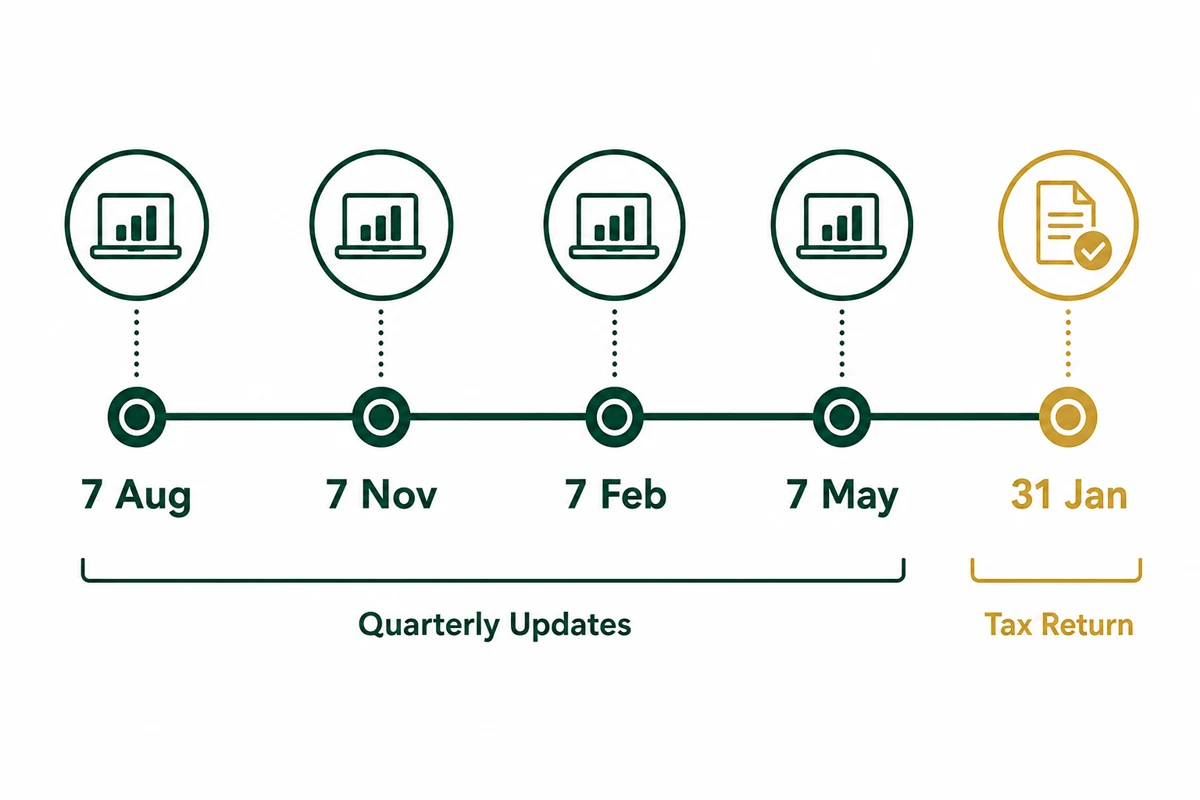

The MTD deadlines that drive the penalty rules

The first MTD year has the same quarterly update deadlines for standard and calendar update periods, even though the period dates differ.

| MTD filing point | Standard period | Calendar period | Deadline |

|---|---|---|---|

| Q1 update | 6 April to 5 July 2026 | 1 April to 30 June 2026 | 7 August 2026 |

| Q2 update | 6 April to 5 October 2026 | 1 April to 30 September 2026 | 7 November 2026 |

| Q3 update | 6 April 2026 to 5 January 2027 | 1 April to 31 December 2026 | 7 February 2027 |

| Q4 update | 6 April 2026 to 5 April 2027 | 1 April 2026 to 31 March 2027 | 7 May 2027 |

| Final tax return | Full 2026/27 tax year | Full 2026/27 tax year | 31 January 2028 |

If you joined MTD for Income Tax from 6 April 2026, those dates should now be in your diary. The first update due on 7 August 2026 is the one that catches people because it arrives during summer, not during the usual January Self Assessment rush.

Our earlier guide to the MTD quarterly update deadline on 7 August 2026 explains the filing process itself. This guide is about what happens when the deadlines are missed.

Worth mentioning though: quarterly updates are summaries, not full tax returns. HMRC says the update sends income and expense category totals, not every receipt or invoice. That makes the filing lighter than a year-end return, but it still depends on records being up to date.

How the points-based MTD penalty system works after 2026/27

After the 2026/27 soft landing for quarterly updates, late submission penalties are points based.

HMRC’s headline rule is:

| Missed deadline | Penalty result after 2026/27 |

|---|---|

| One late quarterly update | 1 penalty point |

| One late tax return deadline | 1 penalty point |

| Reach the threshold | £200 penalty |

| Miss another deadline while at the threshold | Another £200 penalty |

For MTD for Income Tax quarterly filers, the penalty point threshold is 4 points. That makes sense because there are four quarterly updates in a year.

You can only get one penalty point per deadline. HMRC says this applies even if you have more than one business and send more than one quarterly update late for the same deadline. So if you have one sole trade and one UK property business, both with late Q2 updates after 2026/27, that deadline should not create two separate points.

Worked example 1: missing the first 2026/27 quarterly update

Assume Priya is a sole trader who joined MTD for Income Tax from 6 April 2026 because her qualifying income was over £50,000. Her first quarterly update is due by 7 August 2026, but she sends it on 18 August 2026.

Under HMRC’s first-year rule:

| Point | Result |

|---|---|

| Q1 update deadline missed | Late update |

| 2026/27 quarterly update penalty point | £0 and no point |

| Still needs to send update | Yes |

| Can submit final tax return without it | No, not until required updates are sent |

Priya should not get a quarterly update penalty point for that miss in 2026/27. She should still send the update, reconcile her records, and make sure Q2 is not built on a messy Q1 file.

There is a quiet practical risk here. If Q1 is late because the bank feed, categories, or software permissions do not work, those problems can roll into Q2. By November, the issue may be three months larger.

Worked example 2: four missed updates in a later year

Now assume the same pattern happens in 2027/28, when the quarterly update soft landing is no longer in place.

| Missed deadline | Penalty points after the miss | Charge |

|---|---|---|

| Q1 update late | 1 | £0 |

| Q2 update late | 2 | £0 |

| Q3 update late | 3 | £0 |

| Q4 update late | 4 | £200 |

| Next tax return deadline also missed | Still at threshold | Another £200 |

The point system is designed not to fine someone for one isolated slip. The problem starts when missed deadlines become a pattern. Four points is where the fixed penalty begins, then further missed submission deadlines can add more £200 penalties.

If you are close to that pattern, the answer is not to wait for HMRC letters. Get the outstanding updates sent, fix the record process, and keep proof of any software or access problems in case an appeal is needed.

Late payment penalties are a different thing

Quarterly update penalties are about filing. Late payment penalties are about paying tax.

Under MTD for Income Tax, HMRC says new late payment penalties apply to payments not paid in full by the relevant due date, including a balancing payment on your tax bill and amounts due after an amendment or assessment. HMRC also says the new late payment penalties do not apply to payments on account.

That last point is easy to misread. Payments on account can still attract late payment interest if paid late. The specific new late payment penalty structure is the part HMRC says does not apply to payments on account.

The main Self Assessment payment dates still matter:

| Payment | Usual due date |

|---|---|

| First payment on account | 31 January during the tax year |

| Second payment on account | 31 July after the tax year |

| Balancing payment | 31 January after the tax year |

GOV.UK’s Self Assessment deadline page confirms the 31 July second payment on account deadline. If your July payment is coming up and your income has dropped, read our Self Assessment payment on account guide before reducing the amount.

How the new late payment penalties can add up

HMRC says late payment penalties are more linked to how late the payment is. In the first year you are in the new penalty system, you have 30 days from the payment due date to either pay in full or contact HMRC to set up a payment plan. After the first year, this reduces to 15 days.

For the 2026/27 tax year, HMRC’s table shows:

| Payment timing | 2026/27 late payment penalty |

|---|---|

| Up to 15 days late | No penalty |

| 16 to 30 days late | 3% of tax owed at day 15, or no penalty if it is your first year |

| 31 days or more late | 3% of tax owed at day 15, plus 3% of tax owed at day 30 |

| From day 31 | Annual rate of 10% per year on the outstanding amount, charged daily for up to 2 years |

For the 2027/28 tax year, the percentages in HMRC’s corrected table are 4% rather than 3% at the day 15 and day 30 stages.

Late payment interest is separate. HMRC charges interest from the first day the payment is late until it is paid in full. The current published late payment interest rate for the main taxes is 7.75% from 9 January 2026, but this rate can change when Bank of England rates change. Check HMRC’s interest rate page before relying on a calculation.

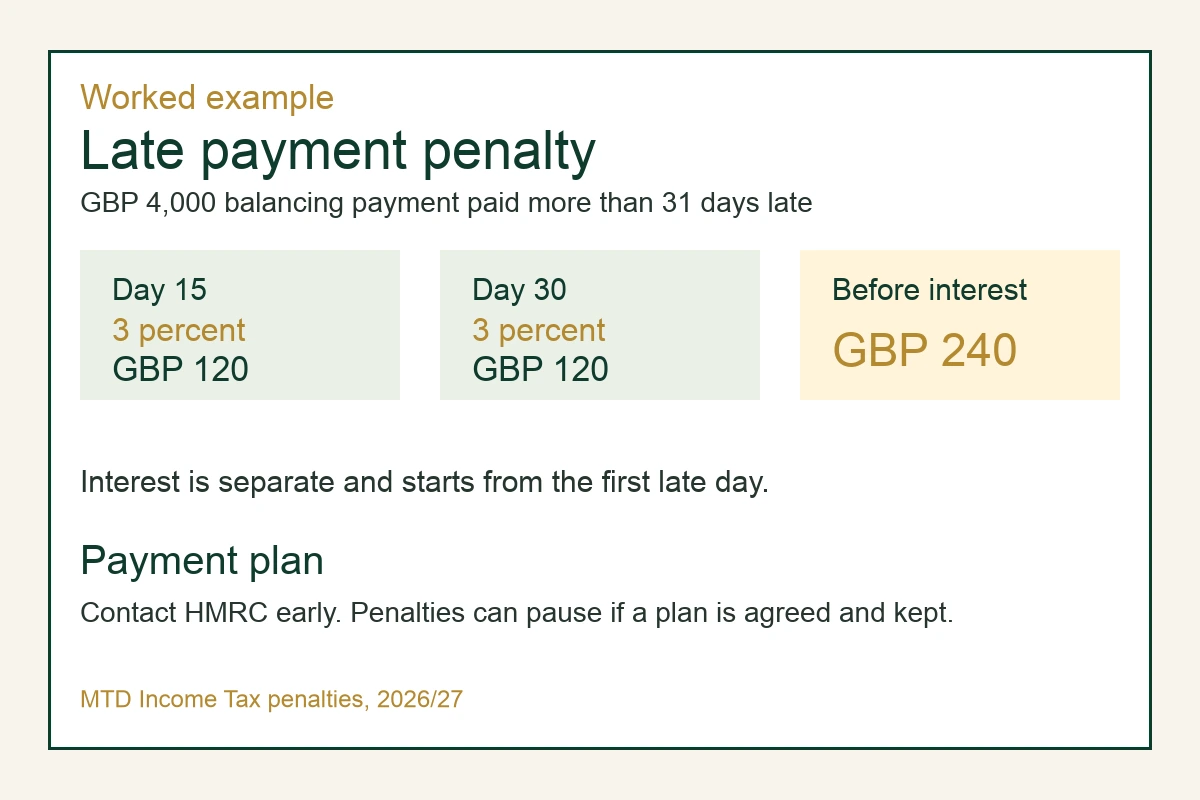

Worked example 3: £4,000 balancing payment paid late

Assume Marcus owes a £4,000 balancing payment for 2026/27, due by 31 January 2028. He is in his first year under the new late payment penalty rules and cannot pay in full.

If Marcus contacts HMRC within the first 30 days and agrees a payment plan, HMRC says penalties can be paused from the date he contacted them, as long as the plan is agreed and he keeps to it. Interest can still run on the unpaid balance.

If Marcus ignores the bill and pays more than 31 days late, the 2026/27 late payment penalty could look like this before interest:

| Step | Calculation | Amount |

|---|---|---|

| Tax owed at day 15 | Given | £4,000 |

| First penalty at 3% | £4,000 x 3% | £120 |

| Tax owed at day 30 | Still unpaid | £4,000 |

| Second penalty at 3% | £4,000 x 3% | £120 |

| Fixed percentage penalties before daily charge | £120 + £120 | £240 |

From day 31, the daily penalty charge can also apply at an annual rate of 10% on the outstanding amount, for up to two years. Late payment interest is separate from that.

This example is deliberately simple. If part of the tax is paid, if a payment plan is agreed, or if the amount changes after an amendment, the calculation can differ. The practical point is clear enough: contact HMRC early if you cannot pay.

What if you miss an MTD quarterly update in 2026?

If you miss a 2026/27 quarterly update deadline, do not freeze. The absence of a penalty point gives you a chance to repair the process.

Use this order:

- send the missing update as soon as your records are good enough

- check whether the software used standard or calendar update periods

- reconcile the bank account for the missed quarter

- correct obvious mispostings before the next update

- note why the update was late

- check whether other income sources need to be recorded for tax estimate purposes

- agree who is responsible for the next filing date

The next deadline arrives quickly. A Q1 update missed on 7 August 2026 can still be sitting unresolved when the Q2 deadline of 7 November 2026 arrives. That is how one admin issue becomes a full-year clean-up.

If software was the problem, get evidence. Keep support tickets, screenshots of errors, emails from the software provider, and notes of dates and times. Do not rely on memory months later.

What if you miss an MTD update after 2026/27?

After the first-year soft landing, a late quarterly update can create a penalty point. The first point is not a cash penalty by itself, but you should treat it as a warning light.

A sensible recovery process is:

| Task | Why it matters |

|---|---|

| Send the outstanding update | You need the missing submission cleared |

| Review all current-year deadlines | One late update often means another date is close |

| Check the penalty point position | Know whether you are near the 4-point threshold |

| Fix the bookkeeping cause | Late filing is often a record issue, not a filing issue |

| Keep evidence for appeal | Useful if there was a reasonable excuse |

| Put the next close date in writing | Someone needs ownership before the next quarter |

If you reach the four-point threshold, HMRC says the way out is stricter. Individual points do not just drop away one by one. You need to meet two conditions: submit quarterly updates and the tax return on time for 12 months, and submit all outstanding quarterly updates and tax returns for the previous 24 months.

Below the threshold, HMRC says each point is removed automatically 24 months after the missed deadline.

Worked example 4: clearing points below the threshold

Assume Aisha has two MTD penalty points from missed updates in a later year:

| Missed deadline | Point added | Automatic removal if below threshold |

|---|---|---|

| Q1 update due 7 August 2027 | 1 point | 7 August 2029 |

| Q2 update due 7 November 2027 | 1 point | 7 November 2029 |

If Aisha stays below four points, those points should fall away after 24 months from the missed deadlines. If she reaches four points before then, the clearance rule changes and she needs the 12-month on-time filing period plus the 24-month outstanding-submission clean-up.

That is why one or two points should not be ignored. They may feel harmless at first, but they reduce your room for error.

Appeals and reasonable excuse

HMRC says it will send a letter if you get a late payment penalty, a late submission penalty point, or a £200 late submission penalty. If you disagree, the letter should explain how to appeal.

An appeal is strongest when it is specific. “I was busy” is not the same as a serious illness, bereavement, HMRC system issue, software outage, or another event outside your control. Evidence matters.

Useful evidence might include:

- medical notes or appointment evidence where relevant

- software support tickets

- screenshots of submission errors

- bank or payment confirmation records

- dated notes of calls with HMRC

- emails showing agent authorisation or access issues

- proof that the issue was fixed promptly once possible

There is no point dressing up a weak appeal. HMRC sees enough of those. If the update was late because records were not ready, the better answer is to fix the system and prevent the next miss. If there was a genuine reason, document it properly and act quickly.

How to avoid MTD penalties without turning bookkeeping into a second job

The easiest way to avoid penalties is not to become a tax calendar obsessive. It is to make monthly bookkeeping boring enough that quarterly updates are not dramatic.

For most sole traders and landlords, that means:

- one separate bank account for business or property income where possible

- bank feeds checked monthly

- receipt capture used for costs that are not obvious from the bank line

- regular costs coded with rules, then reviewed

- personal spending kept out of business categories

- software access tested before filing week

- update periods chosen before the first update is sent

- accountant access agreed early

- a reminder two weeks before each quarterly deadline

If you use spreadsheets, the discipline needs to be even stronger. A spreadsheet can work with bridging software, but only if dates, categories, income sources, and formulas are controlled. A spreadsheet with manual copy-and-paste habits is where errors breed.

Our MTD compatible software guide for sole traders covers the software choice in more detail. The short version is that the cheapest tool is not always the cheapest once missed deadlines, rework, and accountant clean-up time are included.

A practical month-by-month rhythm

Here is the rhythm we would rather see clients use.

| Timing | What to do |

|---|---|

| Monthly | Reconcile the bank feed and check income categories |

| Monthly | Attach or store evidence for larger or unusual costs |

| Two weeks before the MTD deadline | Run the quarterly update report and check odd items |

| One week before the deadline | Fix missing receipts, uncategorised items, and access issues |

| Filing week | Send the update, save confirmation, and note any estimates |

| After filing | Review the tax estimate, but remember it is not the final tax bill |

That rhythm is not glamorous. It works because it spreads the work. January Self Assessment panic usually comes from trying to compress twelve months of decisions into a few evenings. MTD makes that harder to get away with.

Final point before you relax about the 2026 soft landing

The 2026/27 soft landing is useful, and we are glad it exists. But it only protects against penalty points for late quarterly updates in that first MTD year. It does not remove the filing work, the final tax return deadline, late payment interest, or the need to keep digital records.

If your first update is already at risk, treat June and July as a clean-up window. Reconcile April, May, and June. Check the software route. Make sure your accountant can access the file. Then send the Q1 update before 7 August 2026, or as soon as possible after that if the deadline has already slipped.

That is the practical move: use the soft landing to learn the system, not to postpone the problem.

About Golden Tree Consulting

AAT Licensed | ACCA Affiliated

Golden Tree Accounting & Business Consulting provides expert tax, bookkeeping, and advisory services to sole traders and SMEs across Croydon, London, Surrey, and Kent. With multilingual support and decades of combined experience, we help businesses stay compliant and grow.

More Articles You Might Like

Continue exploring our financial insights

MTD Quarterly Update Deadline 7 August 2026: Sole Trader and Landlord Guide

MTD quarterly update deadline 7 August 2026 explained for sole traders and landlords, with records, examples, and filing steps.

MTD for Income Tax UK: April 2026 Checklist for Sole Traders and Landlords

MTD for Income Tax starts in April 2026 for many sole traders and landlords. Use this practical checklist to get ready, avoid penalties, and file with confidence.

Cash Basis Accounting for Sole Traders 2026: Rules, Examples, and When to Use Traditional Accounting

Cash basis accounting for sole traders in 2026, with current HMRC rules, worked examples, MTD points, and when traditional accounting is better.